Exporter compliance frameworks frequently rely on Incoterms® to determine where customs, VAT, sanctions exposure and contractual risk transfer between parties.

International Commercial Terms, which are commonly known as Incoterms® rules, are defined by the International Chamber of Commerce as: ‘a set of eleven three-letter trade terms, reflecting business-to-business practice in contracts for the sale and purchase of goods’. First published by the ICC in 1936, Incoterms® are usually revised every 10 years. The latest edition was released in 2020.

These global standards provide a common ground and define delivery, risks, and responsibilities between sellers and buyers and the allocation of costs.

Incoterms® also clarify which party in the transaction (in the sales contract) is responsible for export/import clearance and for paying taxes and duties. There are 11 Incoterms®, each representing different delivery terms and conditions. Their terms (and corresponding clauses) have been developed to suit more recent transport modes/scenarios and societal demand.

Incorporating them into the sales contract clarifies each party’s obligations, and although Incoterms® are not compulsory, once agreed upon and used, they become legally binding. They play a key role in international sale contracts, and their correct use is integral to best practices within customs and trade compliance.

Both parties to the transaction should have a clear understanding of the responsibilities, costs and risks associated with the agreed Incoterms®, not only to avoid unnecessary issues during audits, but also to manage the risk exposure (especially when using the more extreme/higher risk terms such as EXW or DDP), and mitigate the likelihood of legal disputes.

The Incoterms® 2020 book containing full rules can be purchased through the official ICC website. The practical wallchart illustrating where risks and costs are split/passed on from the seller to the buyer can be downloaded free of charge (upon creation of a free user account). Incoterms® are divided into ‘Any mode of transport’ and ‘Inland waterway / Sea transport’, and the following categories:

- Group E – Departure (EXW)

- Group F – Main carriage unpaid (FCA, FAS and FOB)

- Group C – Main carriage paid (CFR, CIF, CPT and CIP)

- Group D – Arrival (DAP, DPU and DDP)

Each Incoterms® 2020 rule is further explored below.

Incoterms® 2020

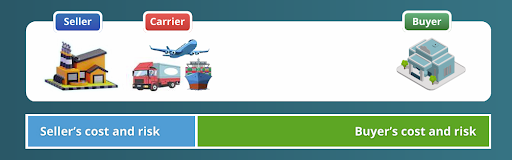

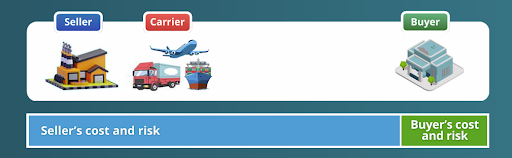

The full and correct reference to the Incoterms® is crucial from both a legal and compliance standpoint, and also because of differences between versions, such as those published in 2010 and 2020. Abbreviated references such as ‘DAP 2020’ or ‘FCA’ are not sufficient, because they do not specify the point of delivery or the named destination/place, which can easily create uncertainty. To support best practice, the full wording and reference should always be used by writing, for instance, FCA named place of delivery, Incoterms® 2020 (e.g., ‘FCA Unicar Cheltenham, UK, Incoterms® 2020’) or DAP named place of destination, Incoterms® 2020 (e.g., ‘DAP MetalWorld Sp. zoo Krakow, Poland, Incoterms® 2020’). This logic should be consistently applied across all terms. The following diagrams describe each Incoterms® rule: the mode of transport, allocation of costs and where responsibilities are passing from the Seller/Exporter to the Buyer/Importer:

| Incoterms® 2020 | Mode of transport | Description |

| EXW – Ex Works (named place of delivery) | Any | Under EXW, the buyer/importer is responsible for all costs. The risk transfers from the seller to the buyer once the goods are made available for collection at the named place, and loading onto the vehicle is at the buyer’s risk. EXW is generally more suitable for domestic trade, as it can create complications for the seller/exporter in providing proof of export, which is further explored in section 4.3.

