TTP heard from Global Advisory Panel member Dr Robert Besseling, CEO of Pangea-Risk.

Following renewed US and Israeli airstrikes, Iran has broadened the battlefield to include Gulf states, targeting US military facilities and civilian infrastructure to raise the cost of further strikes and compress the escalation timeline. Iraq remains the primary proxy escalation channel, with Iranian-aligned armed groups positioned to sustain pressure on US bases, while the Houthis expand maritime risk and Hezbollah exercises calibrated restraint to preserve deterrence. Concurrent disruption across Gulf aviation hubs and the Strait of Hormuz is tightening energy and logistics systems, with sustained transit instability or repeated strikes carrying the risk of broader regional escalation and systemic energy market shock.

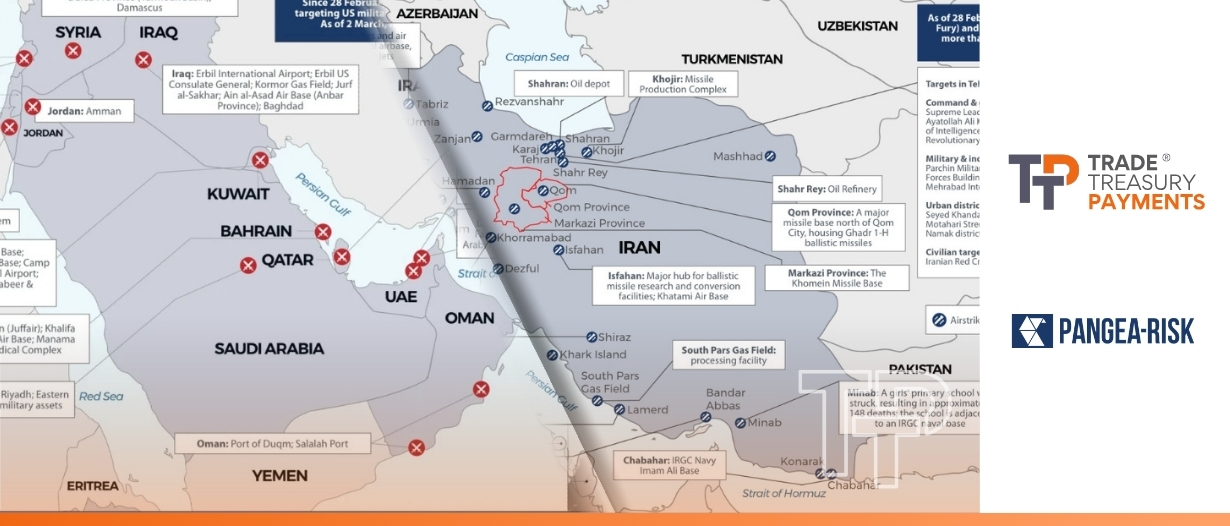

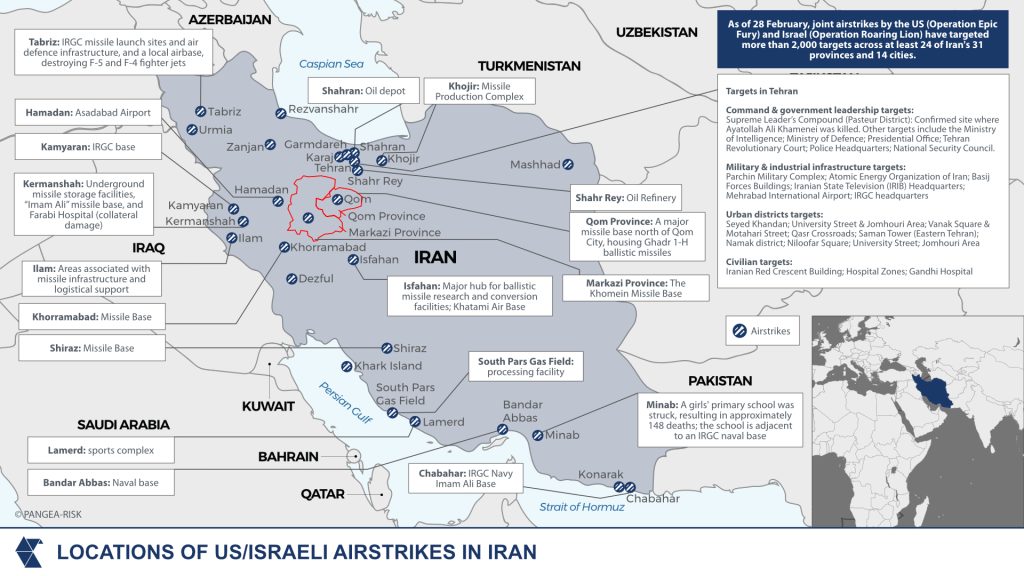

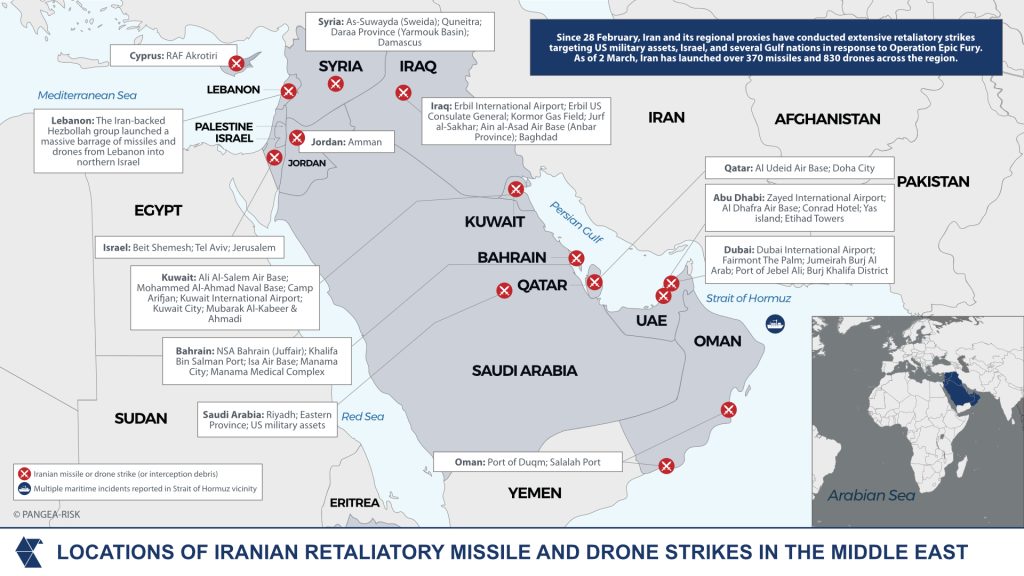

On 28 February, the United States (US) and Israel launched a joint military operation against Iran, striking nuclear facilities, military command infrastructure, and senior leadership compounds across more than 20 provinces. Supreme Leader Ali Khamenei was killed in a strike on his compound in Tehran, along with the defence minister, the Islamic Revolutionary Guard Corps (IRGC) commander, and several members of the defence council. This comes as indirect nuclear negotiations in Geneva, mediated by Oman, were ongoing, with Israel preparing for possible escalation even as diplomacy continued. Iran’s retaliation has been immediate, geographically dispersed, and qualitatively different from prior escalatory rounds: ballistic missiles and drones struck Bahrain, Kuwait, Qatar, the United Arab Emirates (UAE), Saudi Arabia, Jordan, and Iraq in a simultaneous salvo that targeted both US military installations and civilian aviation infrastructure across the Gulf Cooperation Council (GCC).

The conflict has moved beyond the bilateral confrontation that characterised the Twelve-Day War of June 2025 and has drawn the GCC states into its operational perimeter as direct targets. Iran’s identification of Gulf governments as cobelligerents (reflected in its targeting choices) has forced a strategic reckoning that GCC had spent years attempting to avoid. Simultaneously, Iran’s proxy networks across Iraq, Yemen, and Lebanon are under pressure to activate, while the Strait of Hormuz faces its first effective disruption since the waterway’s modern role in global energy trade was established. The commercial consequences are spreading across the oil, liquefied natural gas (LNG), aviation, and shipping markets, with the risk of sustained infrastructure destruction in the Gulf’s energy-producing heartland posing the most severe downside scenario.

