Is it love? Is it fear? Or is it FOMO? I think it is – everything is fair in love and war when it comes to the United States’ stance on global geopolitics. Early this year, the US shocked the world with the strike on Venezuela! Then came the threat to acquire Greenland by any means possible. However, Greenland, being a Danish territory and therefore under NATO protection, is not a quick cease-and-desist. Did this fail to stir the still water of geopolitics? I don’t think so.

It’s this that on 14th February, US Secretary of State Marco Rubio sought to reassure Europe at the Munich Security Conference, declaring that Washington wants to “recharge” the transatlantic alliance so a powerful Europe can assist the US in a global mission of “renewal.”

This comes after months of friction fueled by President Donald Trump’s interest in annexing Greenland and his disparaging remarks toward allies and the threat of imposing high tariffs.

The Greenland question: Following a long American tradition

Trump’s fixation on acquiring Greenland, first revealed during his initial term, has transformed from a diplomatic curiosity into a cornerstone of his second-term foreign policy.

His interest in Greenland comes from multiple strategic calculations. First, the territory possesses vast mineral resources, including rare earth elements (REEs) crucial for advanced technologies and defence systems. China has heavy control over REEs (60% on production and 90% for processing). As China has imposed restrictions on REE exports, it directly impacts the US’s defence sector. The US’s advanced defence systems, such as Virginia- and Columbia-class submarines, drones, Joint Direct Attack Munition (JDAM) smart bombs, and F-35 fighter jets, require REEs.

This makes Greenland quite valuable for the US. Greenland also offers valuable deep-water ports and potential military installations in an increasingly contested Arctic region. It is a strategic foothold between North America and Europe that can significantly enhance American geopolitical positioning.

Amidst resistance from Denmark and support from the other EU countries, Trump imposed 10% tariffs on “any and all goods” from Denmark as well as the other 8 EU countries from 1 February, which could increase to 25% if no deal is struck by June.

America’s hook or crook pursuit of Greenland is not new.

Let’s rewind a bit. During the Cold War, the US repeatedly tried to buy Greenland from Denmark. Secretary of State James Byrnes made a direct offer in 1946, demanding full American sovereignty over the island. The Danes refused then as they refuse now.

Its historical irony cuts deep. When signing the 1916 treaty to acquire the Virgin Islands from Denmark for $25 million, Secretary of State Robert Lansing explicitly promised “that the Government of the United States of America will not object to the Danish Government extending their political and economic interests to the whole of Greenland.” This historical agreement now stands in stark contrast to current American ambitions.

The annexation of foreign territories has been a recurring theme in American history. The Louisiana Purchase of 1803 presented similar constitutional questions about the federal government’s power to acquire foreign territory. President Thomas Jefferson initially had concerns about whether the Constitution explicitly granted such authority, but ultimately proceeded with the treaty.

In 1823, Chief Justice John Marshall clarified in American Insurance Co. v. Canter that “The Constitution confers absolutely on the government of the Union, the powers of making war, and of making treaties; consequently, that government possesses the power of acquiring territory, either by conquest or by treaty.”

The acquisition of Texas and Hawaii had even more controversial precedents. After the Senate rejected a treaty of annexation for Texas in 1844, President John Tyler worked with President-elect James Knox Polk to have Texas admitted as a state using a joint resolution of Congress, which required only a simple majority vote. This move was criticised by some as exceeding congressional powers under the Constitution’s Necessary and Proper Clause.

Similarly, Hawaii’s annexation followed a complex and controversial path. American planter interests engineered a coup backed by a US warship to remove Queen Liliuokalani in 1893. After failed attempts to annex Hawaii through Senate treaty and joint resolution processes, the territory was finally annexed in 1898 amid the Spanish-American War through a joint resolution of Congress.

Europe’s anti-coercion instrument: A revenge or a tool?

The European Union now faces its most consequential decision on transatlantic relations in a generation. At the heart of this dilemma lies the anti-coercion instrument (ACI), a trade defence mechanism adopted in 2023 but never yet deployed.

Adopted after years of feeling economically vulnerable to foreign pressure, ACI gives the EU unprecedented powers to impose targeted sanctions, restrict market access, and even freeze financial assets when faced with economic blackmail. It allows the bloc to respond rapidly to coercion without getting bogged down in WTO disputes that can drag on for years. In essence, it’s Europe’s first serious attempt to weaponise its economic might in a world where trade has become another battlefield. Thus, it has been nicknamed the EU’s bazooka.

Dmitry Grozoubinski, Director at ExplainTrade, explains that “The EU’s ACI is perhaps best understood as a kind of European IEEPA, a legal and procedural framework to expedite the deployment of European tariff and trade measures in a crisis. When you hear calls for activating the ACI or deploying the ACI, what you’re really hearing is a call on the Commission to begin a process that will allow them to retaliate in the face of coercion, if diplomacy fails. The exact nature and scale of any such retaliation is up to the Commission and the member states to decide some way down the line.”

