An insurance market in motion

The global trade credit and political risk insurance market has remained remarkably upbeat on the back of the realignment of supply chains and shifting trading relations in response to US tariffs. Counterparty risk mitigation has become a C-suite conversation in corporates and banks alike, driving opportunity for the insurance market. Trade protectionism, volatile energy markets, political upheaval, and rising resource nationalism are reshaping risk profiles across Africa, Asia, and the Middle East. Insurers are increasingly focusing on project- and sector-specific coverage, while investors must navigate shifting regulatory frameworks and evolving trade barriers.

The familiar cycles of emerging market debt distress, trade disputes, and geopolitical flashpoints in the credit and political risk insurance (CPRI) market are converging. This new dynamic points to a lasting change in how global trade, investment, and risk are shared worldwide. For Africa, Asia, and the Middle East – regions that have long offered both outsized risk and reward – this convergence is reshaping portfolios, capacities, and underwriting priorities. Now, while the opportunities are clear, the dual challenge for insurers, brokers, and investors is to keep pace with these shifts and to position themselves to better understand where the new flows of capital and commerce, and protections that underpin them, will settle.

In order to mitigate trade counterparty risks, C-suite leaders require more detailed and forward-looking intelligence to explore new markets, sectors, and strategies where opportunities remain viable, offering insights to help stakeholders balance growth potential with disciplined risk management in an increasingly complex environment. Leaders also need to remain aware of emerging opportunities across frontier markets and be able to identify sectors where targeted insurance solutions could be most relevant.

PANGEA-RISK uncovers the forces shaping the CPRI market, turning political shifts, trade barriers, and economic volatility into actionable insights for your risk mitigation strategy.

