Trade credit insurance (also named del credere insurance, credit insurance, business credit insurance, or export credit insurance) is the insurance product that businesses purchase to protect themselves against the risk that a buyer defaults on a payment obligation based on the delivery of goods and/or services. Trade credit insurance, as discussed in this context, is a business-to-business product only. As with many risk-transfer tools used in cross-border and domestic trade, its purpose is to strengthen commercial certainty in transactions where goods or services are supplied on credit.

When businesses trade, they often do so on open credit terms rather than making an upfront cash payment. For the sellers in these transactions, this “account receivable” is considered to be unsecured invested capital due to the risk that the buyer will not make payment on time, or at all.

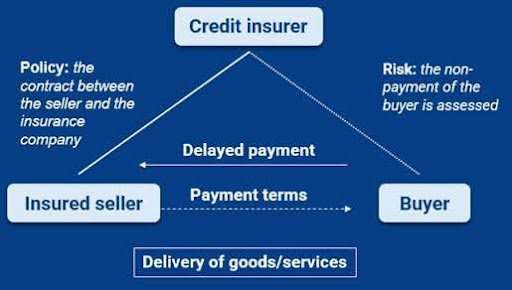

An interesting feature of trade credit insurance is that the policyholder does not represent the risk object like in property insurance. The risk object is a third party (the client of the policyholder).

Trade credit insurance is not used for all trade. In fact, current estimates put the penetration rate of trade credit insurance at around 15% of world trade volume. There are many instances where trade will not be insured, such as intragroup trade or trade where the seller has so much power over the buyer that credit insurance is not necessary.

Stakeholders

To understand trade credit insurance, it is important to first examine all of the possible stakeholders in an insurance transaction. Not all of these will be present in every transaction. Here is an overview of some of these participants:

Corporate clients/the policy holder: For the policy holder, TCI provides financial protection, often allowing them to access financing at a cheaper rate (or in some cases, at all). Corporates can also free up capital, protect cash flow (and therefore liquidity), and grow turnover by offering credit terms to customers and confidently selecting new customers.

Banks: Banks can also be users of credit insurance. Trade credit insurers will support financial institutions to mitigate the risks of unpaid invoices or delayed payments.

Factoring companies: Factoring companies may (and often do) protect the acquired receivables by means of trade credit insurance.

Reinsurers: provide risk capacity beyond what a trade credit insurance company can provide based on its own balance sheet. This allows primary insurers to reduce their exposure to large risks and to accept a larger volume of smaller risks than their balance sheet could carry without this support.

Brokers: Specialised credit insurance brokers are expert intermediaries between clients and insurance providers.

Regulators: The regulator’s role is to maintain financial stability and uphold standards in the insurance industry. Their rulings can affect the work of credit insurers; poor regulation can drive insurers out of a market or create a good environment for insurers to insure local companies.

Role of trade credit insurance in the economy

While it might not be as widely known as other industries, Trade credit insurance has a very important function in the economy. Some of its key aspects include:

Risk mitigation: This includes both protecting businesses against non-payment from their buyers and allowing businesses to better manage their credit risk by providing insights and assessments of customers’ financial health. It can also help stabilise financial systems by absorbing shocks from defaults, preventing cascading failures in interconnected businesses.

Trade facilitation: By transferring the risk of non-payment to the insurer, businesses are more willing to grant or extend credit terms to customers. Banks may also be more willing to offer financing or improve terms when credit risk is managed in this way. Trade credit insurance allows exporters to enter foreign markets with greater confidence by protecting against political and economic risks.

Stimulating economic growth: Companies with trade credit insurance often find it easier to secure financing from banks and financial institutions, as lenders view insured receivables as lower risk, thereby encouraging entrepreneurship and stimulating job creation.

Improving competition: Trade credit insurance can enable smaller businesses to compete more effectively with larger corporations by allowing them to offer competitive credit terms that would otherwise be too risky to be adequately financed.

Data and insights: Insurers often provide valuable information and analysis on market trends and customer risk (payment behaviour and payment capabilities), assisting businesses in making informed credit decisions.

To explore these concepts in greater depth, readers can continue into the full Trade Credit Insurance Guide, which offers a structured breakdown of policy types, underwriting processes, and practical applications across global trade.