Cross-border payments often face delays. This includes high costs and inefficiencies, particularly for retail transactions like remittances and person-to-person transfers. Despite many attempts to improve these processes, issues with foreign exchange (FX) and settlement continue to remain challenges.

To transform this and make reliable, low-cost cross-border payments the new norm, Project Rialto was launched in 2024.

What is Project Rialto?

It is a technical experiment designed to explore how instant cross-border payments can be improved by integrating existing instant payment systems with tokenised central bank money (CeBM) and automated FX mechanisms.

The project, a collaboration between the Bank for International Settlements (BIS) Innovation Hub, the Bank of France, the Bank of Italy, Bank Negara Malaysia, and the Monetary Authority of Singapore, tests a proof of concept (PoC) that connects non-tokenised retail payment systems with tokenised FX and settlement.

The goal here is to showcase that retail cross-border payments can be executed instantly and securely with minimal changes to current infrastructure, while overcoming the traditional bottlenecks of FX conversion and settlement delays.

How does Rialto work?

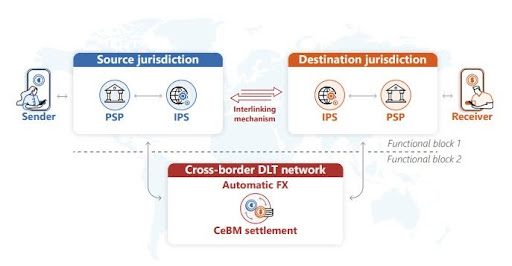

Rialto combines three key components:

- Instant Payment Systems (IPS). The project links existing retail instant payment systems across different jurisdictions, enabling near real-time payment initiation and receipt.

- Automated Market Makers (AMMs): These decentralised liquidity pools automatically price and execute FX conversions using bonding curves, eliminating the need for traditional FX intermediaries.

- Tokenised Central Bank Money (CeBM): Settlement occurs using tokenised versions of central bank money, ensuring a safe and trusted finality of payment.

The PoC successfully tested direct transactions between senders and receivers in different countries and currencies. It also explored the use of a vehicle currency to facilitate exchanges in low-liquidity corridors or when a third currency is needed. The system maintained resilience and integrity even under scenarios involving errors, malicious activity, or disruptions.

One of Rialto’s standout features is that it requires only minimal changes to existing payment infrastructures. This means banks and payment operators can upgrade their systems without costly overhauls. The ability to connect traditional payment rails with tokenised settlement layers opens the door to widespread adoption.

What is the significance of the project?

Cross-border retail payments today often take hours or even days to settle. This delay is expensive financially, and also in terms of trust and convenience. FX and settlement frictions add layers of complexity and risk, especially for smaller transactions like remittances that are vital for millions worldwide. Rialto’s approach enables payment-versus-payment (PvP) settlement in tokenised CeBM, meaning currency exchange and settlement happen simultaneously and atomically.

This reduces settlement risk. By using AMMs, Rialto automates FX pricing and liquidity provision, potentially lowering transaction costs and boosting transparency compared to traditional FX markets.

Yet, technical feasibility is only half the story. The system’s economic viability depends on competitive fee structures, robust performance under varying market conditions, enhanced market transparency, and efficient liquidity and capital utilisation. AMMs typically charge fees based on liquidity pool usage, which could be more efficient than legacy FX spreads and correspondent banking fees. However, AMMs must maintain liquidity and pricing accuracy even during volatile or low-liquidity periods to ensure reliable FX execution.

Tokenisation and distributed ledger technology (DLT) can enhance transparency here by creating an immutable, real-time record of transactions accessible to all authorised participants, but regulators and market participants must ensure system integrity and guard against manipulation. Financial institutions stand to benefit from more efficient capital use, as tokenised settlement reduces the need for pre-funding accounts in multiple currencies.

The Rialto experiment’s findings suggest these economic dimensions are promising.

However, the path ahead requires further testing and regulatory alignment before this innovative approach can become mainstream.

The role of the FX provider in managing slippage and price certainty

One of the most important yet less discussed elements of Project Rialto is the introduction of the Foreign Exchange Provider (FXP) as a specialised intermediary that bridges the gap between the AMM model and the stringent requirements of retail instant payments.

AMMs cannot promise a fixed exchange rate at the time of a quote. This is because they use an algorithm based on liquidity pools to set prices, which can lead to rate slippage. Rate slippage is the risk that the executed exchange rate differs from the quoted rate.

In retail payment systems such as Rialto, it is crucial to guarantee that the exchange rate stays the same from the quote to the execution. This helps build consumer trust and helps meet regulations. The FXP addresses this problem by offering a binding quote and bearing the risk.

When a payment request is made, the FXP gets a quote request from the IPS link, retrieves the rate from the AMM, and then offers a binding quote, committing to that rate.

If the AMM cannot meet the agreed rate during the automatic settlement because of slippage, the FXP will cover the difference from its own reserves. This ensures that the receiver gets the exact amount that was committed.

On the other hand, if the AMM’s rate favours the FXP, the FXP reaps the benefits.

This shifts the slippage risk from payment service providers (PSPs) and end users to the FXP, which manages it through spreads and fees.

The FXP provides stable and predictable pricing, which is important for accepting retail payments and compliance. This approach combines automation with effective risk management.

While FXP absorbs slippage risk and provides binding quotes, it also adds costs, including fees and spreads.

The FXP model supports incremental adoption by allowing existing PSPs to continue operating without direct exposure to AMM volatility, while still benefiting from the efficiencies of tokenised settlement and automated FX.

What’s next for Project Rialto?

While the PoC has showcased technical feasibility, the journey toward full-scale deployment needs to address regulatory, operational, and market challenges.

There are still concerns around interoperability with other payment systems, cross-border regulatory compliance, and the scalability of AMM liquidity pools.

Nonetheless, we can say that the momentum is clear. Central banks and financial institutions are increasingly exploring tokenised money and DLT-based settlement as the future of payments. Amidst this, Rialto offers a glimpse of a future where cross-border payments are as fast and frictionless as domestic payments.

Learn more about Rialto here.