An insurance market in motion

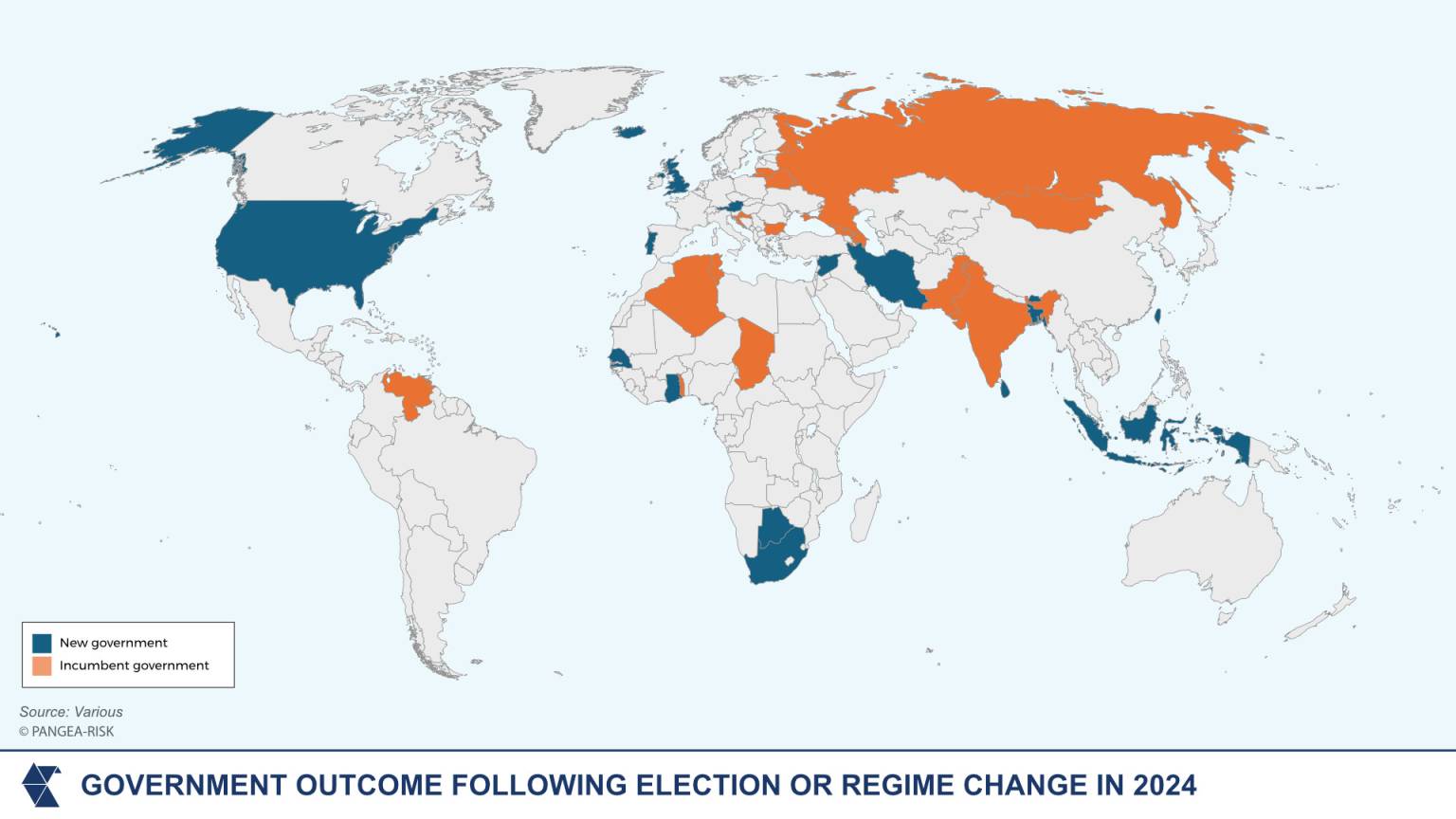

The CPRI market has been quietly but decisively rebalancing over the course of 2025 in response to several external factors. This trend, albeit evident since at least 2023, has been reinforced by a record number of elections in 2024, ushering in administration changes, the spread of military takeovers in parts of Africa, the rise of protectionist policies globally and, more recently, the growing unpredictability of the Trump administration.

According to Willis Tower Watson (WTW)’s March Credit and Political Risk Insurance Capacity Survey, for the reporting period January to March 2025, demand and available market capacity are both increasing for insurance covering contract frustration and transactional credit risks. At the same time, growth in insurance covering broader political risks (like expropriation, political violence, or government actions affecting investments) is slowing.

Rising geopolitical uncertainty, trade disputes, and changing domestic conditions have made political risk claims more complex and unpredictable, prompting insurers to limit their exposure to general political risk coverage. Instead, insurers are increasingly focusing on covering specific transaction risks rather than broad political risk policies. This does not mean political risk insurance is declining. Rather, as global trade and investment evolve, CPRI coverage is diversifying and becoming increasingly specific. Today, the global environment demands more targeted protection across different asset types and regions. As a result, as global uncertainty reshapes trade and supply chains, CPRI underwriters and brokers report heightened demand, with corporates and banks increasingly prioritising counterparty risk mitigation, creating a clear growth opportunity for the sector.

Overall, coverage for risks such as expropriation, currency inconvertibility, and sovereign default is becoming more selective, with many insurers reducing headline limits and concentrating on specific markets where risk can be more effectively managed. Underwriters appear willing to take on political risk in high-growth, sub-investment-grade economies, provided there is a clear project pipeline, reform momentum, and a realistic view of how risk will be mitigated over the policy term.

Emerging economies prove attractive

Across sub-investment-grade markets, a number of economies are demonstrating the mix of fundamentals, policy direction, and project visibility that can draw in discerning underwriters seeking opportunities beyond slower-growing advanced economies.

