The legal foundations of today’s tariff landscape

For most of the modern era, tariffs have been a background factor for many in global trade. Over the course of 2025, however, they have become the top issue for nearly every operator in the space.

That is why Aon Credit Solutions, the American Metal Supply Chain Institute (AMCI) and Trade Treasury Payments (TTP) hosted the “Navigating Tariffs, Trade and Risk” webinar.

During the session, moderator Kim Cordero, Deputy US Practice Leader at Aon, spoke with Lawrence Hanson, of counsel at Sandler, Travis & Rosenberg; José Gasca, co-founder of ME Trading and chair of AMCI; Ricardo Berisso, senior steel merchant at Cargill; and David Culotta, senior risk executive and chief underwriting officer at Coface North America

The legal foundations of today’s tariff landscape

The first step in navigating tariffs is understanding where they come from. As Larry Hanson reminded the audience, nothing about the core legal tools is new. What has changed is the way they are being deployed.

Section 301 tariffs began as a response to intellectual property violations in China, but “that has now expanded to, frankly, all things China,” Hanson explained. Section 201 of the Trade Act targets very specific product groups, such as solar panels and washing machines, while Section 232 has become the “most popular tool” in recent years because it allows the president to impose tariffs on national security grounds with broad discretion.

The most contentious development, however, has been the use of the International Emergency Economic Powers Act (IEEPA). This statute dates back to 1977, with roots in the earlier Trading with the Enemy Act of 1917. It was not drafted with tariff policy in mind. Yet, as Hanson explained, “in the last year… he’d been using the International Economic Emergency Powers Act, or IEEPA, as a basis for additional tariffs, as a weapon, if you will”.

The Supreme Court is now considering whether the president has gone too far. The case turns on two questions. First, can a loosely defined “emergency” trigger such sweeping powers for tariffs under IEEPA? Second, does that interpretation erode the constitutional role of Congress in controlling the power of the purse?

Hanson noted that earlier in the process, he “would have bet a year ago that this is an absolute done deal” against the tariffs, because IEEPA “has never been used before like this ever”, and the constitutional questions are so fundamental. Today, given the current composition of the court and a historical precedent from the Nixon era, he is less certain. That earlier case involved a temporary 10% tariff used to stabilise the currency under the old Trading with the Enemy Act. It could offer cover for upholding presidential authority, even though, as he pointed out, IEEPA “was designed to limit the power of the president rather than expand the power of the president”.

For trade finance and credit professionals, the outcome matters in very practical ways. If the tariffs are struck down, the question becomes how any refunds would be handled, over what period and subject to what conditions. Hanson outlined three possible paths: a traditional administrative protest process at customs, automatic refunds once illegality is confirmed, or a specific appropriation by Congress. None is straightforward at the scale involved.

There is also no guarantee that a legal defeat on IEEPA would end tariff pressure. The president “has other weapons in his arsenal”, including Sections 301, 201 and 232, as well as “even more obscure” statutes, Hanson added.

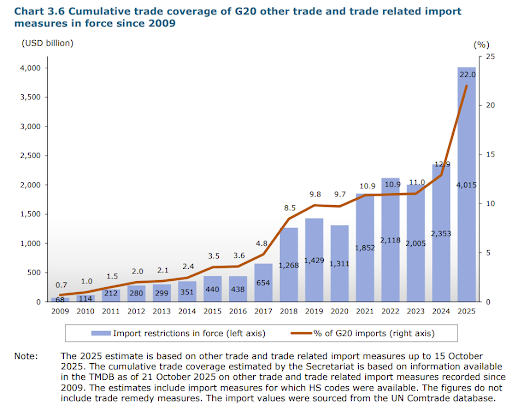

Beyond the courtroom, Hanson painted a wider picture of a strained global trading system. The post-war attempt to manage trade tensions through common rules has weakened. He noted that the World Trade Organization’s appellate body “essentially does not exist” because there are not enough judges. If a party appeals, “there’s no appeal, because they don’t have the mechanics”. At the same time, unilateral tariffs are increasingly used as leverage, with the president ultimately saying: “We’re going to have these tariffs, unless you negotiate with me”.