He further adds that, “The EU’s anti-coercion instrument has never been deployed, having only been created a few years ago. Its creation was spurred in part by the perception that the EU had no way to deploy its economic muscle in the face of coercion, with existing instruments being too slow, procedurally onerous, and prone to getting stuck in the EU decision-making apparatus to be effective weapons, bargaining chips or counter-attacks”

“In the past, when it wanted to retaliate, the EU generally had to awkwardly cobble together something using existing instruments, such as anti-dumping provisions, none of which provided optimal certainty, flexibility, or speed. The ACI provides a legal pathway and framework to retaliation, but Europe would still need to find the political will to use it, the economic strength to do so in a way that hurts, and the stomach to endure the pain it could entail.”

This conceptual divide explains why diplomatic reassurances, such as Rubio’s speech in Munich, fail to address the root causes of transatlantic friction. While the Secretary of State emphasised that “we want Europe to be strong,” Washington’s actions suggest strength is acceptable only within parameters defined by American interests.

Can ACI give the EU economic leverage?

The US-EU economic relationship, valued at approximately $1.68 trillion (as of 2024) in annual bilateral trade, is the world’s largest trading partnership, accounting for 30% of trade and 43% of the GDP.

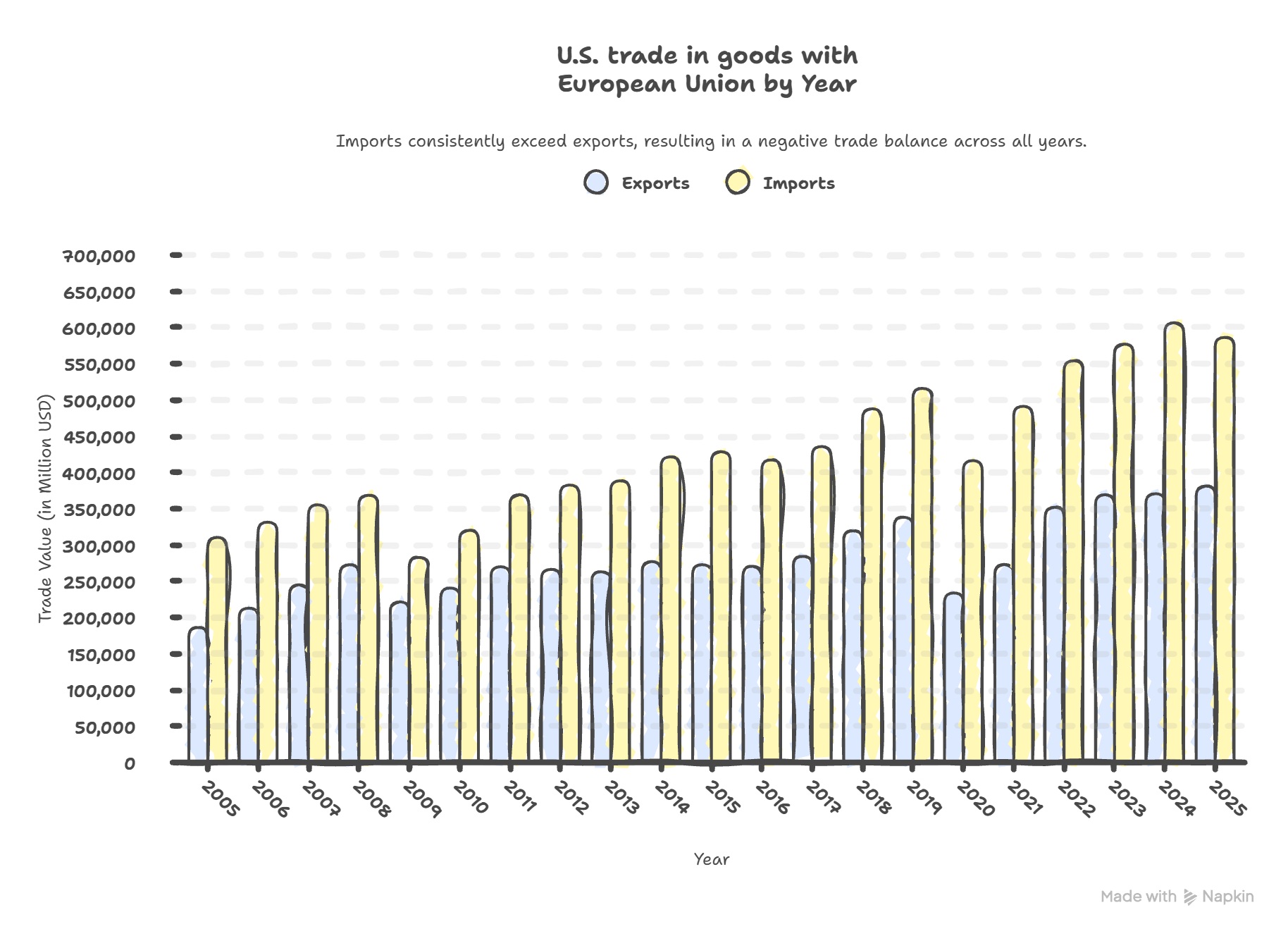

Over the years, the EU’s exports to the US have increased from $185 million to $380 million in 2005, while imports have increased even more from $309 million to $585 million since 2005.

