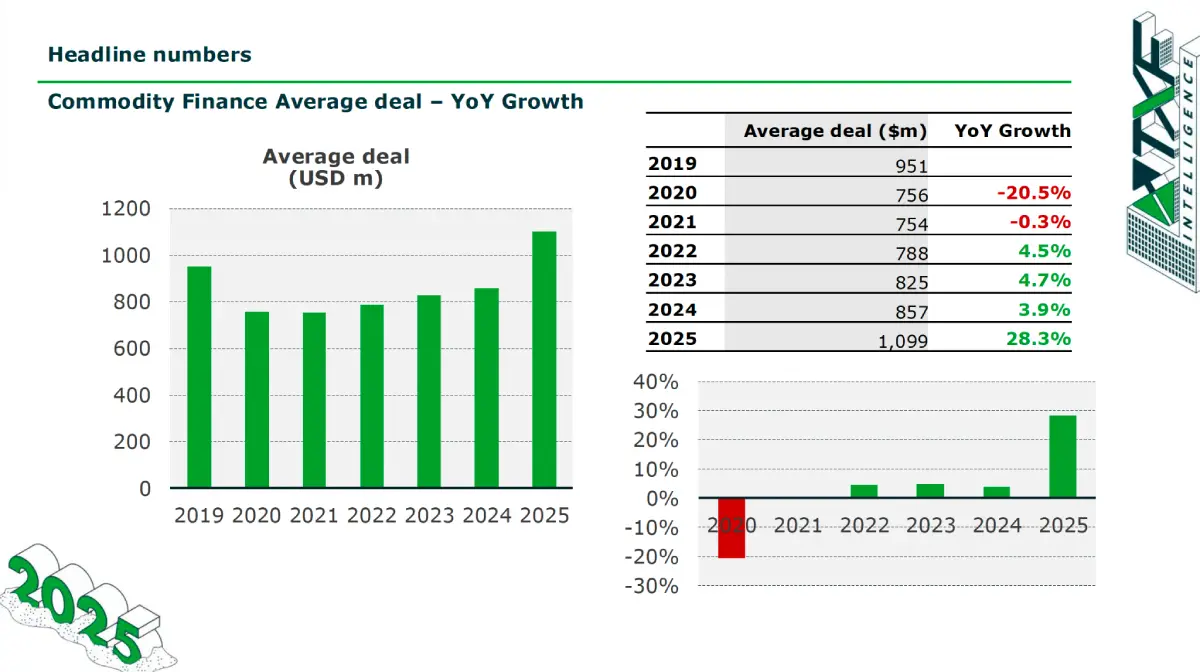

For the first time in history, the average commodity finance deal has crossed the $1 billion mark.

That striking figure alone is a clear sign that what was once a market defined by smaller, more fragmented transactions is now consolidating into larger structures. But there are other interesting findings when you explore the data more.

According to TFX’s Commodity Finance Data Full Year 2025 Report, overall commodity finance volumes have grown by up to 25% over the year, from $134.5 billion in 2024 to $168.1 billion in 2025. Despite that strong growth in value, however, the number of deals closed fell from 157 in 2024 to 153 in 2025. The number of “mega-deals” (those of $2 billion or more), however, increased over that same time frame from a total number of 17 to 22, accounting for more than half of the overall market volume.

To get to the bottom of this “flight to size” and explore some of the implications that it will have for the commodities industry and beyond, TFX and Trade Treasury Payments (TTP) have launched a series of global commodity finance roundtable discussions.

The first, held in London in April, brought together 5 industry leaders under Chatham House rules in an initial conversation that ranged from the impact of Gulf tensions and security concerns to new capital rules that influence sectors.

Diverse concerns are rising from different perspectives. Financial institutions tend to raise questions about competitiveness and the viability of traditional models, while commodity traders point to the significant growth in demand for funding sources and diversification.

Banks have a new perspective

While there were many different perspectives, one consensus quickly made at the London roundtable is that the market is bullish. “It is a lot bigger … if you look at the last five, ten years,” an agriculture services participant said, while another participant added that “the question is not whether the market is growing, but who is growing with it.”

While flat deal counts alone may seem to suggest that banks are stepping back from financing commodity traders, the reality may be that they are prioritising a different kind of client relationship.

“We need to cover the larger traders with more creativity, more products… we need to be in the advisory rather than just slapping additional balance sheets,” a bank participant of the roundtable said. The data indicate that banks may indeed be prioritising these larger clients.

