As preferential trade agreements expand and origin rules become more granular, accurate origin calculations are essential for determining whether manufactured goods qualify for tariff benefits and regulatory relief.

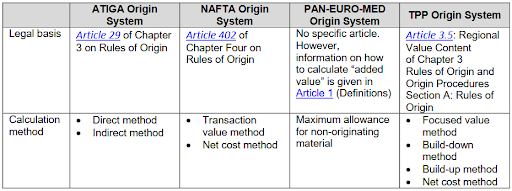

Rules of origin vary across free trade agreement and include product specific rules, mainly listed by HS chapter/heading/subheading (or also via ‘35% Appraised Value’ method like in US-Morocco or US-Jordan FTA’s). Usually the FTA contains the ‘Rules of Origin’ Annex/chapter, such as ‘List of Working or Processing Required to be Carried out on Non-originating Materials in order that/for the Product Manufactured can/to Obtain Originating Status’ (Annex II in most UK or EU FTA’s, or Annex 3 ‘Product-Specific Rules of Origin’ for the TCA), and similar.

For example, the ATIGA origin system (under the ASEAN Trade in Goods Agreement) has two calculation methods: direct and indirect (both have specific calculation formulas), whereas the NAFTA FTA (please note: USMCA substituted NAFTA FTA) calculation methods available are transaction value or net cost methods.

The more FTAs a country has, the more difficult it can be to navigate, but some jurisdictions offer simplifications. For example, the US Customs and Border Protection released the ‘CBP FTA comparison chart’ to help traders find reference documents of where to find rules of origin. However, whether the authorities provide navigation tools or other simplifications, it is crucial that the trader refers to the specific rules of origin and calculation method under the specific FTA.

Depending on the complexity of the manufactured product and the number of its sub-components, preferential origin calculations can be very challenging. To prepare for origin calculations, the quantities and costs of all inputs used in the finished product must first be identified. This includes raw materials or sub-components and other purchased parts. Additionally, overhead costs such as labour, engineering, product design, royalties, as well as the HS codes and origin status (preferential or non-preferential) of each item, needs be determined. This information is essential to ensure the origin calculations are accurate and compliant.

Once the trader has all the information and chooses a free trade agreement to take advantage of, the product-specific rule of origin (legal basis) and method need to be determined next.

Case study: Automotive supplier

A British automotive supplier produces car seats and needs to calculate the origin of its manufactured goods for a customer in the Czech Republic. Aware that an FTA exists between the UK and the EU (the TCA), the supplier refers to the HS heading 9401 to review the specific rule of origin for the product. The supplier finds that heading 9401 falls under product-specific rules of origin and needs to be calculated in line with the specific rules for each FTA.

Traders conducting origin calculations for product’s eligibility need to familiarise themselves with concepts such as Regional Value Content (RVC), Value Added Rule (percentage rule), or MaxNOM percentage (EXW), and tariff shifts. Additionally, calculation methods vary from one FTA to another so it is important to understand the correct method to use for a given circumstance.

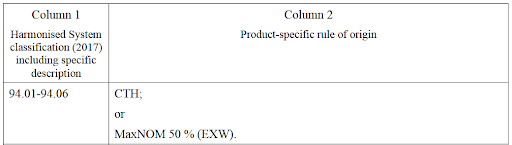

The table below, sourced from the WTO Study (2017), illustrates how calculation methods vary for a specific FTA.

Column 1: ‘94.01–94.06’, and notes that Column 2 sets out the following rule: ‘CTH; or MaxNOM 50% (EXW).’ (Source, page 1081)

What this means is that, for the product to obtain originating (preferential) status, it must either meet the tariff shift requirement (change in tariff heading), meaning all components incorporated into the product must fall under a different HS heading than 9401, or the product must contain at least 50% originating content based on the EXW value.

This originating content can be made up of UK origin components, or both UK and EU origin components if cumulation rules are applied. If the latter is used, the supplier must inform the customer that cumulation was used with the EU.

Best practice is for the manufacturer to have a bill of materials (BOM) available for each manufactured product with all material quantities and costs, which is especially crucial for more complex goods. The table below shows what the BOM for preferential origin calculation could look like.

| Bill of Material for car seat sub-assembly XYZ, company ABC Seats Ltd | HS: 9401 | ||||||||

| Material | Part number | Supplier | HTS Code | Material costs | Quantity used | Country of origin | Preferential status | Total material costs (EUR) | |

| H Screw | S-1000 | XA | 7318156290 | 0.15 | 25 | China | N | 3.75 € | |

| Springs | S-2300 | XB | 7320909090 | 1.20 | 33 | GB | Y | 39.60 € | |

| Lock Washers | W-4700 | XC | 7318210098 | 0.50 | 5 | GB | Y | 2.50 € | |

| Motor | M-4444 | XD | 8501109190 | 6.30 | 2 | GB | Y | 12.60 € | |

| Seal A | S-A-320 | XF | 4016930090 | 2.20 | 10 | GB | Y | 22.00 € | |

| Seal B | S-B-320 | XF | 4016930090 | 2.50 | 5 | Italy | Y | 12.50 € | |

| Material costs | 92.95 € | ||||||||

| Labour costs | 15.20 € | ||||||||

| Other overhead costs | 2.50 € | ||||||||

| EXW price | 110.65 € | ||||||||

| Total GB content | 94.40 € / 85.31 % | ||||||||

| Total non-GB content | 15.95 € / 14.69 % | ||||||||

| Rule CTH | Tariff shift – met | ||||||||

| Rule MaxNom 50% (EXW) | Met (85.31%) | ||||||||

Automation and supplier declarations

Businesses may also choose to automate the process by investing in an origin management program, either as a stand-alone customs software solution or integrated within the company’s ERP system(WCJ).

Several such programs exist, such as Thomson Reuters’ Onesource Free Trade Agreement Management, PwC’s Customs origin calculation tool, AEB’s Origin and Preference, and MIC Cust’s Origin Calculation Free Trade Agreement Management.

Cost assessment, including expert knowledge, software and administration costs, would need to be made and compared to the software costs to determine whether the business would benefit from automation. When set up correctly, origin management automation can save time, reduce costs, strengthen supplier relationships, and enhance trade compliance across the supply chain.

One of the most common automation mechanisms is the use of supplier declarations, such as long-term supplier declarations in the EU, which are especially useful where suppliers sell a wide range of products on a recurring basis. These declarations provide critical origin data used to build BOMs within origin management systems.

In contrast, such declarations are not typically used in the United States, Asia Pacific, or Latin America. Instead, depending on the FTA, suppliers may issue certificates of origin, such as USMCA certificates, to support preferential claims. Automation is still possible through BOM-driven origin calculation engines embedded in customs software.

Depending on software capability, required inputs usually include material and component costs, origin, source, preferential status, HTS classification, cumulation information, and production or overhead costs.

It should be noted that different regions apply different valuation bases. For example, the free on board method is commonly used in the United States and Asia Pacific, while the ex works method is used in the European Union, and the net cost method applies under USMCA.

Once the BOM is calculated, the software interprets the relevant rules of origin and provides a determination as to whether the product qualifies for preferential treatment. Some systems further automate supplier data ingestion using machine learning or optical character recognition technologies.

While origin automation is common among medium to large manufacturers, traders should assess whether software investment is appropriate based on supply chain complexity, data availability, and operational scale.

For deeper guidance on origin calculations, preferential trade compliance, and practical application across free trade agreements, explore the full Exporters Guide here