Source: World Trade Organization

Protectionism in practice and the changing role of traders

With Hanson providing a legal overview, we turn to José Gasca and Ricardo Berisso, who give a perspective from the trading floor, as both operate in the steel sector, which has been a focal point for protectionist measures since 2018.

Gasca, who has been trading for around 30 years, noted that traders are used to adapting to changing conditions, but the past few years have felt different. Since Section 232 tariffs were implemented, he said, “we have been seeing more and more a protectionist environment, not only in the United States, but also in Europe, of course, Latin America, and some parts of Asia”.

That shift has forced a fundamental change in business models. In his words, the “traditional trader that would buy material and sell materials without any added value” is being replaced by a trader who can “add value by processing steel, by offering consignment agreements to customers, extra terms, special delivery requirements”. He argued that this kind of regional, service-centre role is “the only way that a trader can justify its role and can be part of a modern way of doing business in the steel industry”.

Berisso echoed the sense of a system under pressure. From his vantage point at Cargill, he sees a range of measures reshaping flows into and within Europe. One example is the EU’s Carbon Border Adjustment Mechanism (CBAM), which he described as “a CO2 carbon tax”. In other regions, he pointed to anti-dumping measures in Korea against Chinese steel and in India against Vietnamese steel. “It looks like the world is closing the doors to trade,” he said, adding that “globalisation is having a bit of a hit at the moment”.

China sits at the centre of this dynamic. Berisso spoke of the “involution theory” in China, where “it refers to a cycle of excessive self-defeating competition… what we call a race to the bottom”. He noted that this pattern has been visible in the steel business and is now spilling over into automotive, particularly on the electric side. For developed industrial bases, this creates hard choices. “We might see… the United States today paying double the price on steel than what China and other countries are importing for,” he said. Similar pressures can also be seen in Europe, with question marks over how this affects demand.

In that environment, trading has become more complex and more data-driven. “Life as a trader has become way more difficult than it was before,” Berisso said. “In some cases, we’re flying blind when we do some trades.” That uncertainty is pushing counterparties towards firms that can help them see and manage risk (as opposed to those that only help them execute transactions).

Cargill uses analytics “on a daily basis to try to understand our potential risk” and is increasingly asked by customers “how can Cargill… help me mitigate my risk,” Berisso said. That may involve taking input risk or price risk out of customers’ hands. At the same time, the firm is selective about the trades and counterparties it engages with.

Gasca’s experience in North America, on the other hand, provides an example of how fast the landscape can change. Many companies invested in plants on the Mexican side of the border in recent years, expecting nearshoring and reshoring to create a “bright future”. The implementation of US tariffs on Mexican goods has complicated those plans. Still, he sees enduring fundamentals in North American trade, rooted in complementary supply and demand. Mexico has products that the US cannot produce in sufficient quantity, while Mexican industry depends heavily on US goods.

He pointed to the growing interest in organisations like AMCI as companies seek information and networks to adapt to these shifts. “There is a lack of information, there is a lack of networking,” he said, arguing that “this is the right time to join organisations like ours” to understand where to operate and how.

For trade, treasury and payments practitioners, these experiences translate into concrete questions. Where will supply be reliable? How will price differentials evolve across regions? How exposed are borrowers and buyers to sudden regulatory changes? And to what extent can service-centre traders and regional platforms act as stabilisers in such a fragmented system?

Credit risk, counterparties, and the new information gap

Given all the changes, uncertainty, and questions abound, it is little wonder that the rise in protectionism is spilling over into the risk domain, something Coface’s David Culotta helped explain.

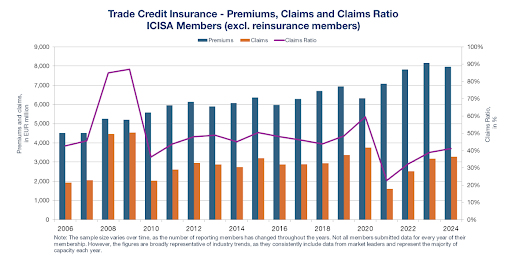

Trade credit insurance, he said, “is essentially offering insurance against payment default risk or bankruptcy risk”. Beyond the payout, however, the product offers advice and ongoing analysis. Analysts “diving into the… risk associated with not only one counterparty, but your entire portfolio” can help clients understand where they are most exposed.

