Capital demand across regions

The global private credit market is set for continued expansion in 2026, driven by rising capital demand and a shifting investment landscape, says the Moody’s 2026 Global Private Credit Outlook. The report highlights key trends shaping this growth, including a transition from traditional corporate lending toward asset-backed finance (ABF), increasing innovation to meet liquidity demands, and evolving regulatory scrutiny.

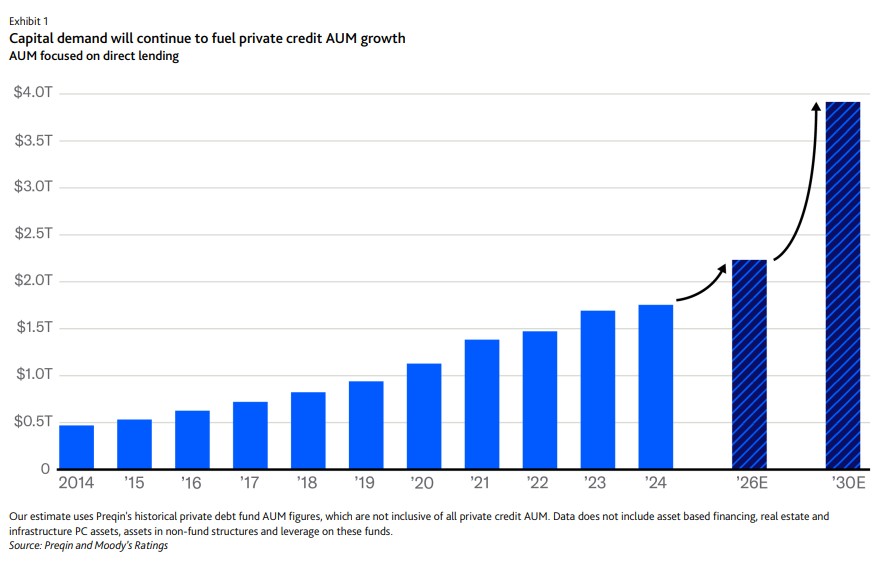

The report says that assets under management (AUM) in private credit are expected to surpass $2 trillion in 2026, with projections approaching $4 trillion by 2030.

While corporate direct lending remains the dominant segment, the market is witnessing a significant shift toward ABF, which is gaining traction as a core funding mechanism.

This shift shows a wider variety of asset classes and locations, including Europe, the Middle East, Africa (EMEA), and Asia-Pacific (APAC).

Mergers and acquisitions (M&A) and leveraged buyout (LBO) activity are anticipated to escalate, intensifying competition among lenders but simultaneously expanding funding opportunities.

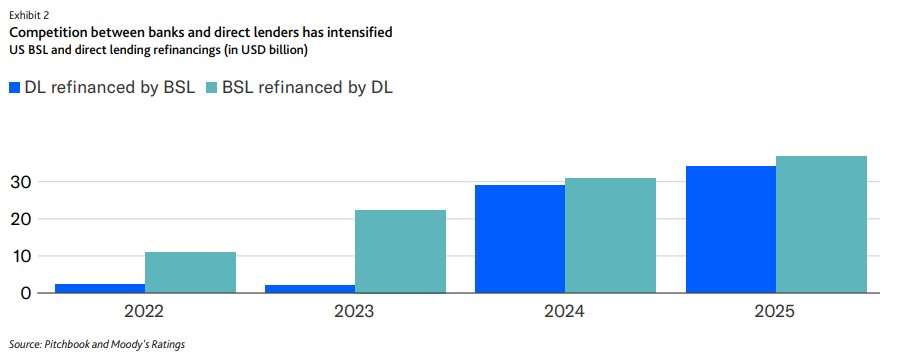

The competitive space is further complicated by the interplay between direct lenders and the broadly syndicated loan (BSL) market, which has reclaimed market share as interest rates have eased.

The recent regulatory relaxation in the United States, notably the December 2025 waiver of certain leverage limits by the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC), is expected to influence deal leverage multiples and lending dynamics.

Capital demand across regions

Europe’s private credit sector is expected to grow faster than the United States’, with European assets forecast to reach between $800 billion and $900 billion by 2028.

Capital demand is intensifying as Europe faces significant funding requirements, particularly in critical infrastructure and defence sectors. Private credit is positioned to provide longer-term, tailored financing solutions where traditional funding sources are insufficient.

Meanwhile, the APAC region, which remains predominantly reliant on bank intermediation, is set for growth supported by a relatively low base, increasing domestic financing needs, and investors’ pursuit of yield and diversification.

The region’s outlook remains positive due to ongoing economic growth, improved regulations, and a rising need for flexible financing outside of banks. Australia, Japan, and India are key markets for private credit growth.

Asset-backed finance to lead growth

Alternative asset managers are increasingly targeting newer and more diverse pools of assets, including consumer loans and data infrastructure credit. Partnerships are playing a pivotal role in accelerating asset origination, particularly as banks face constraints in certain lending activities. This reliance on partnerships, while beneficial for deal flow, introduces underwriting risks due to reduced direct control.

The report shows the growing importance of ABF deals’ structural protections and lender oversight to mitigate downside risks. Less cyclical sectors, such as digital infrastructure, are expected to perform more resiliently given the essential nature of their services.