PANGEA-RISK assesses that Iran’s strategy of widening the conflict to Gulf states and activating selective proxy pressure is designed to force rapid US recalibration.

Iran hedges on the Gulf to break the strike cycle

Shortly after the US and Israeli airstrikes, Iran expanded its retaliation beyond Israel and directed missile and drone operations at US military facilities in Bahrain, Qatar, Kuwait, the UAE, and Iraq, alongside civilian infrastructure, including Dubai International Airport. Within the same operational window, airports in the UAE and Qatar experienced temporary disruption, and USlinked facilities in Iraq came under pressure from Iranian-aligned armed groups. The targeting pattern indicates that Iran chose to widen the battlespace at the outset of the escalation, rather than absorb additional strikes and respond sequentially. At least 150 tankers are anchored in Gulf waters, and several large carriers suspended transit through the Strait of Hormuz, including Maersk. A tanker was struck near Oman’s Musandam peninsula, and drone activity affected Oman’s Duqm port.

The leadership house in Tehran after the strikes

The breadth of these effects indicates that Iran is using the first phase of escalation to alter regional risk pricing and to constrain the US operational envelope. In previous cycles, Iran often relied on calibrated proxy action or geographically contained retaliation. In this phase, Iran moved directly against US basing architecture and against infrastructure in states that host and enable US military operations. The intent is to pre-empt a sustained strike campaign on Iranian territory by immediately altering the cost distribution. By embedding host governments into the operational space, Iran seeks to raise the political and military price of continued US action and to compress the escalation timeline. Iran likely calculates that if Gulf states face direct security and economic exposure at an early stage, they will exert pressure on the US to limit further strikes. The approach aims to elevate deterrence thresholds in a single step. Rather than signalling through gradual escalation, Iran has attempted to redefine the scope of the conflict in the first phase. This is designed to seize the initiative and to deny the US the option of controlled, repeat strikes confined to Iranian territory.

Iranian strikes on the main headquarters of the US navy’s 5th fleet in Manama, Bahrain

However, direct action against GCC states increases the probability that those governments move from hedging to overt alignment with the US. Saudi Arabia and the UAE have maintained a diversified set of external relationships in recent years, balancing security ties with the US against regional dialogue and economic coordination with other powers. Repeated strikes on airports, military facilities, or strategic nodes reduce the viability of that position. Host governments will prioritise integrated air defence, intelligence coordination, and force protection arrangements. That process deepens operational integration with the US and narrows diplomatic flexibility.

Iran’s leadership appears to assess that early, concentrated escalation offers a higher probability of forcing rapid recalibration in the US government than incremental retaliation. The expected reward is early de-escalation under pressure from exposed regional partners. The countervailing risk is structural consolidation of an anti-Iran alignment across the GCC, accompanied by expanded US basing posture and regional defence integration. If Iranian action remains limited in duration and scope, Gulf governments may seek to contain the confrontation while quietly reinforcing security cooperation. If strikes persist or expand, neutrality strategies will erode, and open alignment could harden.

Iran remains the primary proxy escalation channel

Anti-US protest activity escalated into lethal unrest outside the US consulate in Karachi, Pakistan, with security forces using tear gas and live fire after demonstrators breached the perimeter, and parallel mobilisation occurred outside the Green Zone in Baghdad, Iraq. These events coincided with Iranian-aligned armed groups in Iraq issuing renewed threats against US facilities, and with Yemeni armed actors signalling a return to attacks on shipping and Israel-linked targets. The combined pattern indicates that the conflict’s operational perimeter is expanding through proxy forces and public mobilisation, even as Iran’s ability to coordinate a disciplined, multifront campaign is constrained by leadership disruption and competing priorities.