European exports to the US have fallen by approximately 5% in volume over the past 12 months, reducing European growth by around 0.2% in 2025. The trade has also slowed down to around €1.1 trillion per year. Certain sectors, particularly automotive, machine tools, and chemicals, have been more severely affected.

This can impact the EU, but the good news is that its total exports to the US are only 3% of the GDP. With the 10% increase in tariff, it may slow the EU’s growth by 0.2% to 0.5% in the medium term, which may balance in the long term based on the EU members’ exposure to the US economy. For instance, the impact would be severe on Germany compared to Estonia.

Grozoubinski said, “Use and threat of financial measures is not unprecedented in disputes between countries, but to have the EU raising it as a possibility against the US certainly elevates the stakes and the playing field. While trade is generally considered at least somewhat resilient and adaptable, making up a small enough part of most economies for them to survive turbulence and tension, financial instruments are generally treated with more care. Anything which might spook bond markets and raise the cost of government borrowing and the servicing of government debt, for example, is generally avoided. This makes the willingness of the EU to talk about using financial measures, and thus broaden the ‘battlefield’ into that sector a somewhat new development, given the sheer size of the two markets involved.”

George Riddell, Managing Director at Goyder Ltd, a trade consultancy, noted that, “Traditionally, the EU has dealt with trade wars through the imposition of tariffs – which is what we saw through the 2000s with the US-EU Airbus-Boeing dispute – where Harley Davidsons and scotch whiskey got caught in the cross-fire. The ACI gives the EU the ability to respond beyond tariffs, by imposing restrictions on services, digital, intellectual property, and financial services.

He also said that the EU has never triggered the ACI, and EU Member State governments have made it clear that there is a high bar to do so. “There is much we don’t know about how the retaliation will be decided and against what sectors. If the EU authorities were to target US treasury bond holdings by European nations and investors, it would constitute an unprecedented move.”

It is to be noted that EU investors are heavily invested in the US market, owning $8 trillion in US stocks and bonds. $3.6 trillion of that is in the US Treasury alone. This is 10% of the US Treasury market size.

While a large sell-off may seem unlikely, the EU can hit where it hurts. For instance, Alecta (Swedish pension fund) sold most of its Treasury holdings worth 70-80 billion Swedish kronor ($7.7–8.8 billion) from 100 billion kronor. Denmark’s AkademikerPension have also sold $100 million worth of Treasury.

EU’s Nordic alliance

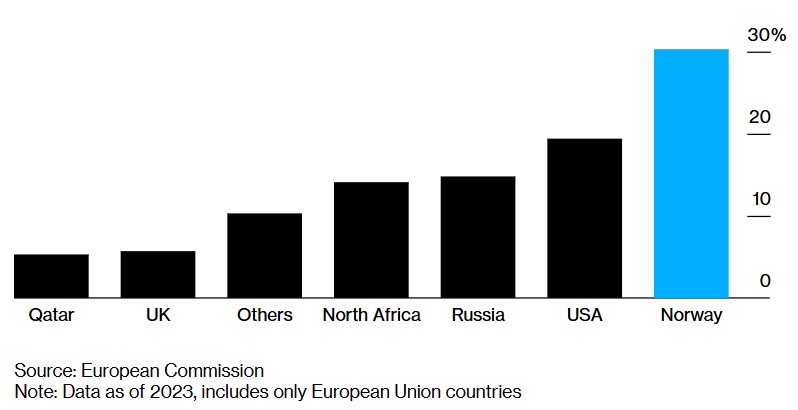

A crucial factor strengthening Europe’s position is that Trump’s latest tariffs also affect Norway. Norway’s role is particularly significant given Europe’s energy vulnerabilities. Since Russia’s invasion of Ukraine, Norway has overtaken Russia to become the EU’s most important supplier of natural gas, with the US ranking second. Norway’s Equinor supplies 30% of natural gas to the EU compared to 35% by Russia’s Gazprom PJSC.

Coordinating with Oslo could reduce Europe’s dependence on American liquefied natural gas (LNG), removing an important lever of economic pressure from Washington’s arsenal.

Such coordination with affected non-EU states is explicitly provided for in Article 7 of the EU anti-coercion regulation. This can strengthen the impact of any countermeasures while reducing political opposition within the bloc.

Economic risk against political sovereignty

European policymakers face a delicate calculation in deciding whether to activate the ACI. While a trade war with the US would likely damage both economies, a failure to respond to perceived coercion could fatally undermine the EU’s credibility.

As tensions escalate, European leaders face their most consequential decision on transatlantic relations in a generation.

French President Emmanuel Macron has been among the most vocal advocates for a robust response, reportedly urging the EU to deploy its trade “bazooka” against Washington.

For the moment, Europe’s trade tool remains holstered, but with fingers increasingly close to the trigger. If implemented, it can change the global trade.