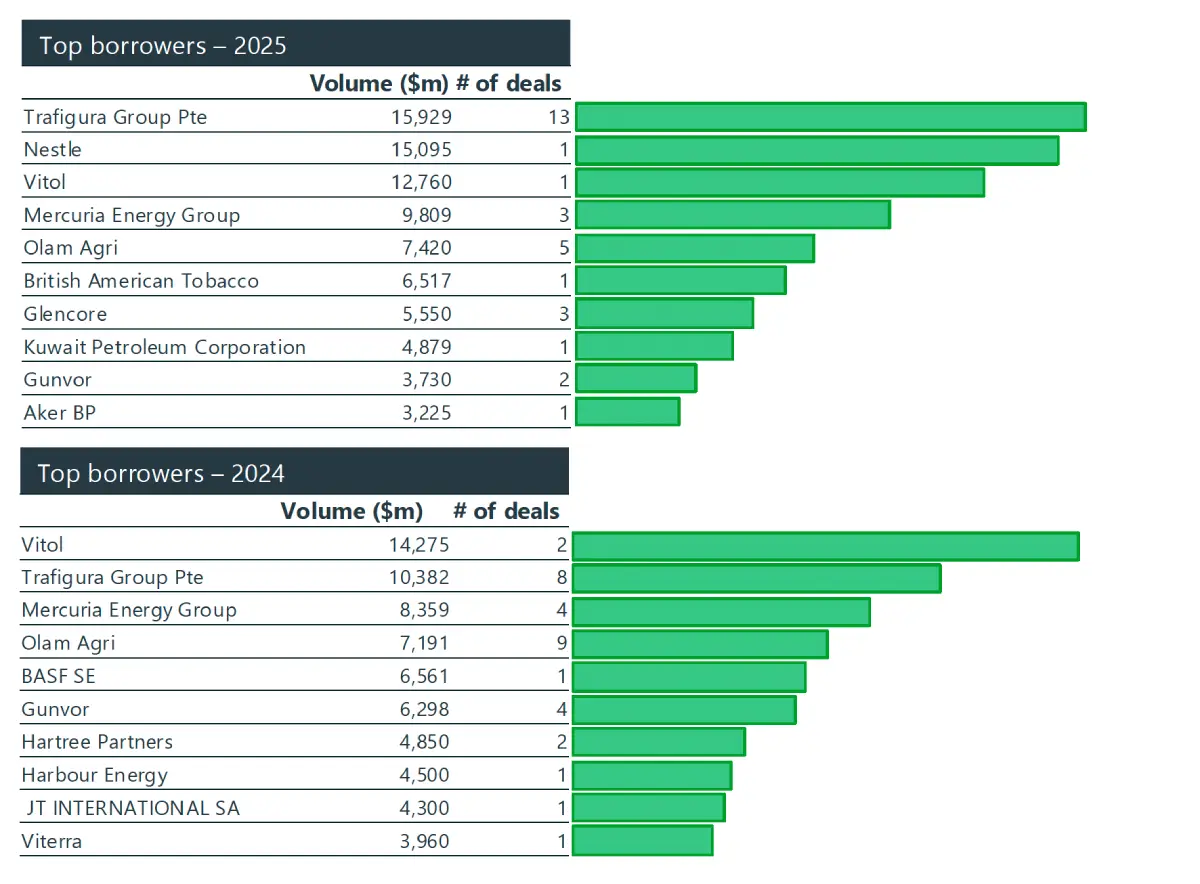

The top three borrowers alone – comprising Trafigura Group Pte, Nestle, and Vitol – collectively raised over $43 billion in 2025, up from just $33 billion the year before (when Vitol, Trafigura Group Pte, and Mercuria Energy Group held the top spots). In 2025, Trafigura alone accounted for nearly $16 billion of this, spread across 13 deals, while Nestle topped $15 billion in just a single one.

Why such a pronounced contraction? The worsening geopolitical situation, with tensions and even direct conflicts more pronounced than in the past, may be to blame, especially as “banks have become more and more risk-averse,” the bank participant said.

But it is also true that larger deals with larger clients often make commercial sense for the banks. They are more reliable and have greater borrowing potential, which has a tendency to yield the returns that banks seek. “When your creditworthiness improves, it opens up to longer tenors, it opens up to bigger amounts, and it opens up new markets, new sets of investors,” the bank participant added.

Capital follows certainty, commodities follow necessity.

Capital, by its nature, relies heavily on certainty and predictable margins, performing its best work when the risks involved can be clearly defined, and the outcomes modelled well in advance. Commodities, on the other hand, are driven by necessity. Even if there is tremendous uncertainty in the world, humans still need food and energy.

This creates a fundamental tension at the heart of commodity finance. The assets being financed need to move, and are therefore inherently exposed to price swings and geopolitical shocks. “The only concern is the uncertainty,” one of the agri expert participants said. “That’s the only thing that we have.”

“What does that mean?” one of the bank participants asked. “Prices are higher, which means deal sizes are bigger.”