The most proximate and operationally ready threat to US assets lies in Iraq because armed groups linked to the Popular Mobilisation Forces (PMF) have established attack infrastructure, local access, and an existing political ecosystem that can absorb periodic strikes without requiring cross-border force movement. The likely operational profile is a sustained campaign of rocket, drone, and indirect fire attacks against bases hosting US personnel, combined with attempts to generate political pressure through protest mobilisation around diplomatic sites and security zones. This presents escalation options for Iran because the action threshold is lower in Iraq than in other countries, the attribution environment is more permissive, and the operational tempo can be modulated to test US response boundaries without committing Iran’s regular forces. The main constraint on this pathway is that sustained attacks that produce US fatalities increase the probability of a US strike response that degrades militia infrastructure and forces armed groups into a higherrisk operating mode, which can reduce their ability to sustain tempo over time.

Violent confrontations erupted at anti-US protests in Karachi, Pakistan

On the other hand, the Houthis have repeatedly demonstrated the capacity to disrupt maritime movement through missile and drone activity and to generate broad commercial effects disproportionate to the cost of individual launches. A resumption of attacks in the Red Sea corridor expands the conflict’s operational perimeter away from the Gulf core and reopens a space where escalation can be sustained without requiring direct confrontation with GCC militaries. This channel serves Iranian interests by stretching defensive coverage requirements for the US and partners across multiple maritime approaches. It also carries its own constraints

because sustained interdiction activity invites repeated US and partner strikes on launch infrastructure, which can degrade launch rates and shift the balance toward shorter, more opportunistic attack cycles rather than sustained pressure.

Hezbollah’s posture is the principal uncertainty because it remains the most capable Iranianaligned actor outside Iran, yet it also faces the highest marginal cost of large-scale activation. The available indicators to date point to rhetorical solidarity and political signalling without a decisive shift into sustained, high-volume rocket or missile employment that would trigger a large Israeli response in Lebanon. Hezbollah will weigh the risk of major infrastructure and leadership losses in Lebanon, the limited defensive depth available in a high-intensity exchange, and the possibility that entering the conflict at scale would reduce its capacity to preserve deterrence in the longer term. This restraint also reflects an organisational preference to retain agency over timing and scale, rather than being drawn into a conflict cycle in which escalation control rests with Israel and the US.

The regional protest environment adds a second escalation layer as it affects host-government stability and asset security without requiring a proxy attack to succeed. In Iraq, mobilisation near the Green Zone introduces recurring risk to diplomatic facilities, contractor movement, and government security posture. The Iraqi government’s immediate challenge is operational control over security zones where armed groups and protest networks have proximity advantages. In Pakistan, the Karachi consulate incident demonstrates that protest mobilisation can shift quickly from street demonstrations to attempted breach events against foreign facilities, creating acute security exposure for Western diplomatic and commercial interests. These dynamics increase the likelihood of temporary service disruptions, movement restrictions, and heightened protective security requirements across multiple jurisdictions, even when governments retain overall control.

