By: Scott Sanchon, Trade Treasury Payments

Geopolitical shocks are once again rippling through the global energy market. The Middle East conflict is driving up prices and disrupting trade across the European Bank for Reconstruction and Development’s (EBRD) regions.

The conflict in the Middle East has significantly driven up energy and fertiliser prices. The disruption had a detrimental impact on global trade and tourism, resulting in global economic regression. On March 20, liquified natural gas (LNG) production in Qatar was damaged by this conflict. The price of natural gas in Europe more than doubled, surpassing $100 per barrel on 9 March 2026. As the Strait of Hormuz remains in conflict, around 14 per cent of world energy production could be shut off.

A new report from the EBRD on the potential economic impact of the conflict in the Middle East assessed the conflict in the region that can drive an increase in pricing globally.

From 2011 to 2014, the price of oil remained below the levels and gas prices have yet to reach the peak levels seen since 2022. The Strait of Hormuz, if it remains off-market, could potentially skyrocket the price of oil to $180 per barrel. The higher price, in the longer term, will destroy demand and relocate supply elsewhere, which might bring the price back down to around $100.

“The conflict shows how quickly geopolitical shocks can ripple through energy markets, supply chains and financial conditions,” said Beata Javorcik, EBRD Chief Economist.

“Rising energy prices come at an already challenging time for the European manufacturing sector, while the broader fallout from the conflict is likely to strain government budgets already overstretched by high defence spending in central Europe and elevated debt-servicing costs in the southern and eastern Mediterranean and sub-Saharan Africa. The effects of the conflict are likely to linger beyond the end of hostilities.”

Despite this economic disruption, commodity exporters are expected to benefit from this geopolitical tension. However, the significant constraints will impact import-dependent economies. The growth forecast for the EBRD regions is forecast to drop by 0.4 per cent. Moreover, higher fertiliser costs, driven by disruptions, are driving up food prices. Supply chain disruptions will affect material prices. Economies that rely on trade and tourism, particularly those that are tied to the Strait of Hormuz, especially in the Middle East, North Africa and Eastern Europe, are expected to encounter severe economic challenges.

The economic impact across EBRD regions

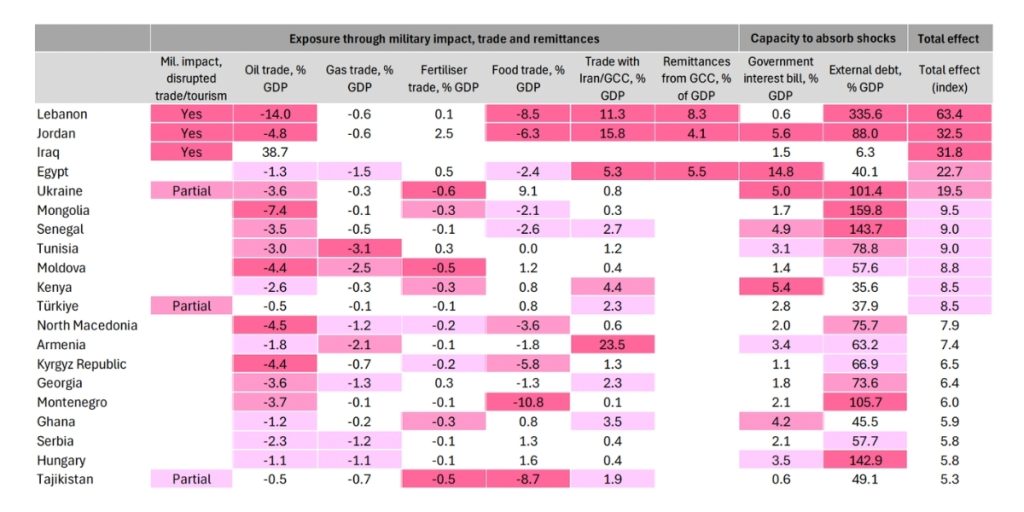

Exhibit 1: Economies in the EBRD regions that are most impacted by the war in the Middle East (Source: European Bank for Reconstruction and Development (EBRD), 2026, p. 4)

The conflict was expanded in February 2026, when the US and Israel launched major air and missile strikes on Iran, leading to retaliatory attacks by Tehran across the region.