Source: International Credit Insurance and Surety Association (ICISA)

The array of tariffs and protectionist measures entering the policy arena is certainly changing that risk map. At Coface, teams are “taking a particularly strong look and closely monitoring very specific sectors and the overall impact… of the tariffs”. In steel, for example, oversupply from China is now spilling into Europe because the US is importing less of the metal, which leaves Europe absorbing more low-priced Chinese material. Culotta said this dynamic has created “a bit of a discrepancy between pricing on European hot rolled coil versus the US product” because European markets are grappling with cheaper inflows while US prices remain higher behind tariff walls.

This uneven picture creates both winners and losers. Culotta pointed to end markets related to construction and automotive as sectors “under pressure”, while “anything related to data centre rollout and infrastructure related to data centres” is seeing stronger demand. From an insurer’s perspective, the priority is to understand “at the buyer level… what that end market looks like, who they’re selling to, and what the overall impact is”.

In practice, that means daily dialogue with clients, careful limit setting, and a degree of caution in an uncertain environment. “Because of the amount of uncertainty, there’s a certain reluctance to release that capacity,” Culotta said. Discussions focus on “right-sizing and putting in place appropriate buffers”, while staying ready to support clients who want to seize spot opportunities or capacity gaps, such as when domestic production cannot meet demand.

Kim Cordero added that many companies are looking beyond straightforward buyer insolvency cover, with some seeking protection “on a pre-delivery loss basis via insolvency”, and in some cases, “movement in that price can be incorporated”. Clearly, price risk and supply competition now sit high on the risk agenda.

For Gasca, credit insurance has become as important as a banking relationship. In Europe, he noted, “credit insurance is a tool to get credit. The banks take the credit insurance as collateral”. His firm is proud never to have had to use its policy, but values it as a conservative risk tool. At the same time, he stressed that the goal should be to avoid claims, not to rely on the policy. That requires knowing customers well: “You need to know their capabilities, their financial situation, their market situation”, he said.

Compliance as strategy and the line between evasion and planning

Given the onslaught of tariffs, it is tempting for many traders to try and find ways to minimise the amounts that they will need to pay. This is where the distinction between tariff evasion and tariff avoidance becomes important to understand. From a legal standpoint, Hanson explains, tariff avoidance is the perfectly legal act of structuring affairs to reduce taxes or duties, while tariff evasion is the illegal act of lying or concealing information.

In the trade context, he said, “the core of all evasion… basically begins with just lying”. That might involve misdeclaring origin, for example, by moving Chinese-origin goods through another country, exporting them from there and “calling it Vietnamese”. It can also involve misclassification, where the product is declared under a tariff line with lower duties, or under-valuation, where post-shipment adjustments reduce the declared value on which duty is assessed.

These methods are not new, but the stakes are higher because duty levels are so significant. Customs authorities are alert to them, and “increasingly there’s been threats of jail time for this type of thing, not just an additional bill for the duty”. Hanson described cases where companies built plants to shift production, spending “tens or hundreds of millions of dollars”, only to discover that the transformation carried out was not enough to change origin. They ended up owing both Chinese and, in some cases, additional duties, with the result that he advised one client to “be talking to a bankruptcy attorney pretty quick”.

By contrast, avoidance involves “good planning… to limit your duty and to reduce your risk”, without deception. He cited examples such as the first-sale rule, where duties are based on the value of an input at an earlier transaction stage, or careful structuring of supply chains so that substantial transformation really does take place in a different country. The key test is transparency. “The key thing about avoidance is you never have to lie about it,” he said. Companies can go to customs and say “flat out, here’s what we’re going to do”, secure their agreement, and proceed legally.

But what happens when companies come forward having already made mistakes? Hanson says that early, accurate advice is essential because once goods are imported under a false premise, the available options have already narrowed. In some cases, there is room to correct course before an investigation starts, but in others, especially where structural missteps have already been baked into capital investment, the scope for remedy is limited.