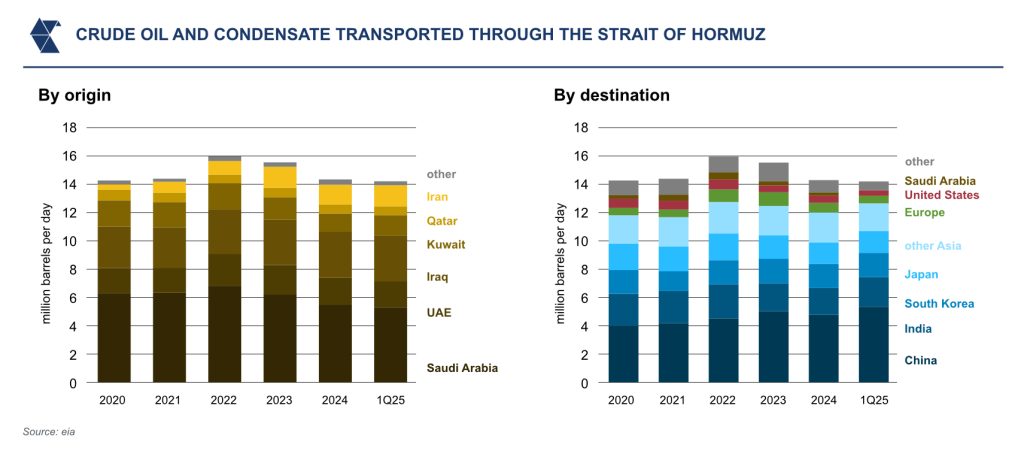

Hormuz instability could reverberate across energy markets

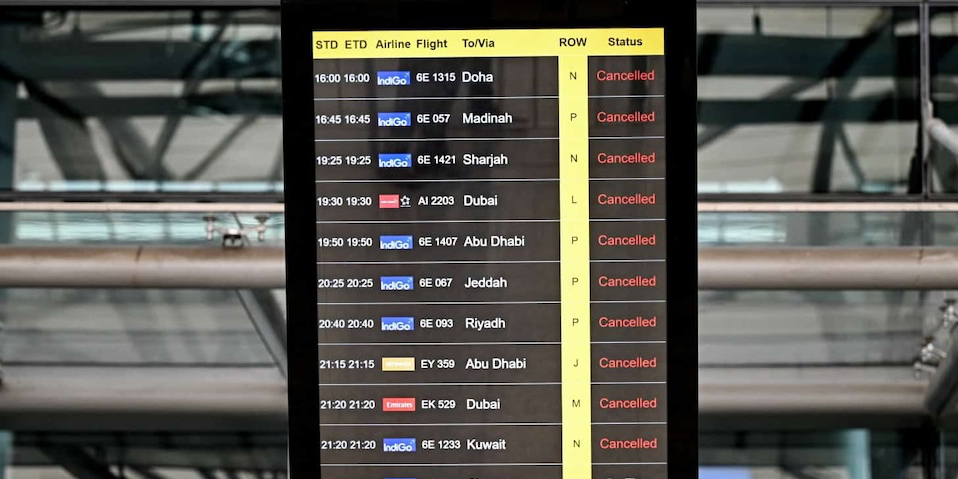

Iranian retaliatory strikes struck Dubai International Airport and Abu Dhabi’s Zayed International Airport directly, killing one person and injuring seven at Abu Dhabi, while Dubai sustained confirmed structural damage to a concourse. Emirates suspended all flight movements indefinitely. Etihad extended cancellations through 2 March. Qatar Airways halted all operations from Doha. Of approximately 4,218 flights scheduled across the Middle East on 28 February, 966 were cancelled, representing 22.9 percent of total scheduled movements. Emirates and Etihad cancelled 38 percent and 30 percent of their respective schedules.

A further 1,400 flights were cancelled for 1 March, with disruption cascading as far as Australia and Brazil as Air India suspended transit routes through Gulf airspace affecting its Europe and US services. The three major Gulf hub carriers typically process approximately 90,000 passengers per day. Dubai and Abu Dhabi alone handled a combined 127.7 million passengers in the prior year. The closure of these hubs, even temporarily, directly undermines the UAE’s positioning as a global aviation and logistics centre, and the economic transmission from this disruption into tourism, hospitality, and trade finance revenues will be measurable within weeks.

In maritime space, the IRGC issued VHF radio broadcasts across the Strait of Hormuz declaring that no vessel was permitted to pass. The UK Maritime Trade Operations and the EU’s naval mission EUNAVFOR ASPIDES both confirmed receipt of these transmissions from commercial vessels operating in the area. Iran had not formally ratified the closure through its Supreme National Security Council as of 2 March, but the de facto operational impact was equivalent to a partial closure: at least eight tankers were idling outside the Gulf of Oman awaiting clarity, LNG tanker traffic from Qatar had materially halted with at least eleven vessels pausing voyages, and major Japanese shipping operators including Nippon Yusen, Mitsui OSK Lines, and Kawasaki Kisen Kaisha had instructed their fleets to stand by in safe waters.

