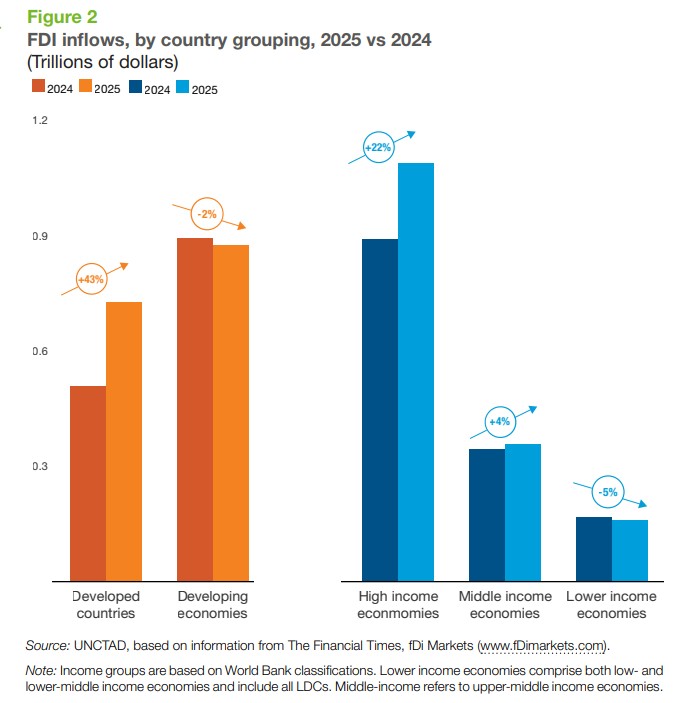

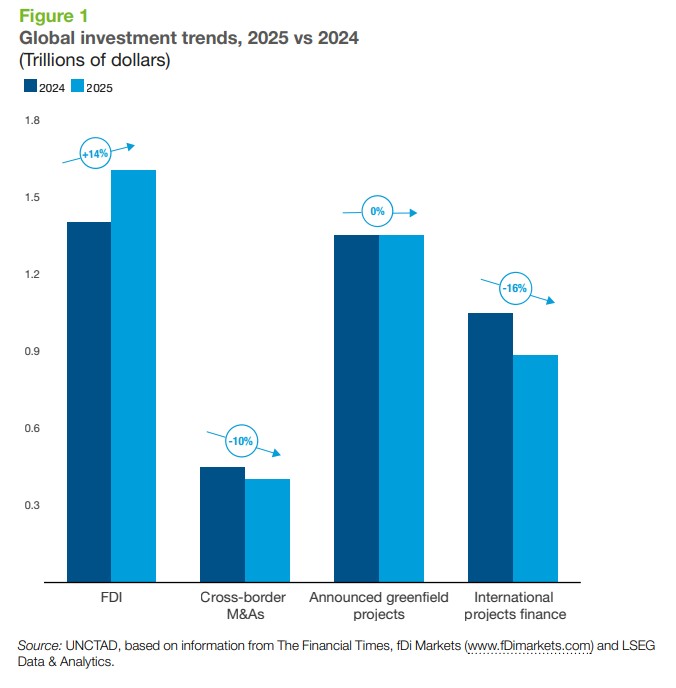

Global foreign direct investment (FDI) flows increased by 14% in 2025, reaching an estimated $1.6 trillion, according to the latest UNCTAD Global Investment Trends Monitor. Developed markets benefited from a surge of over $140 billion in inflows, largely concentrated in global financial centres. This rise was largely driven by significant inflows into developed economies, which experienced a 43% increase to $728 billion.

In contrast, developing economies saw a 2% decline in FDI, totalling approximately $877 billion and accounting for 55% of global flows. Notably, three-quarters of the least developed countries (LDCs) reported stagnant or declining investment.

This decline reflects challenges such as geopolitical tensions, economic fragmentation, and policy unpredictability, which have dampened investor confidence in emerging markets.

A stark contrast in FDI investment in high-income vs low-income countries

FDI increased by 22% in high-income economies and by 4% in middle-income economies, while declining 5% in lower-income countries.