The increase in energy prices reflects this conflict widely on the supply chain infrastructure and transport route through the Strait of Hormuz. For example, the LNG production in Qatar was equivalent to approximately 20 per cent of global supply, accounting for a significant share of global energy supply. As a consequence, Qatar halted its production of LNG on 2 March. Furthermore, shipping activity through the Strait of Hormuz has fallen, reflecting higher insurance costs and elevated security risk. At the same time, these impacts have curtailed global oil shipping activity through the Strait. With around 18 per cent of global energy supply passing through this route, rerouting remains severely critical.

Energy Markets Tighten as Prices Surge

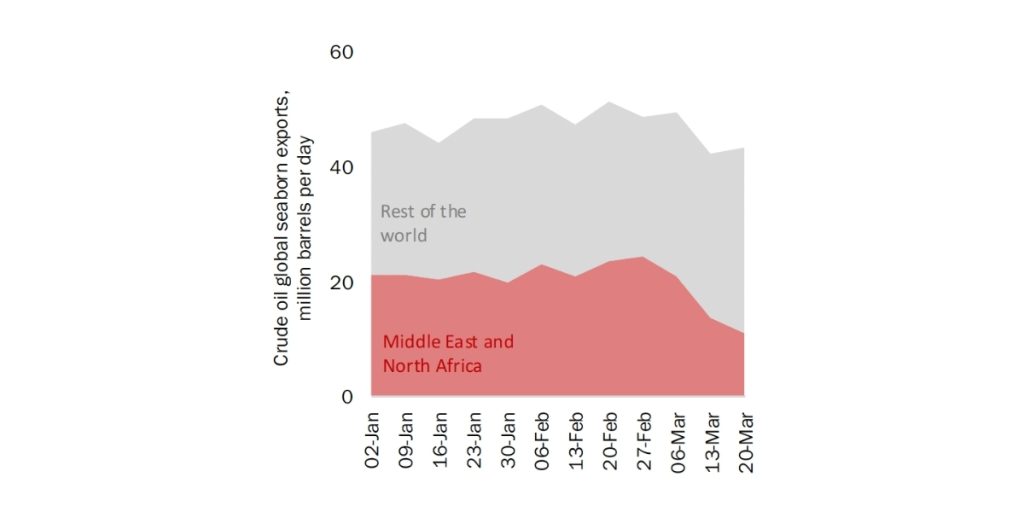

Exhibit 2: Seaborne exports of crude oil from the Middle East and North Africa fell by around 10 mbd between February and mid-March 2026 (Source: European Bank for Reconstruction and Development (EBRD), 2026, p. 5)

The energy market in Europe has come under increasing pressure as supply disruptions intensify across production. As a result, gas prices in the region more than doubled by 19 March 2026. The gap between the price of gas in the US and in Europe widened to nearly 6 times.

While LNG from the Strait of Hormuz accounts for a small share of global gas consumption, LNG plays an important role in connecting fragmented regional gas markets and thus setting the price of gas. Seaborne crude export from the Middle East and North Africa declined by approximately 10 million barrels per day from February to mid-March 2026, illustrating the negative impact on the global supply chain.

Brent crude oil prices surpassed $100 per barrel in March 2026. In response, the International Energy Agency pledged to announce the release of 400 million barrels from oil reserves. Nonetheless, the reserve energy could be supplied to the market at a rate equivalent to 1-3 per cent of global oil production daily. The logistical constraints are expected to limit the pace at which these reserves of LNG could be supplied to the market.