Flight information board reflects cancellation at the Rajiv Gandhi International Airport in Hyderabad

The Strait handles approximately 20 million barrels of oil per day, equivalent to roughly 31 percent of all seaborne crude flows globally. Approximately 84 percent of that volume is destined for Asian markets, with China, India, Japan, and South Korea together accounting for 69 percent of all crude and condensate transiting the waterway in 2024. Qatar’s LNG exports (77 million metric tonnes per annum, rising to 110 million metric tonnes per annum with new capacity in the second half of 2026) are entirely dependent on Strait transit, as are pipeline gas flows from Iran to Türkiye. Oil prices jumped 12 percent within hours of the disruption announcement, with Brent crude, which had settled at USD 72.48 per barrel on 27 February, already up 19 percent year-to-date, facing analyst projections of USD 100 per barrel or above when markets reopened. The bypass infrastructure that Gulf states have developed provides only marginal relief: Saudi Arabia’s east-west pipeline and the UAE’s Habshan-Fujairah pipeline together handle an estimated 15 to 20 percent of normal Strait throughput, covering approximately 2.6 million barrels per day. The world’s spare oil production capacity, held overwhelmingly by Saudi Arabia, the UAE, and Kuwait, transits the Strait by necessity, meaning any closure strands the very buffer the global oil market relies on to absorb supply shocks.

The supply chain cascades extend well beyond crude oil and LNG. Approximately 33 percent of globally traded fertilisers, including sulphur and ammonia, transit the Strait. Iran was the third-largest global urea exporter in 2024, with export volumes of approximately 4.5 million tonnes. Iran has shut down seven urea and ammonia plants since the strikes. Qatar, Saudi Arabia, and Iran collectively account for approximately 25 percent of global nitrogen fertiliser exports, and when Egypt and Bahrain are included, the bloc supplies over one-third of global nitrogen fertiliser trade. CRU data indicate that roughly one-third of global urea exports, 44 percent of sulphur exports, and one-fifth of ammonia exports transit from countries west of the Strait. Gulf Coast urea prices, which were around USD 350 per tonne at the end of the prior week, opened above USD 410 per tonne following the strikes. The transmission of fertiliser prices into agricultural commodity markets lags by four to eight weeks, meaning the food price impact of the current disruption will not be fully visible in consumer data until the second quarter of 2026.

Insight

Over the coming weeks, the direction of the energy market will be determined by duration and strike concentration. If vessel transits through the Strait of Hormuz resume consistently within two weeks and anchoring levels return to normal congestion ranges, the disruption remains a cost shock rather than a supply shock. Under that condition, Brent trades at a higher structural floor due to insurance and freight repricing, but physical availability remains intact. LNG flows stabilise once cargo scheduling normalises. The system absorbs the event without lasting export impairment. If transit instability persists beyond three to four weeks, the tightening mechanism shifts from risk premium to delayed liftings and shipping scarcity. Cargo nominations begin to slip. Charter rates rise. War risk coverage contracts are available and priced. Under this duration threshold, Brent above USD 100 per barrel reflects constrained export flow rather than speculative positioning. LNG spot prices tighten in parallel as Qatari shipments face scheduling uncertainty. Import-dependent economies such as India and Japan face immediate cost transmission into current accounts and power generation pricing. European storage drawdowns accelerate if replacement cargo competition intensifies.

A different phase begins if strikes repeatedly target stabilisation plants, separation facilities, and export terminals. Abqaiq, Ras Tanura, and associated processing nodes represent throughput bottlenecks rather than distributed wellhead capacity. Repeated impact against these nodes would impair export capability even if upstream production remains intact. If 10 to 15 million barrels per day of effective Gulf export capacity is removed for several months, price formation reflects restoration timelines rather than transit risk. Under that condition, Brent above USD 150 per barrel is consistent with the supply removal scale. Repair cycles would extend if impacts recur during restoration attempts.

A separate escalation pathway arises if elevated oil prices persist into the US political cycle. Sustained Brent above USD 100 per barrel increases the probability of crude and LNG export restrictions under existing legal authorities. The US produced approximately 13.6 million barrels per day of crude oil and 110 billion cubic feet per day of natural gas in 2025. Export controls would tighten Atlantic Basin balances. Europe sourced approximately 57 percent of LNG imports from the US in 2025, while Russian flows remain structurally reduced. Concurrent Gulf impairment and US export restrictions would materially compress European supply channels and be transmitted into electricity pricing within weeks. Market pricing currently reflects transit disruption risk. It does not fully reflect sustained processing impairment or export policy intervention. The trajectory will be determined by measurable developments: persistent anchoring levels, strike density against processing assets, producer export guidance revisions, and shifts in US domestic energy policy signalling.