A blueprint for catalysing sustainable trade finance investment into African SMEs at scale

The African trade finance gap – stubbornly fixed at $100-130 billion annually – is a structural market failure that systematically excludes small and medium-sized enterprises from essential capital. These SMEs drive 80% of the continent’s employment, yet face rejection rates approaching 45% for trade credit applications. Meanwhile, empirical data from the ICC Trade Register consistently demonstrates that African trade finance assets carry default rates below 0.2%. In this paradox, low-risk assets remain unfunded while the real economy is starved for liquidity.

Beyond traditional trade finance

Traditional dollar-denominated, cross-border solutions (such as documentary letters of credit and LC refinance – known as FI Trade 1.0 and 2.0, respectively – and supply chain finance programmes) address only 30% of SME financing requirements. These instruments systematically exclude local currency, domestic trade flows, working capital products such as factoring and overdrafts, and the growing ecosystem of non-bank financiers serving the SME segment. The 70% coverage gap demands fundamentally different architecture.

Various SCF initiatives have been sporadically implemented across Africa. These programmes are necessary but demonstrably insufficient as scalable solutions. They employ small-scale aggregation calculus through anchor corporates, capturing only hundreds of SMEs’ payables credit per programme. Moreover, their expansion depends upon deep-tier trade digitalisation infrastructure that has yet to materialise at scale across African markets.

The regulatory displacement problem

The core structural barrier lies in what practitioners term the ‘Basel Paradox’. Prudential regulations (specifically the liquidity coverage ratio and net stable funding ratio requirements) compel African banks to hold substantial high-quality liquid assets, predominantly in the form of government bonds. Simultaneously, punitive risk-weighted asset allocations for SME exposures destroy return on equity for lending to the productive economy.

This creates a perverse incentive structure. Bank treasurers, acting rationally, invest in high-yield, zero-RWA government securities rather than finance trade. The result is an estimated $1.4 trillion in capital that sits trapped on African bank balance sheets. That is effectively ‘dead liquidity’ that could otherwise fuel SME growth. EIB research confirms this crowding-out effect, with African bank holdings of domestic sovereign debt rising from 10.3% to 17.5% of assets between 2010 and 2023.

Two breakthrough innovations

The FI Trade 3.0 Catalysing Sustainable SME Trade Investment Schema, presented at the Trade Finance Conference of Parties (TF COP) congress in London, offers a blueprint to resolve this impasse. The framework delivers two critical product innovations aligned with the UN’s sustainable trade finance interpretation articulated in the Seville Commitment.

First, portfolio-level aggregation. FI Trade 3.0 shifts the reference point entirely. Instead of refinancing individual cross-border transactions, it facilitates investment against an African bank’s entire portfolio of SME trade and working capital assets, including domestic, local currency trade, factoring, overdrafts, and exposures originated by non-bank financiers. By aggregating millions of underlying exposures, the schema transforms granular, high-volume SME financing into a diversified, institutional-grade asset class. This approach addresses the 70% of SME needs that traditional approaches cannot reach.

Second, the embedded option security. This mechanism unlocks the $1.4 trillion liquidity trap at its source. In traditional secured lending, when an African bank pledges or repos government bonds as collateral, those bonds become encumbered and are removed from LCR calculations, penalising the bank’s regulatory position. Banks are therefore reluctant to pledge their HQLA, leaving capital dormant.

The embedded option security resolves this through an elegantly simple structure. Rather than requiring a repo or pledge, the master trade loan agreement incorporates an embedded option known as contingent upon default, whereby the lender gains the right to exercise a put or call option on the bank’s government bonds at the outstanding loan amount. Under IFRS and Basel rules, this contingent option does not constitute an encumbrance until it is exercised. The bonds remain unencumbered (satisfying regulators) while the lender holds effective sovereign-backed security. Dead capital becomes live liquidity.

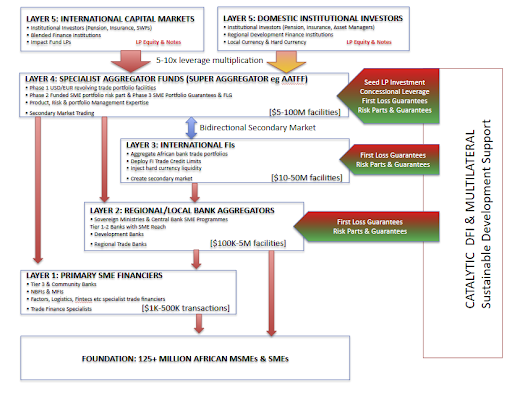

The architecture of public/private collaboration

Achieving scale requires structured collaboration across the financial ecosystem. The schema diagram below visualises two critical dimensions. First, the five-layer private sector architecture bridging 125 million African MSMEs to global institutional capital pools, and second, the TF COP-promulgated integration of ‘public’ DFI and multilateral catalytic support into the largely ‘private’ five layers of institutional financiers.

At the foundation, primary SME financiers, such as tier 3 banks, fintechs, MFIs, and specialist trade financiers, originate granular assets in the $1,000-$1M range. Regional and local bank aggregators, including Tier 1-2 banks and central bank SME programmes, aggregate these flows and deploy their government bond holdings as security via the embedded option mechanism. International financial institutions inject additional hard currency liquidity and create secondary market functionality by using their existing correspondent refinance credit limits. Specialist aggregator funds validate the sustainability of SME impact, manage portfolio risk, structure investment products, and enable bidirectional market activity. Finally, institutional capital from pension funds, insurance companies, sovereign wealth funds, and impact investors provides the ultimate funding source through LP equity and notes.

Integrated throughout this private sector architecture, DFIs and multilaterals provide catalytic sustainable development support: seed LP investment at the fund level, concessional leverage to enhance returns, and first-loss guarantees and risk participations cascading through each layer. This public/private integration brings SDG 17’s partnership principles to life, ensuring catalytic public capital de-risks and mobilises multiples of private institutional investment.

This structure achieves triple credit enhancement: self-liquidating trade assets as first recourse, the regulated FI obligor as second, and sovereign bond security (typically at 150% coverage) as ultimate backstop. The result transforms SME trade credit into an investment-grade, investable asset class product.

Sustainable trade finance at scale

The structured collaboration creates a powerful leverage cascade. Through aggregation, security mechanisms, and the velocity of short-term revolving trade assets, the schema can transform every $1 of catalytic DFI capital into $60-90 of real-economy impact, decisively moving the rhetoric of ‘billions to trillions’ toward reality.

This capability aligns directly with the Seville Commitment adopted at FfD4 in July 2025, which explicitly called for sustainable trade finance mechanisms to mobilise private capital for productive capacity building. The schema provides both the missing bridge between institutional investment pools and SME trade credit, and an overarching framework to organise the SDG 17 collaboration that TF COP seeks to promulgate.

The Washington Declaration’s commitment to halve the global trade finance gap by 2030 requires mechanisms that address root causes rather than symptoms. FI Trade 3.0 delivers precisely this. It aligns regulatory requirements with commercial incentives, recycles trapped sovereign exposure into productive SME financing, and creates the institutional-grade product structures that pension funds and insurers require. What remains is the vision and collaboration the UN called for in Seville. The architecture exists, and the mechanism is proven. What we are still waiting for is the $100 billion opportunity.