Industries on the rise

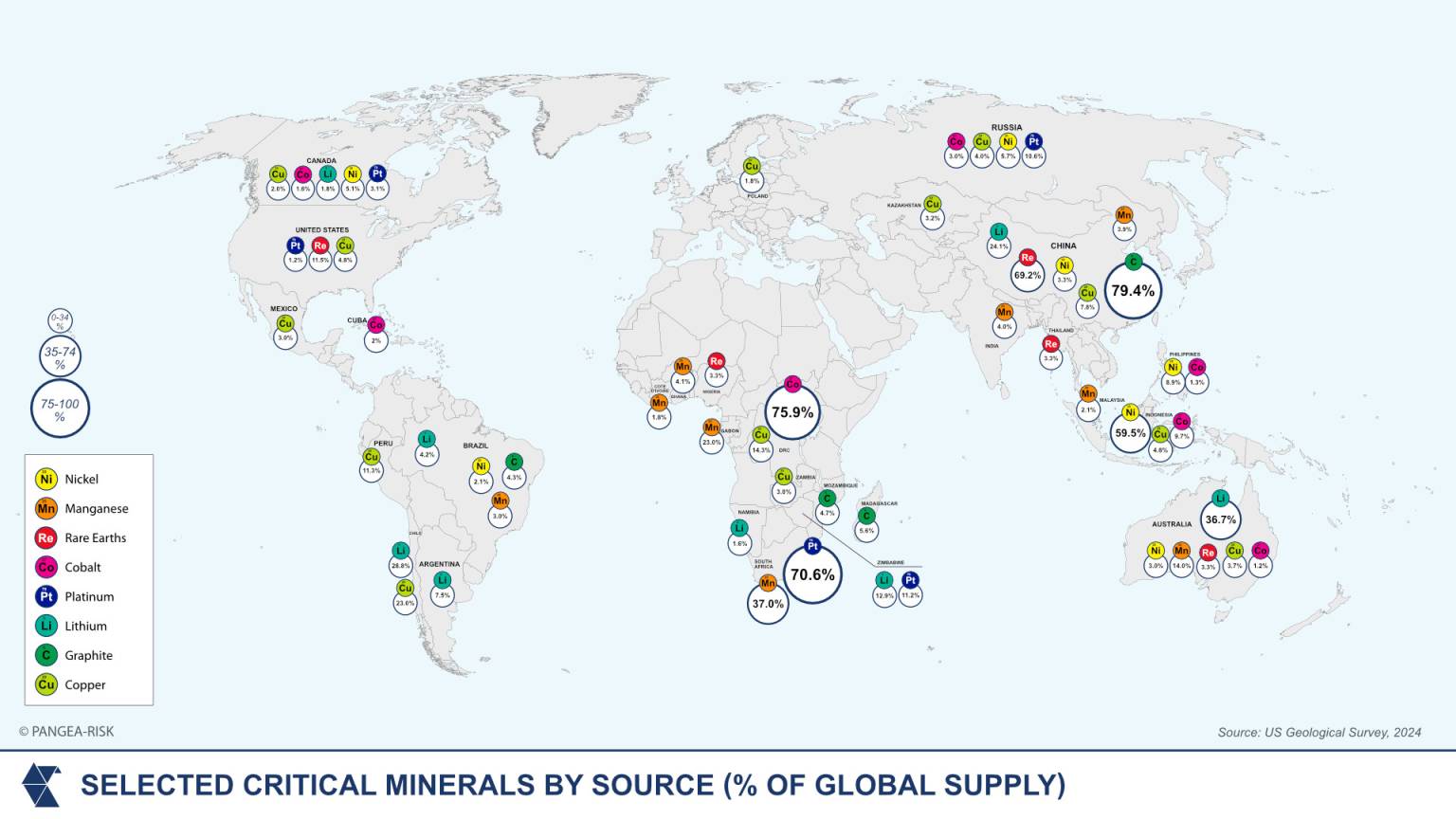

Industry exposure within the CPRI market is also evolving in response to shifting global dynamics. According to recent surveys, financial institutions remain the largest sector reliant on CPRI, closely followed by oil and gas. However, sovereign risk exposure has declined, overtaken by rapidly growing interest in renewable energy. The energy transition is driving unprecedented capital flows into solar, wind, and hydro projects across frontier and emerging markets while also driving interest in the minerals that undermine the requisite technologies. Insurers are responding by increasing line sizes for well-structured, project-level risks, even as they reduce headline limits tied to broader national risk considerations.

Morocco stands out in North Africa’s renewable energy sector, targeting over 50 percent renewable electricity generation by 2030. Its stable policy environment, high-profile projects like the Noor Ouarzazate solar complex, and multilateral financing attract significant foreign investment. This pipeline of well-supported projects makes Morocco’s renewables sector particularly appealing for CPRI coverage focused on long-term, manageable risks.