Gasca connected this back to commercial behaviour, especially with the large amounts of uncertainty, arguing that “this is the time to know your customer well”. That applies equally to buyers, suppliers, and other intermediaries that might be involved in the process. When new players appear promising attractive terms or quick fixes, the risk of non-compliance rises. His firm has “preferred to say no to a customer than really entering into a risk that is unknown for us and that we’re going to disappoint someone”.

He also pointed to a recent example in Mexico, where the government decided “not to let any import from Malaysia, Indonesia, and Vietnam”. The decision was “announced, from one day to the other”, leaving many companies with unexpected supply problems or cargo they could not clear. Gasca’s team had heard rumours beforehand and chose not to engage in those flows. “We decided not to engage and not to offer because we knew that there was a rumour that this could happen,” he said. For him, that is also a question of principles, advising customers not to do certain business, even at the cost of immediate revenue.

A tariff-evading structure can turn a previously sound counterparty into a distressed one overnight. Conversely, companies that invest in good planning and transparent engagement with authorities can offer a more stable base for trade and working capital finance.

Preparing for the next phase of global trade tensions

The webinar closed with a look at the geopolitical picture and what may come next. Cordero asked Culotta about the recent in-person meetings between US President Donald Trump and Chinese President Xi Jinping and their implications.

Culotta relayed an analogy he had heard, comparing the meeting to “a boxing match that went on multiple rounds without an actual knockout”. The immediate outcome was an avoidance of the most extreme scenarios, including “the threat of 100% tariffs against China for at least the immediate term”. He described the current situation as “a fragile trade truce… that provides a resolution to the most immediate issues”.

From the US side, priorities included stemming flows of fentanyl precursors, addressing export controls on rare earths and retaliation affecting the semiconductor industry, and reopening markets for heavily taxed agricultural exports such as soybeans. The meeting reduced some immediate fears, but it’s a long road ahead.

Hanson, looking at longer history, warned that the system is “very volatile” both on day-to-day trade flows and on the legal framework. The original post-war attempt to manage trade relations through the General Agreement on Tariffs and Trade in 1948 was rooted in the recognition that trade conflicts had contributed to earlier wars. Today, his concern is that “we have not learned our history” and are drifting back towards more fragmented and conflictual trade.

He noted that other countries are beginning to question whether the US should sit at the centre of global trade and finance to the same degree, including in areas such as currency and payment systems. At the same time, firms need to be willing to step back from transactions where risk cannot be measured or controlled. In Gasca’s words, “these are the times to have these things in mind all the time”.

Trade has adapted to major shifts before. New rules, new technologies and new patterns of global demand have repeatedly forced companies and financiers to rethink how they operate. The current wave of tariffs and protectionism is another such moment.

The insights from this AMCI–Aon–TTP discussion suggest that those who invest in legal clarity, robust compliance and information-rich credit-risk management will be best placed to contend with whatever comes next.

Article Info

Related Articles

Digital Trade +2

Digital Trade +2Trade digitalisation accelerating: what’s next?

By: James Dorman The momentum behind the digitalisation of trade and trade finance is undeniable....

Risk Management +2

Risk Management +2We are in a new G2 world – here is a way forward for the rest of the world

TTP’s Global Advisory Panel member, Chris Southworth argues that the old economic order has quietly...

Correspondent Banking +4

Correspondent Banking +4The last correspondent: how de-risking left a sovereign nation distributing dollars by blockchain

De-risking has removed most correspondent banking relationships across the Pacific and parts of Eastern Europe,...

Cash Management +2

Cash Management +2No ownership, no profit: How Murabahah keeps trade finance honest

By: Iqbal Karmally In Islamic trade finance, the bank does not lend — it buys...

Stay Ahead of the Curve

Get exclusive insights, expert analysis, and breaking news on liquidity and risk management, delivered to your inbox

Article Info

Featuring

Stay Updated

Get the latest insights on trade finance, treasury management, and global payments delivered to your inbox.

Join 25,000+ professionals. Unsubscribe anytime.