Financial pressures mount as energy shock reshapes global markets’ risk

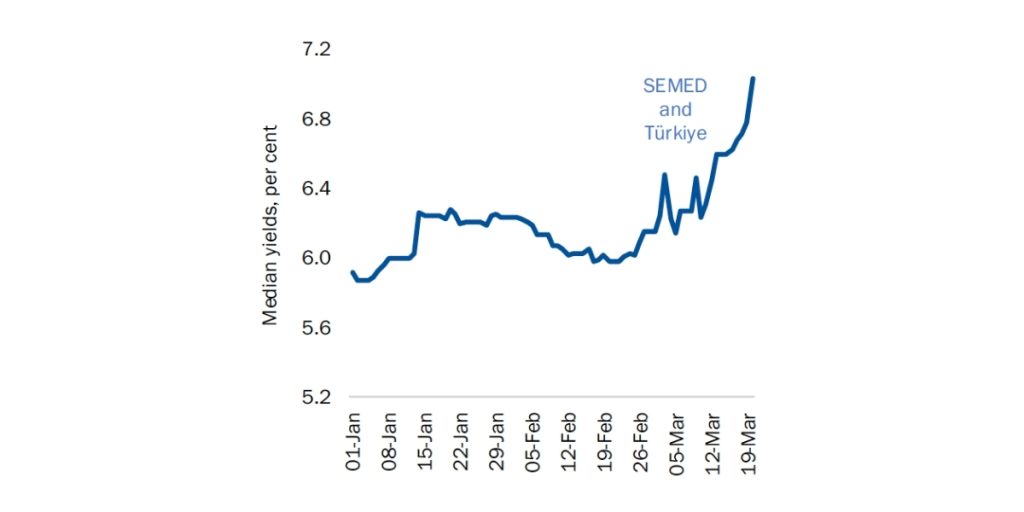

Exhibit 3: Bond yields have risen in the southern and eastern Mediterranean and Türkiye (Source: European Bank for Reconstruction and Development (EBRD), 2026, p. 17)

Rising energy prices and supply chain disruptions are expected to tighten global financing conditions, increasing borrowing costs for economies exposed to the conflict.

Countries with greater exposure to the war may experience an additional risk premium, similar to the risk premium paid by economies in central and south-eastern Europe after Russia’s invasion of Ukraine in 2022.

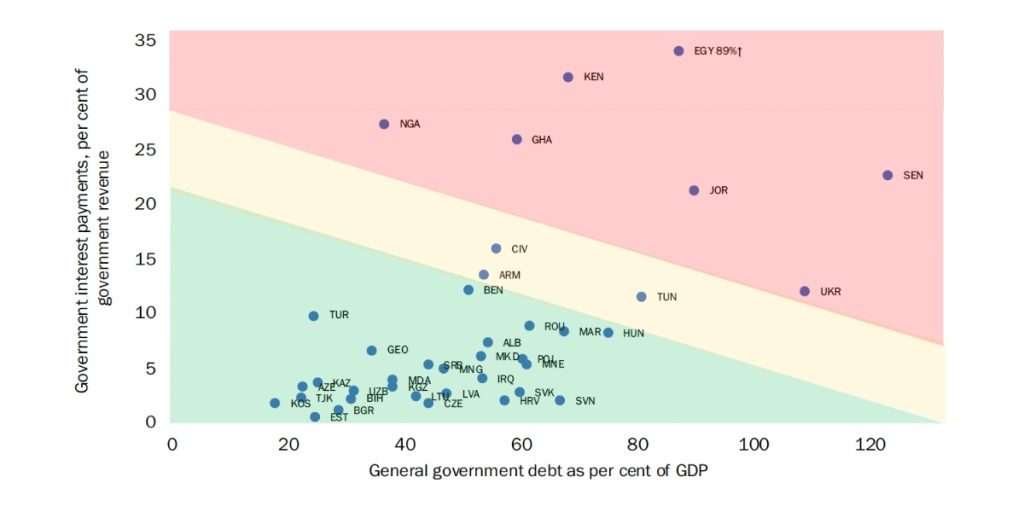

The conflict is compounding pre-existing fiscal vulnerabilities across EBRD regions. A number of economies in the region were facing both high ratios of government debt to GDP and high interest payments. For instance, in Egypt, interest payments reached 89 per cent of government revenues in 2025, followed by estimated to account for over 30 per cent of revenues in Kenya and 20 per cent in Nigeria.

Exhibit 4: Even before the conflict, some economies in the EBRD regions were facing fiscal pressures (Source: European Bank for Reconstruction and Development (EBRD), 2026, p. 17)

In the end, the conflict may reinforce the importance of energy security and accelerate the fragmentation of international trade. Economies in the EBRD regions that are dependent on energy imports, fertilisers, and food and have strong ties to the Gulf will encounter the most impact, such as Egypt, Iraq, Jordan, Kenya, Lebanon, and Türkiye. With energy trade increasingly concentrated along political alignment, this rising political tension illustrates the growing fragmentation of international economies.

The EBRD has stated that it is ready to support its clients and countries of operations in managing the economic impact of ongoing developments in the Middle East.