Similarly, in Southeast Asia, where rapid urbanisation is fuelling demand for infrastructure development, CPRI also benefits from sector-based opportunities. Countries such as Vietnam, Indonesia, and the Philippines are investing heavily in transport, utilities, and urban projects. Multilateral development banks, including the Asian Infrastructure Investment Bank (AIIB), are providing critical financial backing that mitigates political risks, making these projects more insurable and attractive to investors. In sub-Saharan Africa, agribusiness is poised for growth, supported by favourable climate conditions, a youthful labour force, and rising global food demand. Countries including Kenya, Ghana, and Nigeria are pursuing policies to improve food security and draw investment into agriculture. The African Development Bank’s ‘Feed Africa’ strategy aims to transform the continent into a major food producer by investing in technology, irrigation, and value chains. Complementary initiatives such as the Africa Risk Capacity (ARC) provide insurance against climate shocks, enabling governments to respond swiftly and prevent humanitarian crises. For CPRI providers, agribusiness offers promising opportunities to support sustainable projects with robust risk mitigation. Overall, the CPRI market is transitioning from broad expansion to more focused, data-driven growth. As sovereign coverage contracts, demand rises for targeted, sector-specific insurance that aligns with the unique domestic political realities and societal needs across emerging markets. It is clear that while premium growth may slow in some areas due to softer global trade, demand is rising in new regions, industries, and transaction types. The move away from general sovereign coverage toward more targeted project- and sector-specific insurance reflects a pragmatic response to an increasingly fragmented and politically complex global environment.

Similarly, in Southeast Asia, where rapid urbanisation is fuelling demand for infrastructure development, CPRI also benefits from sector-based opportunities. Countries such as Vietnam, Indonesia, and the Philippines are investing heavily in transport, utilities, and urban projects. Multilateral development banks, including the Asian Infrastructure Investment Bank (AIIB), are providing critical financial backing that mitigates political risks, making these projects more insurable and attractive to investors. In sub-Saharan Africa, agribusiness is poised for growth, supported by favourable climate conditions, a youthful labour force, and rising global food demand. Countries including Kenya, Ghana, and Nigeria are pursuing policies to improve food security and draw investment into agriculture. The African Development Bank’s ‘Feed Africa’ strategy aims to transform the continent into a major food producer by investing in technology, irrigation, and value chains. Complementary initiatives such as the Africa Risk Capacity (ARC) provide insurance against climate shocks, enabling governments to respond swiftly and prevent humanitarian crises. For CPRI providers, agribusiness offers promising opportunities to support sustainable projects with robust risk mitigation. Overall, the CPRI market is transitioning from broad expansion to more focused, data-driven growth. As sovereign coverage contracts, demand rises for targeted, sector-specific insurance that aligns with the unique domestic political realities and societal needs across emerging markets. It is clear that while premium growth may slow in some areas due to softer global trade, demand is rising in new regions, industries, and transaction types. The move away from general sovereign coverage toward more targeted project- and sector-specific insurance reflects a pragmatic response to an increasingly fragmented and politically complex global environment.