The rise in FDI to high-income economies was largely fueled by increased flows to financial centres and investment hubs, with several major recipient countries also experiencing growth. FDI to the European Union surged 56%, with Germany, France, and Italy all recording higher inflows supported by increased cross-border mergers and acquisitions (M&A).

Germany’s FDI rebounded to an estimated $50 billion after a low in 2024, while France and Italy saw inflows rise 45% to $39 billion and 53% to $34 billion, respectively.

In high-income Asian economies, FDI inflows decreased in Hong Kong and South Korea but increased in Singapore, Israel, and Saudi Arabia. In Oceania, Australia’s FDI fell by one-third to $34 billion, driven by a 62% drop in cross-border M&A activity.

FDI into middle-income economies increased, with Latin America and the Caribbean recording the strongest growth at 24%. Brazil experienced a 42% rise in FDI, while Mexico registered a 16% increase.

Chinese FDI declined for the third consecutive year, falling 8% to an estimated $107.5 billion, with investments primarily concentrated in strategic and high-growth sectors. By contrast, Thailand and Türkiye recorded robust FDI growth of 35% and 29%, respectively.

FDI flows to lower-income economies fell by 5% to $159 billion, raising concerns over their access to external financing. Angola saw inflows of $3 billion, ending nine years of net divestments. Meanwhile, Egypt remained Africa’s largest FDI recipient.

Mozambique saw an 80% increase in inflows to $6 billion, attributed to the resumption and acceleration of major LNG project construction.

In Asia, India recorded a 73% surge in FDI to $47 billion, primarily driven by substantial investments in services, including finance, information technology, and research and development, as well as manufacturing. This growth has been supported by policies designed to integrate India into global supply chains.

Weakness in new project announcements and M&A activity

In 2025, international investment deals and project announcements showed mixed results.

While the value of greenfield projects in industrial sectors stayed high, supported by mega-projects in developed countries, the number of announced projects dropped by 16%, reflecting a cautious investment environment.

International project finance, mainly infrastructure-related, declined for the fourth consecutive year, with values dropping 16%. This sustained downturn signals persistent challenges in mobilising capital for cross-border infrastructure development, particularly in emerging markets.

Cross-border M&A values decreased by 10%, despite a surge in domestic deal activity. The decline in international M&A shows increased policy uncertainty and geopolitical risks, which have constrained cross-border corporate transactions.

Data centres and semiconductors lead, declines in GVC-intensive sectors

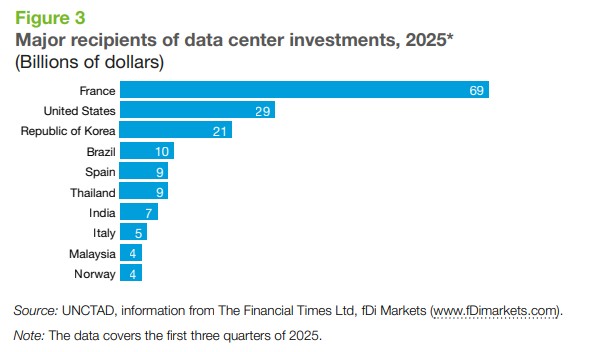

Sectoral analysis reveals a reshaping of the FDI landscape. Data centres now constitute one-fifth ($270 billion) of global greenfield project values, reflecting the growing strategic importance of digital infrastructure in the global economy.

Leading hosts included France, the United States, and South Korea, with emerging markets like Brazil, Thailand, India, and Malaysia also ranking among the top ten (see figure 3). MGX from the UAE announced a $43 billion AI campus project in France, followed by $74 billion in U.S. greenfield investments, $28 billion from China, and $25 billion from Canada.

