Infrastructure corridors reshaping trade routes

Emerging markets have seen a resurgence in investor interest after a period of relative underperformance. Factors such as a weakening US dollar, strong commodity prices, and changes in US tariff policies have contributed to increased local-currency trade and capital inflows, particularly in Africa and Asia, says Pangea-Risk’s Insight 2026.

Despite this, outcomes remain uneven, with opportunities mainly in politically stable countries that have strategic importance and solid market structures.

These gains come from policy reforms, improved governance, and targeted investments that strengthened economic resilience. In contrast, those with political instability or weak governance face capital outflows and limited investment.

Infrastructure corridors reshaping trade routes

Large-scale infrastructure projects are transforming trade routes, industrial capacity, and regional integration in Africa, Asia, the Middle East, and Latin America.

These initiatives would lower logistics expenses, enhance export capability, and draw in private investment to foster sustainable economic development.

The Capricorn Bioceanic Corridor, which is a 2,300-kilometre road, would connect Brazil, Paraguay, Argentina, and Chile. It will cut freight costs by up to 40% and save about 15 days in shipping time. This corridor will create new export routes for agricultural, mining, and manufactured goods, boosting trade in the region.

Similarly, the Lobito Corridor, a rail-based multimodal network connects Angola’s Lobito port with mining regions in the Democratic Republic of Congo and Zambia. This project aims to offer more options for exporting minerals and to make the supply chain stronger.

In West Africa, the Abidjan–Lagos Corridor Highway, valued at $15.6 billion, connects five West African countries to alleviate congestion and strengthen regional value chains.

In North Africa, Morocco’s $1 billion Nador West Med deep-water port and industrial platform is slated to commence operations in the second half of 2026. The project will have an initial capacity of about 1.8 million TEU per year. It will improve Morocco’s role as a logistics and energy hub in the Mediterranean, connecting Europe, North Africa, and West Africa. Additionally, it is expected to create up to 100,000 jobs.

Senegal’s Port of Ndayane, a deep-water logistics hub designed to handle up to 1.5 million TEU annually, is projected to contribute up to 3% to the country’s GDP by 2035. This port will enhance Senegal’s role as a maritime gateway for West Africa.

Adding to these projects, the Grand Faw Port Corridor in Iraq integrates port, rail, and highway infrastructure linking southern Iraq to Turkey. This will be part of a $17 billion project that is set to start partial operations in 2026. This development aims to make Iraq an important transit hub between the Gulf and Europe.

On a similar line, the Gulf Cooperation Council (GCC) is advancing its Unified Rail Network, a long-term cross-border railway programme connecting all six Gulf states. Construction will start in 2026 on the rail link between Saudi Arabia and Kuwait, and work is ongoing on the Hafeet Rail, which will connect the UAE and Oman. The planned investment of over $250 billion would cut down transportation costs and boost trade in the region.

The success of these projects will require effective governance, regional cooperation, and sustained investment.

Capital flows are likely to be selective

In 2026, investment flows into emerging markets are expected to be selective.

Investors are likely to focus on countries that have robust policies, stable currencies, and goals that align with their interests.

Debt fund inflows are projected between $40 billion and $50 billion across Sub-Saharan Africa, the Middle East and North Africa, and Asia-Pacific, supplemented by significant equity and infrastructure investments.

Sovereign issuers in emerging markets are cautiously returning to international debt markets, mainly through refinancing and liability management. Commodity-linked countries such as Angola, Nigeria, and South Africa have led this trend, reflecting improved fiscal management and favourable commodity prices.

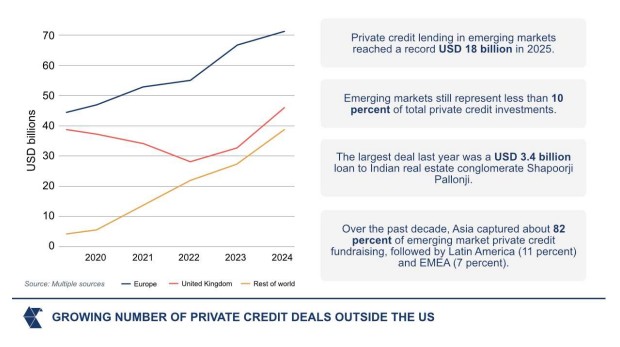

Private credit is expanding rapidly, with $18 billion invested in emerging markets in 2025 as a result of reduced lending by banks. This provided the opportunity for alternative financiers.

