Credit cycles tighten while pricing holds

The International Credit Insurance and Surety Association (ICISA) has released its latest business sentiment survey. According to the results, which cover both trade credit insurance and surety, demand looks steady, expectations for losses are rising, and pricing has stayed largely unchanged.

Credit cycles tighten while pricing holds

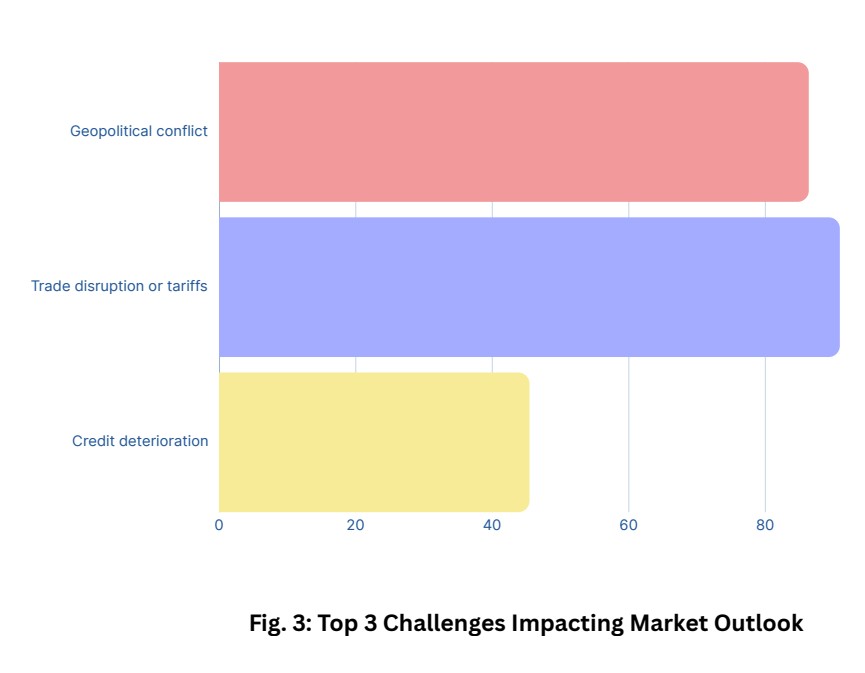

The near-term picture is shaped by credit deterioration, geopolitics, and trade disruptions or tariffs. A clear majority of TCI respondents expect more claims in the next year and a sharper rise in insolvencies, while surety respondents also tilt toward higher claims and insolvency risk.

The survey records that 59% of TCI respondents expect claims to increase and 77% expect insolvencies to rise. On the surety side, 42% expect claims to increase and 62% anticipate higher insolvencies. Yet most still describe pricing as broadly stable.

Underwriters are cautious about sector and counterparty selection, but capacity is available and programmes continue to be broker-led, particularly for complex cross-border arrangements. Brokers are the primary channel by a wide margin, accounting for 68% in TCI and 71% in surety, which reflects the value of intermediation in assembling multi-insurer placements and managing multi-jurisdictional documentation.

AI moves from exploration to execution

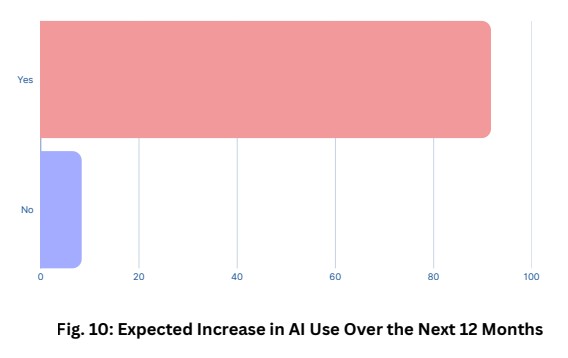

The most decisive trend in the survey is technology adoption. Members expect to scale AI quickly over the next 12 months, with underwriting the focal point and claims and modelling following close behind. The survey shows that 94% of TCI and 92% of surety respondents plan to increase AI use, with underwriting being the highest-impact domain. The main execution constraint is talent, as firms report difficulty hiring and retaining digital and data skills.

Embedding AI in risk selection and limit management can tighten response times to buyer deterioration, sharpen portfolio steering, and support more granular risk sharing with banks and factors. In practice, that means faster limit decisions, earlier stress signals, and cleaner connectivity into structured stacks where capacity can be syndicated or top-upped.

ICISA’s analysis suggests the near-term winners will be those who hard-wire AI into underwriting workflows and use broker ecosystems to assemble flexible risk-sharing arrangements at scale.