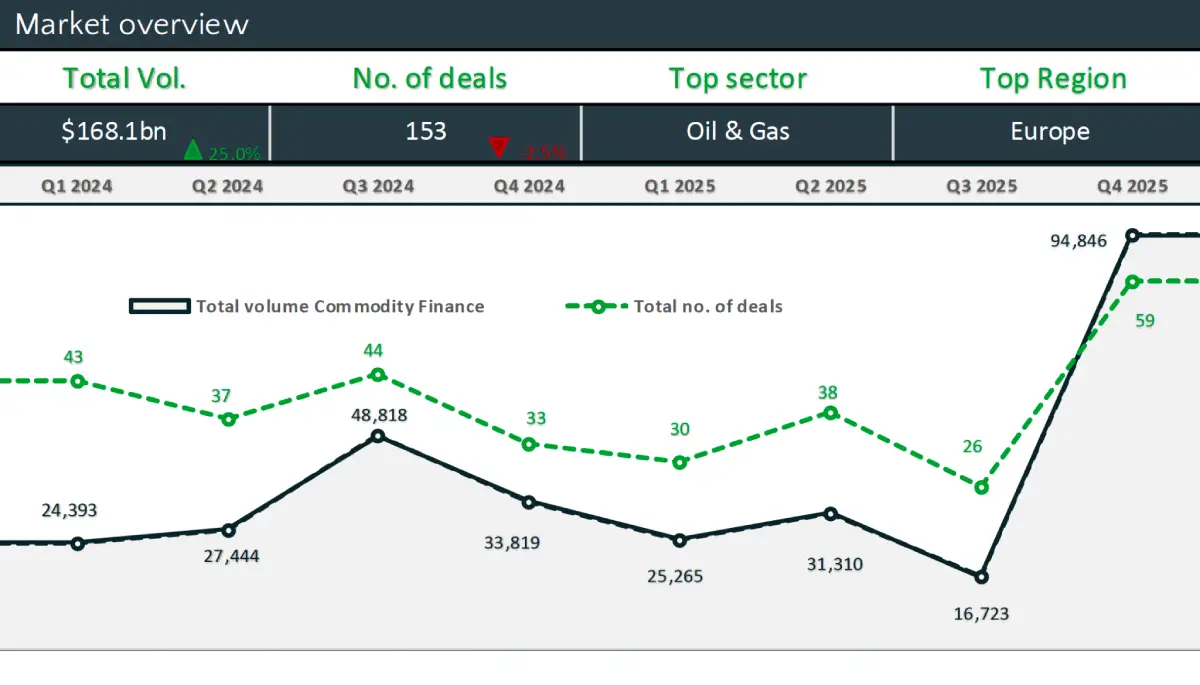

Perhaps this is why the data from TFX’s report demonstrates an unprecedented concentration of mega-deals closed in Q4 2025. The increase of approximately $94.8 billion in a single quarter, more than the first three combined.

“We are pricing for uncertainty,” the bank participant added, “but uncertainty can not be priced. Risk can be priced, but at the moment we don’t know what those risks are.”

Moving forward, commodity companies must maintain their relationships, since the current environment might be an illusion of something bigger. The demand for commodities remains, but might shrink due to geopolitical tensions and supply chain disruptions. When the market reveals the new structure from this shift, the capital will follow.

The market no longer clears for everyone.

One takeaway from TXF’s 2025 data and the London roundtable could be that the commodity finance market is functioning extremely well… at least for the small handful of large players at the very top of the market. Find yourself outside of this exclusive club, and the market may not be serving you as well as it once did.

While mega-deals of $2 billion now account for more than half of overall volumes, the lower bracket, such as smaller traders and agricultural companies, generated only 1.7% of the total proportion, with only 31 deals.

One of the commodity professionals at the roundtable noted the tumultuous journey that small traders have been on over the past two decades. “SMEs – first, obviously, 2008 made a big shake-up in this financing. But then, definitely after COVID, it never returned,” they said.

In the past, smaller banks generally financed SMEs with limited credit and financial data. But after COVID, these higher-risk investments have largely gone under, as companies either restructured or exited after losses.

It seems then that the big banks are more willing to make a billion-dollar investment in a major supply chain company than to underwrite even 20 smaller submissions independently, taking on the work with every single one of them. “It’s a lot easier to go to your compliance team and get approvals for a single client,” one of the bank participants said. “I’d rather finance just one company than a bunch of different companies in these different places.”

The longer-term consequences of the current changes taking place in commodities markets have the potential to be severe and could extend well beyond the markets themselves. “Commodities will be the first thing to go,” the economist at the roundtable said, “and that will undermine economic security in Europe.”

Financing commodities companies at the smaller end of the market will keep the market moving forward sustainably. If the financing gap at the smaller tier persists, then the supply chain that depends on mid-tier and low-tier traders will remain fragile and ultimately disappear from the market.

The market’s $1 billion average deal is a milestone. But ensuring commodity financing spreads throughout the market is more important to keeping the economy competitive and sustainable.