Development finance institutions are shifting focus from traditional aid to strategic sector financing, emphasising supply chain resilience, national security, climate change mitigation, and energy transition. Also, outcome-linked debt instruments, including debt-for-nature and debt-for-food security swaps, are gaining prominence as mechanisms to increase fiscal space while addressing social and environmental challenges.

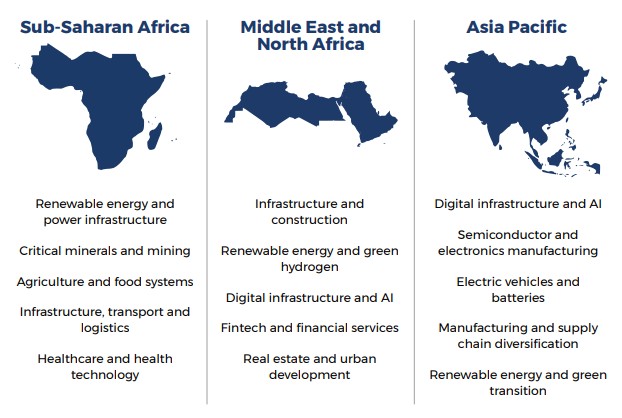

Sectoral investment priorities

Renewable energy and power infrastructure investments are accelerating, driven by the global energy transition and the need for grid modernisation and storage solutions. Critical minerals and mining remain strategic sectors due to their importance in technology and clean energy supply chains.

Agriculture and food systems continue to attract investment aimed at improving food security and sustainability amid global supply disruptions. Digital infrastructure and technologies supporting artificial intelligence are expanding rapidly, enabling economic modernisation.

Additionally, manufacturing and supply chain diversification are reshaping production hubs, especially in Asia and Africa, as companies seek to reduce dependency on single-source suppliers. Healthcare infrastructure and technology investments are increasing in response to rising demand for medical services and pandemic preparedness.

Geopolitical and risk factors remain

Insight 2026 emphasizes that emerging markets offer major trade and investment opportunities, but success depends on understanding the varied political and economic conditions.

Growth momentum is expected to continue in 2026, but there are risks. Geopolitical tensions, political instability, and financing needs will impact capital flows and investment risks.

A sharper slowdown in advanced economies, especially due to new trade restrictions or tariff increases, could reduce export demand and fiscal revenues.

If the US raises interest rates to combat inflation, it may strengthen the dollar and tighten external financing conditions. Political unrest in 40 countries holding elections, along with policy reversals and reform delays, poses risks, especially for economies dependent on multilateral aid or portfolio inflows.

These factors indicate that the recovery in emerging markets is fragile and conditional, with capital flows expected to be selective and sensitive to both global and domestic risks through 2026.

Regions experiencing managed conflict de-escalation and peace agreements offer more stable environments, while unresolved conflicts and coercive actions pose ongoing risks.

Stakeholders equipped with detailed, localised intelligence and scenario-based risk assessments will be best positioned to capitalise on durable opportunities and mitigate risks in the fragmented global economy of 2026 and beyond.

Read the full report here.

Article Info

Related Articles

Digital Trade +2

Digital Trade +2Trade digitalisation accelerating: what’s next?

By: James Dorman The momentum behind the digitalisation of trade and trade finance is undeniable....

Risk Management +2

Risk Management +2We are in a new G2 world – here is a way forward for the rest of the world

TTP’s Global Advisory Panel member, Chris Southworth argues that the old economic order has quietly...

Correspondent Banking +4

Correspondent Banking +4The last correspondent: how de-risking left a sovereign nation distributing dollars by blockchain

De-risking has removed most correspondent banking relationships across the Pacific and parts of Eastern Europe,...

Cash Management +2

Cash Management +2No ownership, no profit: How Murabahah keeps trade finance honest

By: Iqbal Karmally In Islamic trade finance, the bank does not lend — it buys...

Stay Ahead of the Curve

Get exclusive insights, expert analysis, and breaking news on liquidity and risk management, delivered to your inbox

Article Info

Stay Updated

Get the latest insights on trade finance, treasury management, and global payments delivered to your inbox.

Join 25,000+ professionals. Unsubscribe anytime.