ESG opportunity is real, data is still catching up

That brings us to ESG. Around one third of respondents across both lines have updated ESG policies in the past six months. Opportunities appear to be concentrated in capital-intensive segments such as renewables, energy efficiency, and green construction, that have more predictable project pipelines. The survey indicates that there is a strong interest among the surety market in renewables alongside green construction.

The challenge, however, is finding the best ways to measurement ESG impacts and deciding how to price them. Members flag a persistent ESG data problem, which has historically been driven by inconsistent definitions of what counts as a green risk and uneven standardisation across markets.

Over the medium term, respondents expect greater automation to be highly likely and ESG to become a more consistent rating factor, while regulatory fragmentation will remain a concern to watch.

Financial institutions remain central to market structure

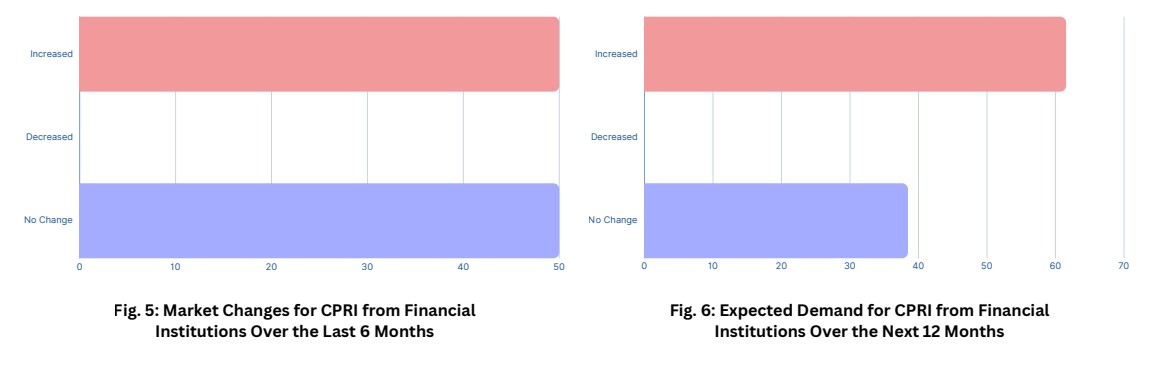

The link between insurers and lenders continues to shape demand with banks and factors relying on TCI and CPRI for capital relief and exposure management, while surety demand is tied to bank regulation. Among those active in CPRI, half saw increased financial-institution activity in the past six months and nearly two-thirds expect growth over the next year. Capital relief is the dominant driver, followed by limit and exposure management.

The distribution implications are straightforward. As risk-weighted asset pressures ebb and flow, brokered programmes that blend whole-turnover cover with facultative or top-up capacity are likely to remain the working template. That model fits an environment where losses may trend higher, but where is still strong competition on price and execution quality.

The direction of travel

According to the ICISA survey credit conditions are tighter, but insurers are remaining active partners to trade and infrastructure. Technology is moving from pilot to production, particularly in underwriting. ESG is maturing from policy statements to selective deal flow where data supports risk selection. And distribution is anchored to broker intermediation and bank-linked channels that can translate coverage into financing capacity.

For readers who want the detail behind the numbers, the full ICISA Business Sentiment Survey 2025 sets out the data, structures, and market signals, including line-by-line views on pricing, insolvencies, financial-institution demand, and operational priorities for the next year.

You can read the full ICISA Business Sentiment Survey 2025 here.

Article Info

Related Articles

Emerging Markets +4

Emerging Markets +4Are stablecoins a geopolitical issue?

By: Joy Macknight While artificial intelligence (AI), ranging from machine learning to agentic commerce, dominated...

Payments +2

Payments +2Issue 05 – Fine Print: Looking Beyond the Headlines

Scott Sanchon, Trade Treasury Payments “We live in an age that rewards the headline.” Every...

Cash Management +6

Cash Management +6TTP Studios, on the record

By: James Dorman and Deepesh Patel A comfortably-furnished room under the railway arches of Central...

Bills of Lading +5

Bills of Lading +5Beyond the headlines: A foreword to the fine print of global finance

A note from the editors We live in an age that rewards the headline. Every...

Stay Ahead of the Curve

Get exclusive insights, expert analysis, and breaking news on liquidity and risk management, delivered to your inbox

Article Info

Stay Updated

Get the latest insights on trade finance, treasury management, and global payments delivered to your inbox.

Join 25,000+ professionals. Unsubscribe anytime.