A global environment under pressure

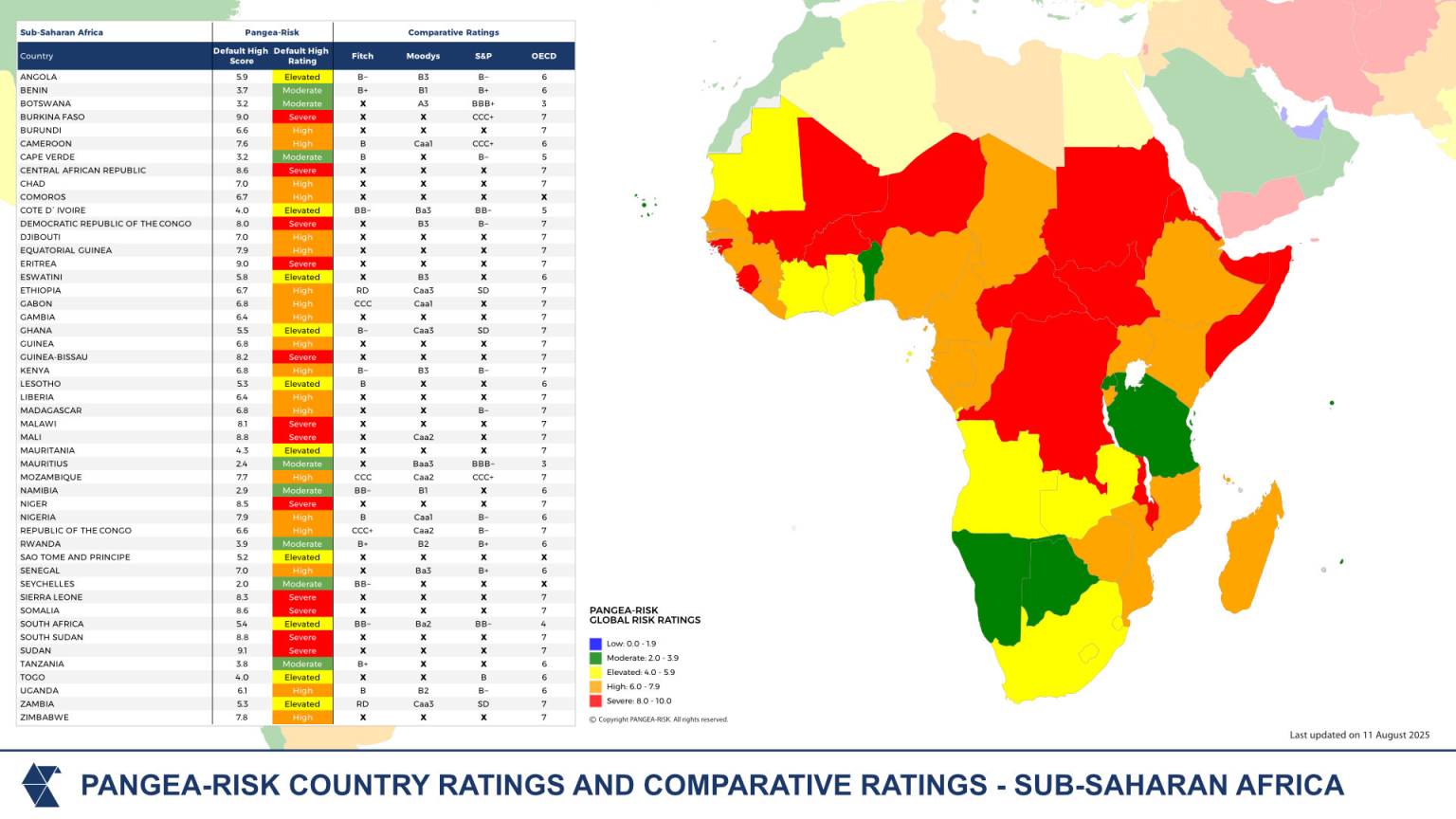

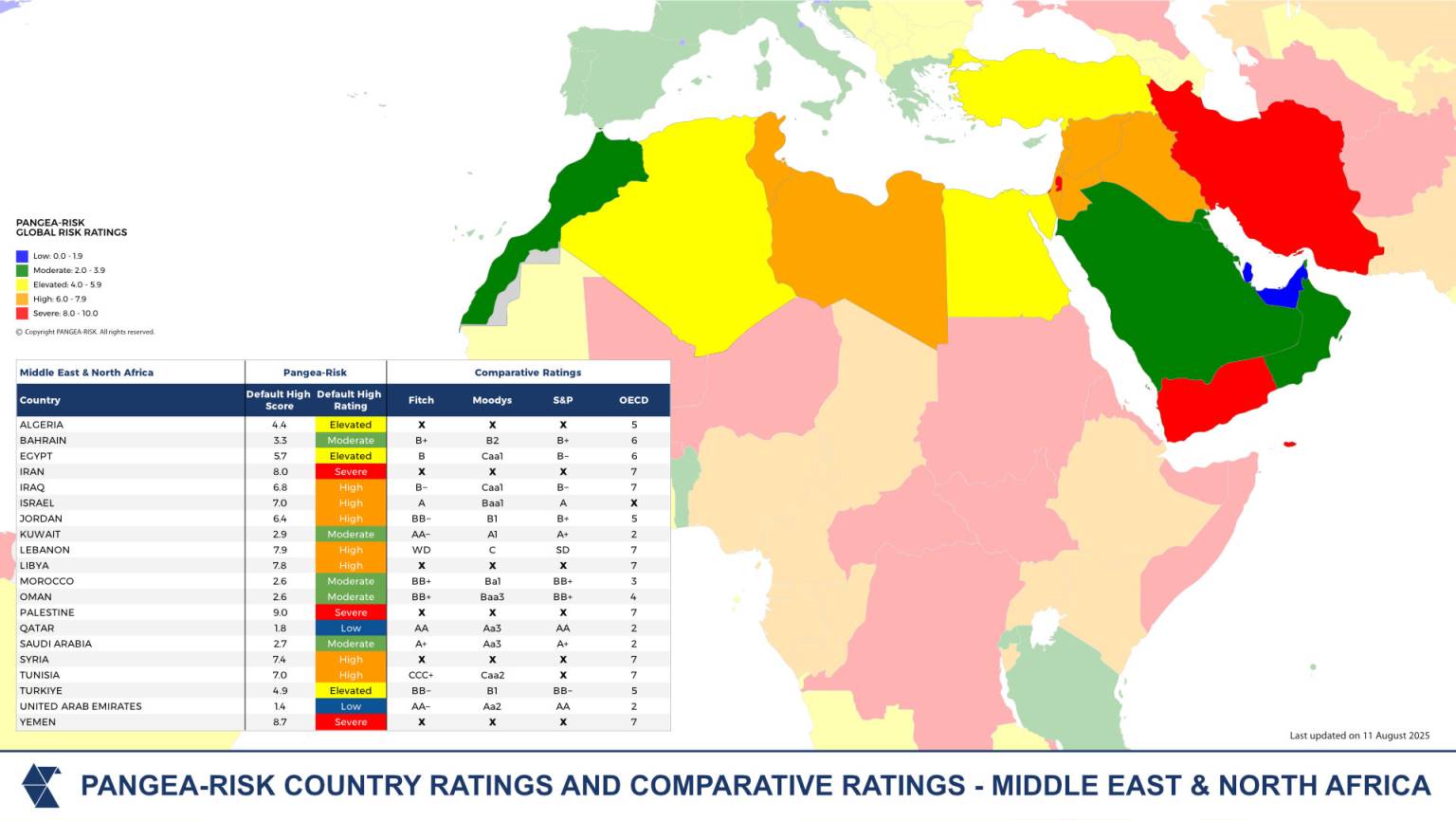

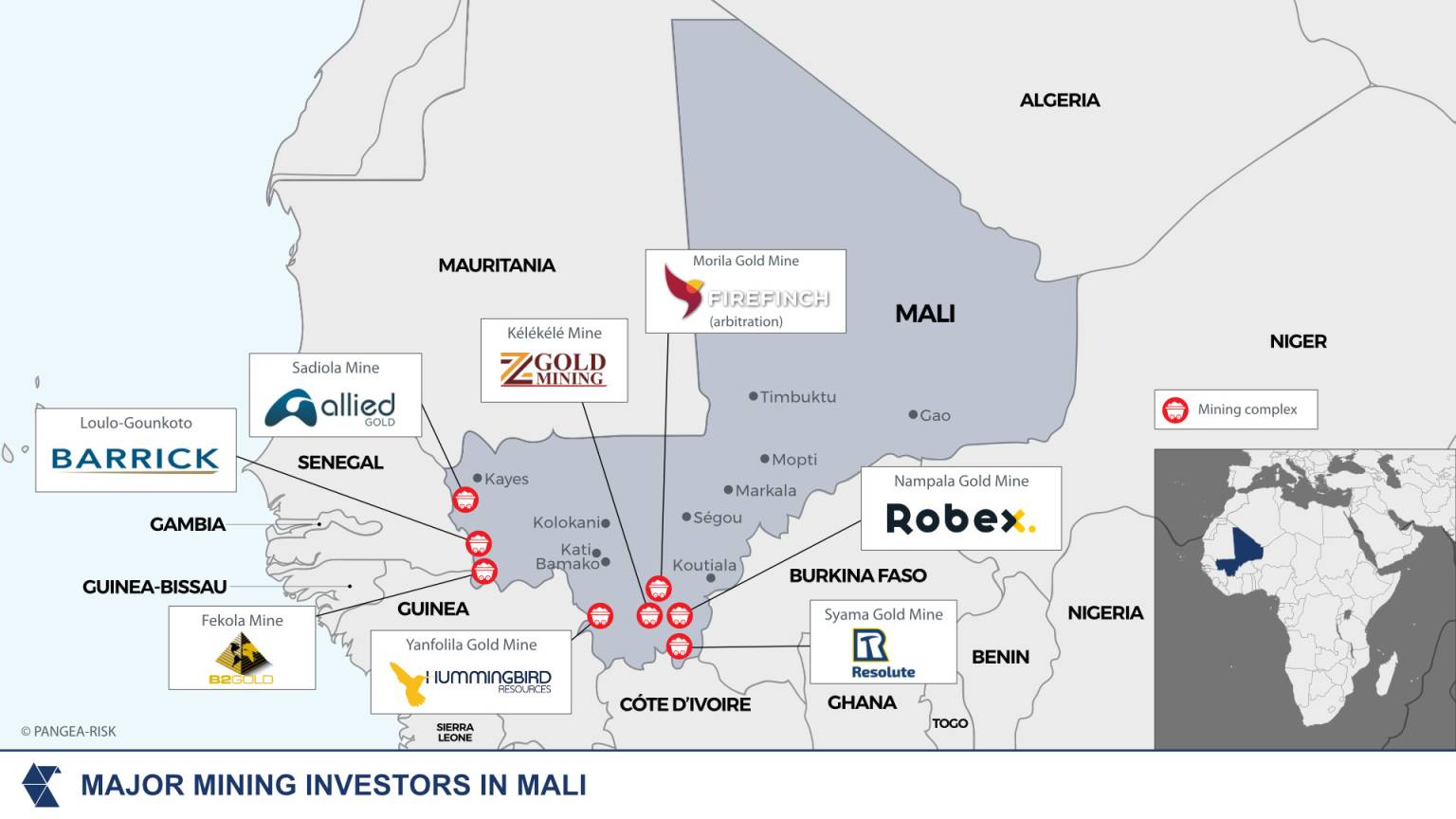

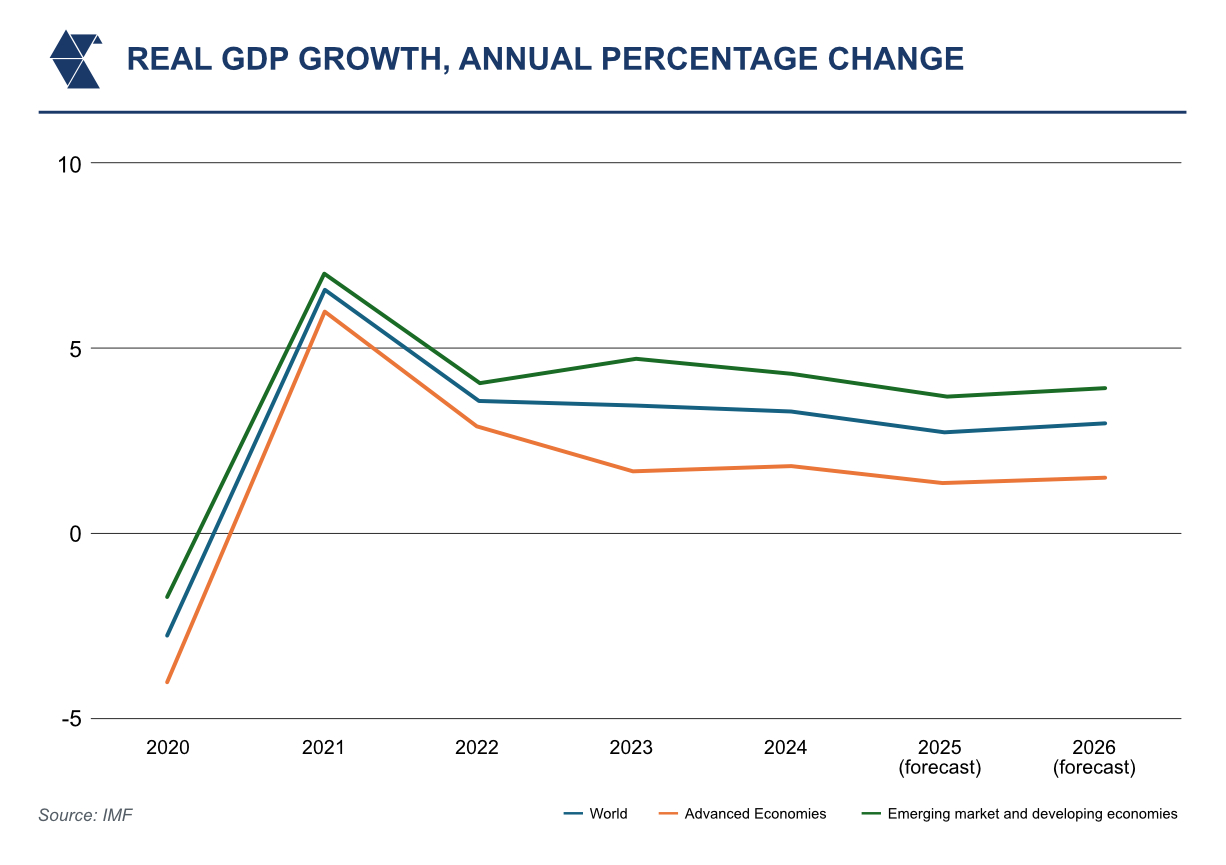

While opportunities in the CPRI market remain clear, a complex set of global pressures continues to shape, and in some cases disrupt, market trajectories. The geopolitical environment in 2025 has been defined by aggressive use of tariffs, volatile energy markets, and fracturing global alliances, creating heightened uncertainty for insurers and investors alike. Trade protectionism has emerged as a particularly potent risk driver. The US administration’s imposition of secondary tariffs on countries importing Russian oil, including a 25 percent tariff on Indian goods, exemplifies a new and precarious escalation, with many countries still reeling from President Trump’s Liberation Day duties. These measures threaten to disrupt longstanding trade relationships and signal a more interventionist use of tariffs as foreign policy instruments. Broader US reciprocal tariffs on steel, aluminium, and other imports from China, Vietnam, and the EU have already caused construction delays, cost overruns, and supply chain disruptions. Regulatory barriers and disputes over strategic infrastructure, including the Panama Canal, further