Global supply chains continue to operate under intense strain, with the latest Chartered Institute of Procurement & Supply (CIPS) Pulse Survey for Q2 2026 revealing that a slight easing in short-term anxiety does not signal a return to stability but rather a new normal of elevated risk.

Procurement and supply chain professionals remain deeply concerned about geopolitical conflicts, cyber threats, and tariff uncertainties shaping the risk landscape.

Ben Farrell MBE, Global CEO of CIPS, said: “The tectonic plates of global trade are shifting. The world we knew has gone. Regionalisation is rising, globalisation is being reshaped, and those organisations that build resilient regional partnerships will be best placed to thrive.”

“Procurement and supply professionals are turning geopolitical exposure into practical options. They are moving beyond traditional just-in-time models towards more resilient supply webs that can maintain continuity when routes are blocked, inputs are restricted or sudden shocks occur. With conflict in the Middle East, continued instability linked to Iran and the ongoing war in Ukraine, the NATO Summit in Ankara is putting security of supply firmly in the spotlight. Procurement is a strategic function at the heart of national and organisational resilience.”

Elevated risk environment amid geopolitical turmoil

The survey highlights that procurement and supply chain leaders are navigating an unusually high-risk environment dominated by ongoing conflicts in the Middle East and Ukraine, alongside broader geopolitical tensions.

These concerns come as global attention focuses on the NATO Summit in Ankara, Türkiye, scheduled for 7-8 July 2026, where defence, industrial resilience, and supply security are expected to be key topics.

While short-term concern about supply chain shortages and disruptions decreased to 4.95 on a 1–7 scale, down from a Q1 2026 peak of 5.69, it remains higher than any reading in the previous two and a half years.

Similarly, longer-term anxiety over the next 12 months eased to 5.0 from 5.64 but still ranks as the third-highest long-term concern recorded by the survey.