Expansion of asset classes supports securitisation growth

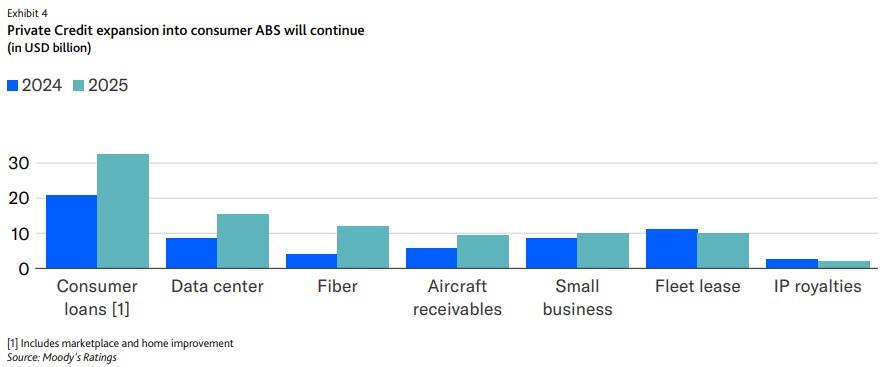

Private credit’s footprint in securitised products continues to widen, focusing on sectors where higher yields compensate for asset riskiness amid compressed spreads. Key asset classes include consumer lending, residential and commercial mortgages, and nontraditional assets.

Private credit’s role in financing capital-intensive sectors, such as digital infrastructure, is surging. The demand for data centres, fibre networks, and related technology equipment is driving securitisation issuance volumes higher.

For instance, securitisation issuance for data centres increased by 80% in 2025 compared to the prior year, with private equity-backed firms frequently sponsoring these transactions.

Innovation to address growing liquidity demands

Liquidity pressures remain a defining theme in private credit, prompting sponsors and issuers to adopt increasingly innovative financing solutions. The convergence of private and public markets has led to looser covenant structures and the proliferation of payment-in-kind (PIK) features. Back-leverage, often structured as PIK debt, enables sponsors to extract dividends or redeploy capital without increasing leverage at the operating company level.

Financial innovation involves the growing use of net asset value (NAV) lending, rated fund structures, and evergreen funds. Evergreen funds, known for their liquidity, are changing distribution channels, but also bring maturity transformation risks not typically found in private markets. The surge in private wealth has led to new managers entering the field and an increase in products with periodic liquidity, raising complexity and liquidity risk.

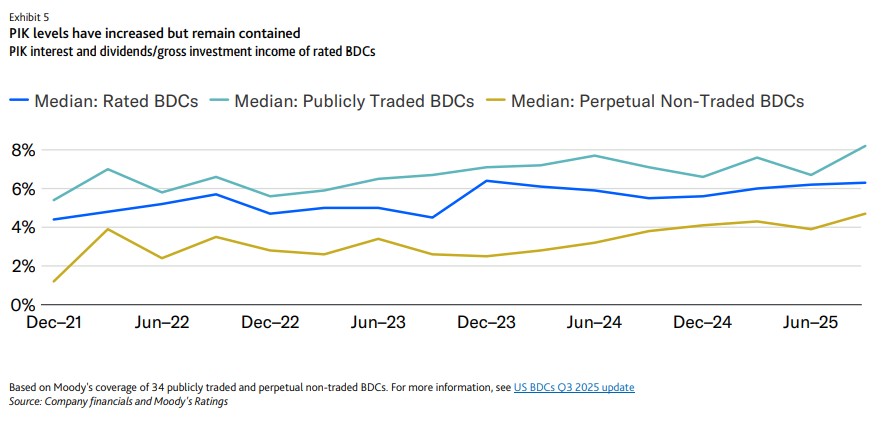

Monitoring PIK income trends in business development companies (BDCs) offers early indicators of asset quality. While PIK levels have been rising slowly, they remain low and account for only a small portion of gross investment income.

Regulatory guardrails remain limited, but the transparency focus grows

Regulators worldwide support the role of private credit in bridging capital funding gaps. They are focused on capital formation while maintaining some regulations to facilitate growth.

The Main Street retail investor is expected to become increasingly important, with regulatory proposals in the United States aimed at facilitating retirement account investments in private credit and private equity.

European regulators are working to improve access to private markets and increase transparency. The UK’s Solvency II reforms and updates to the European securitisation framework are designed to encourage insurers to invest in private credit.

The Bank of England is also conducting scenarios to evaluate systemic risks associated with the rapid growth and lack of transparency in this sector.

In the United States, banks have increased lending to non-depository financial institutions (NDFIs), reaching $1.2 trillion by mid-2025, with approximately $300 billion directed to private credit providers. Enhanced disclosure requirements for these loans have been introduced to improve market transparency.

Rising risks amid growing interconnectivity

Innovation has fueled the growth of private credit, but it has also created structural complexity and increased interdependencies.

Deepening ties between private credit funds and traditional financial institutions could amplify contagion risk during economic downturns.

The growing participation of individual investors, though currently a small share, may increase market volatility compared to the traditionally stable institutional capital base. Such volatility could elevate the cost of capital precisely when capital availability is most critical.

Read the full report here.

Article Info

Related Articles

Digital Trade +2

Digital Trade +2Trade digitalisation accelerating: what’s next?

By: James Dorman The momentum behind the digitalisation of trade and trade finance is undeniable....

Risk Management +2

Risk Management +2We are in a new G2 world – here is a way forward for the rest of the world

TTP’s Global Advisory Panel member, Chris Southworth argues that the old economic order has quietly...

Correspondent Banking +4

Correspondent Banking +4The last correspondent: how de-risking left a sovereign nation distributing dollars by blockchain

De-risking has removed most correspondent banking relationships across the Pacific and parts of Eastern Europe,...

Cash Management +2

Cash Management +2No ownership, no profit: How Murabahah keeps trade finance honest

By: Iqbal Karmally In Islamic trade finance, the bank does not lend — it buys...

Stay Ahead of the Curve

Get exclusive insights, expert analysis, and breaking news on liquidity and risk management, delivered to your inbox

Article Info

Stay Updated

Get the latest insights on trade finance, treasury management, and global payments delivered to your inbox.

Join 25,000+ professionals. Unsubscribe anytime.