complicate operational planning for multinational corporations, increasing demand for insurance coverage against trade disruption, expropriation, and contract frustration. Fragmented supply chains, shifting supplier bases, and the reallocation of production to mitigate trade risks require insurers to adopt more targeted, country- and sector-specific underwriting approaches. Sudden regulatory changes further amplify the unpredictability of current operating environments. Multinational corporations are exposed to potential forced divestitures, contract renegotiations, and project delays, which, in turn, create higher claims uncertainty and reduce insurers’ appetite for broad sovereign risk coverage. In Sub-Saharan Africa, political instability and rising resource nationalism have intensified market risk. Military takeovers in Mali, Burkina Faso, and Niger have led to sweeping reforms, nationalisations, and coercive tactics targeting foreign-owned mining assets. In Mali, the detention of Barrick and Resolute Mining executives, multi-million-dollar settlement demands, and the seizure of USD 245 million in assets illustrate the severity of intervention. Burkina Faso has expropriated major gold mines and unilaterally increased royalty rates, while Niger has nationalised a French-operated uranium mine and pressured Chinese oil firms. Elsewhere, Tanzania’s higher royalty regime and Zimbabwe’s lithium export ban, underscore a broader pattern of governments seeking greater control over strategic resources.  At the same time, global growth is projected to slow to 2.3 percent in 2025, nearly 0.5 percentage points below early-year expectations, with advanced economies expected to achieve just 1.3 percent growth. Emerging markets, long a source of faster expansion, are also experiencing significant deceleration, with growth outside Asia declining from 6 percent in the 2000s to around 3.7 percent in 2025. Slower trade, muted investment, elevated debt levels, and persistent inflation constrain fiscal and monetary flexibility, limiting the capacity for stimulus. These trends threaten employment growth and per capita income convergence, further exacerbating political and economic volatility.

At the same time, global growth is projected to slow to 2.3 percent in 2025, nearly 0.5 percentage points below early-year expectations, with advanced economies expected to achieve just 1.3 percent growth. Emerging markets, long a source of faster expansion, are also experiencing significant deceleration, with growth outside Asia declining from 6 percent in the 2000s to around 3.7 percent in 2025. Slower trade, muted investment, elevated debt levels, and persistent inflation constrain fiscal and monetary flexibility, limiting the capacity for stimulus. These trends threaten employment growth and per capita income convergence, further exacerbating political and economic volatility.

Article Info

Related Articles

Payments +2

Payments +2Issue 05 – Fine Print: Looking Beyond the Headlines

Scott Sanchon, Trade Treasury Payments “We live in an age that rewards the headline.” Every...

Cash Management +6

Cash Management +6TTP Studios, on the record

By: James Dorman and Deepesh Patel A comfortably-furnished room under the railway arches of Central...

Bills of Lading +5

Bills of Lading +5Beyond the headlines: A foreword to the fine print of global finance

A note from the editors We live in an age that rewards the headline. Every...

Bills of Lading +2

Bills of Lading +2How Switzerland gave electronic documents of title the force of law

By: Tim Staheli Geneva and Zug together account for an estimated 35 per cent of...

Stay Ahead of the Curve

Get exclusive insights, expert analysis, and breaking news on liquidity and risk management, delivered to your inbox

Article Info

Stay Updated

Get the latest insights on trade finance, treasury management, and global payments delivered to your inbox.

Join 25,000+ professionals. Unsubscribe anytime.