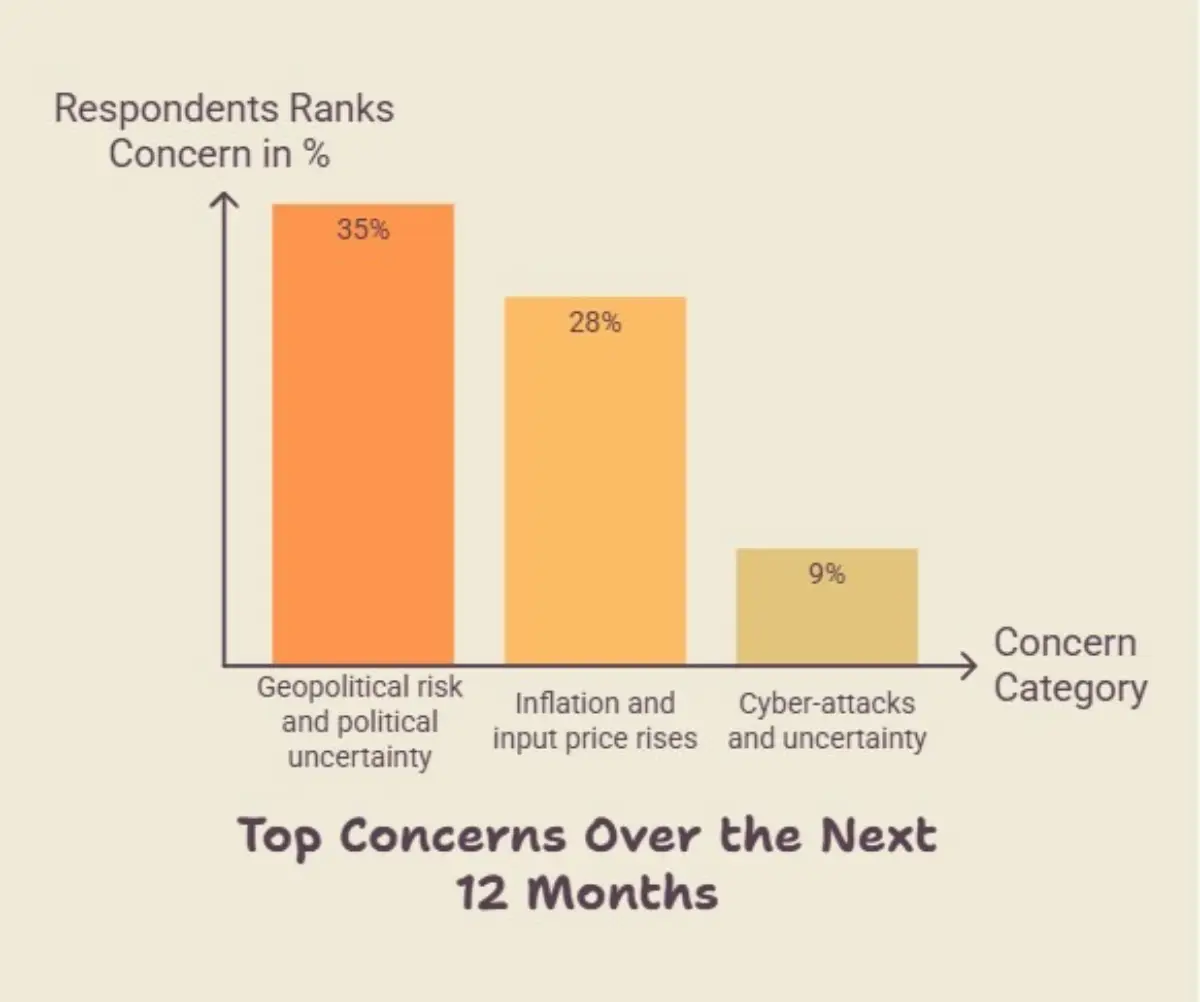

Middle East conflict dominates supply chain anxiety

Geopolitical disruption remains the primary driver of supply chain concern, with 75% of respondents citing conflict in the Middle East, 67% highlighting the general geopolitical environment, and 33% pointing to the war in Ukraine.

Although the proportion citing Middle East conflict has declined from 89% in Q1, it remains the leading source of anxiety. Concern over the war in Ukraine has increased from 28% to 33%, reflecting ongoing challenges across critical sectors including energy, logistics, food, manufacturing, and defence.

This shift confirms a trend identified in Q1, where immediate geopolitical threats surpassed US protectionism and US-China trade tensions as the top disruption causes. Despite some moderation in headline anxiety, the underlying risk remains severe.

Cyber-attacks rise as a critical supply chain threat

Cyber risk has surged in prominence among supply chain leaders.

This marks a shift from Q1, where logistics disruption ranked third. The change signals growing recognition of cyber-attacks as a direct threat to supply chain continuity beyond traditional IT risks.

A new survey question on cyber exposure revealed concern about cyber-attacks has risen to an average of 4.73 on a 1–7 scale, up from 4.32 in Q1. Nearly 79% of respondents rated their concern at 4 or above, with 17% expressing very great concern.

Proactive redesign of supply networks for resilience

Procurement teams are prioritising resilience strategies over narrow cost efficiency to ensure supply continuity in the face of disruption. The top strategies planned for the next three to six months are as below.

These figures indicate a strategic shift beyond reactive measures toward redesigning supply networks to reduce dependence on single suppliers, regions, or fragile transport corridors.

The profession is shifting from linear supply chains to complex supply webs that focus on visibility, flexibility, and resilience across various tiers.