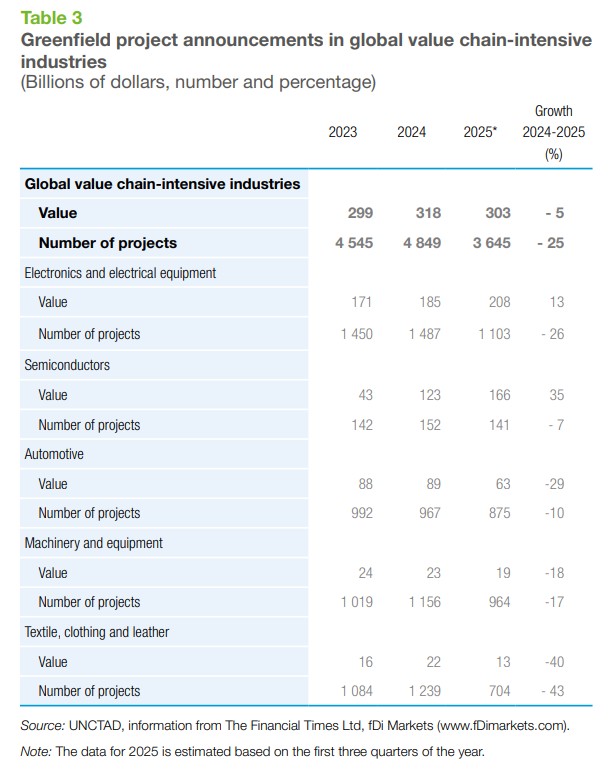

The semiconductor sector also saw a 35% increase in the value of newly announced projects, driven by rising demand and policy support in key markets. In contrast, sectors heavily exposed to tariff-related global value chain (GVC) disruptions, such as textiles, electronics, and machinery, experienced sharp declines in project numbers, down 25%. This contraction signals ongoing challenges in industries vulnerable to trade tensions and supply chain realignments.

For the first time, telecommunications investment value overtook renewable energy, though renewable energy still leads in project count. International project finance in renewable energy decreased by 7%, reaching a four-year low due to investor concerns over revenue risks, uncertain returns, and regulatory challenges.

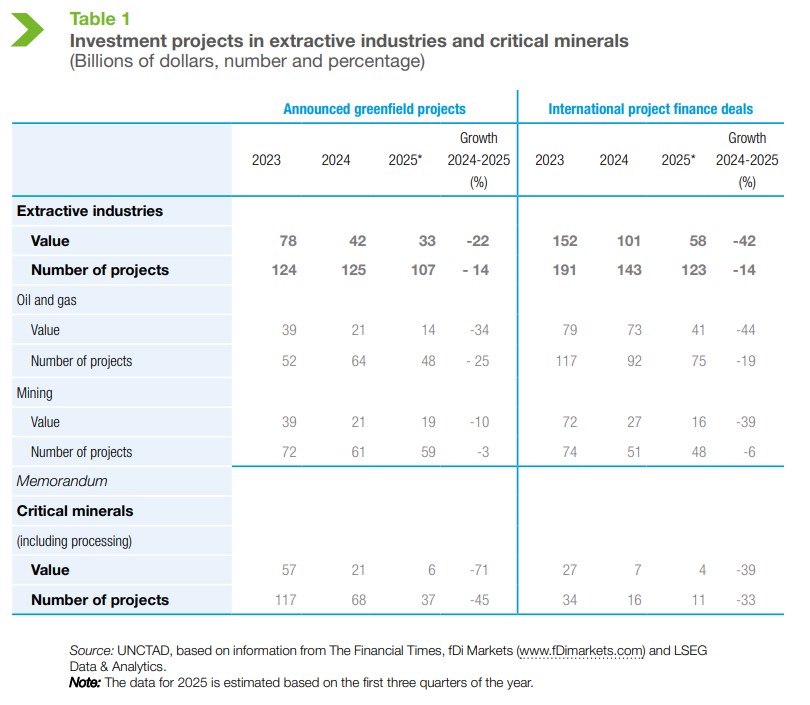

Investments in extractive industries and critical minerals also fell in 2025, with project values down 36% and the number of projects down 14%.

Critical minerals investment plummeted to $10 billion, a 63% drop from 2024, driven by low energy prices and volatile mineral markets, which have made investors more cautious.

Outlook for 2026

Outlook for 2026

Looking ahead, there is potential for increased FDI flows in 2026, supported by projections of easing inflation and borrowing costs in major markets. A rebound in M&A activity could further stimulate cross-border investment.

However, downside risks remain. Geopolitical tensions, regional conflicts, and economic fragmentation are likely to suppress project activity, concentrating capital expenditures in a limited set of strategic industries, particularly data centres and semiconductors. Investors and policymakers need to focus on sectors with strong growth potential and create stable policies to attract and maintain investment.