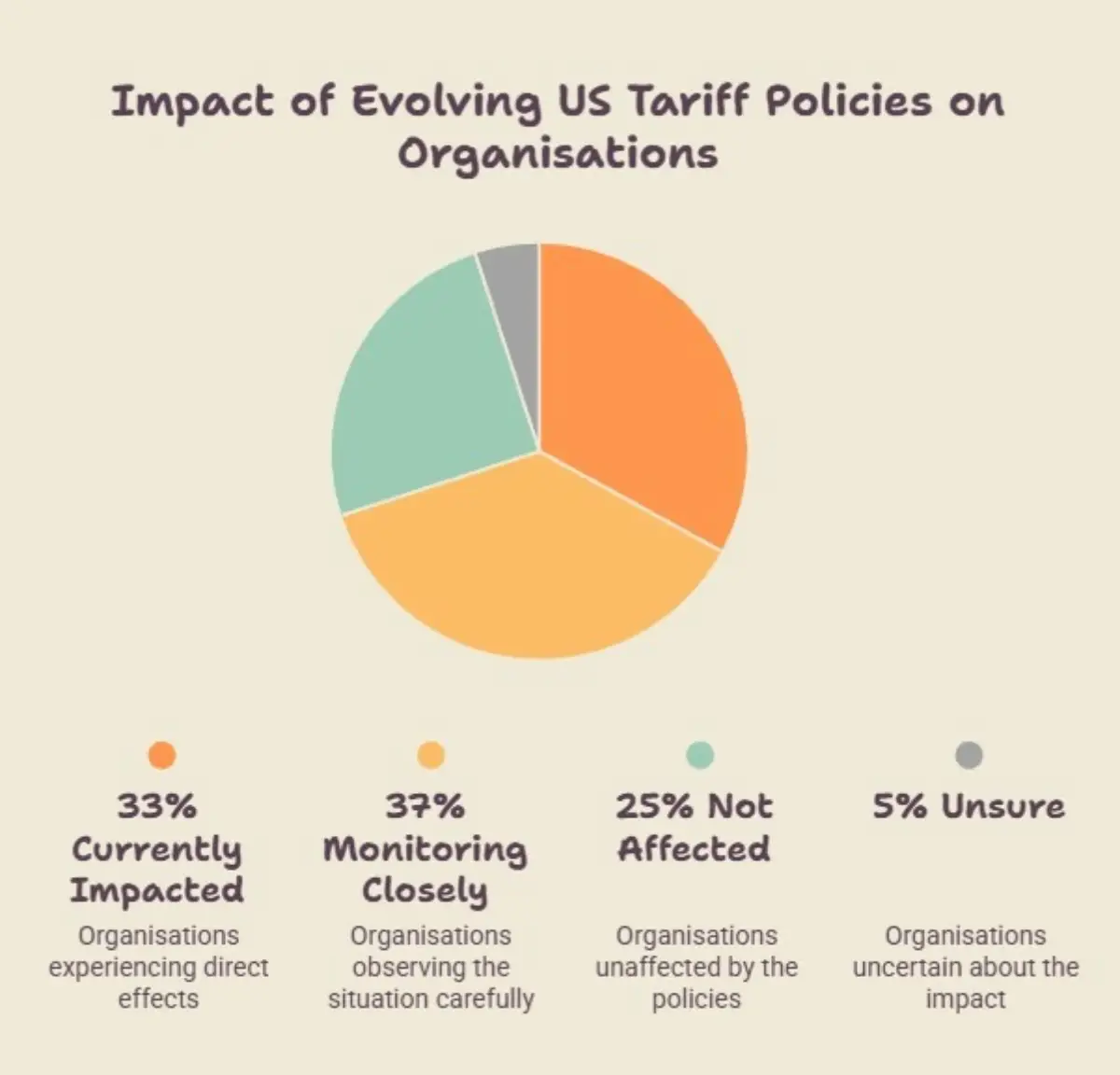

US tariff uncertainty persists as a background risk

Despite geopolitical conflicts dominating concerns, uncertainty around US tariff policy continues to affect procurement planning.

This shows tariff uncertainty as an ongoing risk factor amid more immediate operational challenges.

The economic impact

Dr John Glen, Chief Economist at CIPS, said: “The easing in short-term anxiety should not be misread as a return to normality. A short-term concern score of 4.95 is still higher than any Pulse reading before Q1 2026, and the 12-month outlook remains at one of the highest levels we have recorded. The direction of travel may have softened, but the level of concern remains elevated.”

“The increase in concern around cyber-attacks is another warning sign. Modern supply chains are digitally connected, so a cyber incident can rapidly become an operational, financial and reputational crisis.”

“Taken together, the data points to a global economy still vulnerable to stagflationary pressures: weak confidence, elevated costs and persistent geopolitical risk. The priority for businesses is to build resilience without locking in unnecessary cost. The priority for governments is to reduce uncertainty wherever possible and support the security of critical supply networks. Put bluntly the Global Economy is in danger of suffering from what the Cambridge Economist John Maynard Keynes labelled the ‘paradox of thrift. Faced with heightened levels of uncertainty and fear, consumers and businesses go to cash, save money and economic activity as a result contracts.”

The Q2 2026 CIPS survey shows how procurement professionals’ views on short-term and long-term (12-month+) supply chain risks, and their impact on input price increases, and organisation strategies to protect the supply chain.