Alongside DDP, this term is commonly considered ‘higher risk’. |

|

||

| FCA – Free Carrier (named place of delivery) | Any | The buyer is responsible for contracting the carrier and for all costs; however, the seller arranges for export clearance/formalities. Risk passes from the seller to the buyer once goods are ‘delivered’ to the carrier (placed at the disposal of the carrier) or loaded onto the vehicle at the seller’s premises (named place).

This term is commonly recommended to be used instead of EXW. |

|

||

| CPT – Carriage Paid To (named place of destination) | Any | Under CPT, the seller pays for the carriage and associated costs to the named place/point (blue area in the illustration below), and is responsible for export clearance. The buyer covers import duties and taxes (and associated import clearance costs). However, the risk for loss or damage transfers from the seller to the buyer once goods are ‘delivered’ to the carrier (placed at the disposal of the carrier) or loaded onto the vehicle at the seller’s premises (named place) – green area in the illustration. |

|

||

| CIP – Carriage and Insurance Paid To (named place of destination) | Any | The seller is responsible for paying for transport to the named place of destination and is required to contract for clauses (A) insurance (Institute of Cargo Clauses “IoCC”), or similar. Risk to loss or damage passes when the goods are ‘delivered’ to the carrier (placed at the disposal of the carrier). Similar to CPT, the seller handles export formalities, and the buyer is responsible for import clearance. |

|

||

| DAP – Delivered at Place (named place of destination) | Any | One of the most widely used Incoterms®. The seller pays for transport costs to the named destination (usually the buyer’s premises) and is responsible for export formalities, whereas the buyer is responsible for import taxes and duties. The risk of loss or damage passes from the seller to the buyer when goods are delivered to the named place and are made available for unloading. It is important to note that the unloading of goods is at the buyer’s risk. |

|

||

| DPU – Delivered at Place Unloaded (named place of destination) | Any | New term under the 2020 version. The seller pays for the transport and delivers to the named place, and is responsible for unloading the goods (risk passes from the seller to the buyer once the goods are unloaded, as opposed to DAP).

In the 2020 edition, DPU replaced the previous Incoterms® DAT (Delivered at Terminal, Incoterms® 2010). The new term allows for delivery to locations other than a Terminal or Quay, such as the buyer’s premises. |

|

||

| DDP – Delivered Duty Paid (named place of destination) | Any | The seller covers transport costs and is responsible for all export and import clearances and formalities, including covering import VAT and duties (the seller must be registered in the importer’s country for tax and duty purposes). The risk of loss or damage passes once goods are ready to be unloaded at the named destination. DDP should be used with extra caution due to the seller being exposed to extra formalities at the destination country, where costs can be difficult to plan and procedures to navigate (it is a ‘higher risk’ term). |

|

||

| FAS – Free Alongside Ship (named port of loading) | Sea and Inland Waterway (non-containerised) | The seller ‘delivers’ by placing goods alongside the vessel at the named port of departure. Responsibility passes from the seller to the buyer once the goods are delivered to and unloaded at the named port. The buyer pays for the carriage from the named port of departure and is responsible for import taxes and duties at the final destination.

FAS is not suitable for FCL (full container load) or LCL (less than container load) transactions, because it is for non-containerised goods. |

|

||

| FOB – Free on Board (named port of loading) non-containerised | Sea and Inland Waterway (non-containerised) | The seller arranges for the export clearance and is responsible for ‘delivering’ (by placing goods on board the vessel at the named port of departure), at which point the risk of damage or loss transfers to the buyer. Good practice amongst parties in the transaction is to specify the ‘on-boarding’ (if it means ‘passed over the ship’s rail’, or something else) separately in the sales contract for extra clarity around the risk transfer, if required. The buyer pays for the carriage from the named port of departure and is responsible for import taxes and duties at the final destination.

FOB is not suitable for FCL (full container load) or LCL (less than container load) transactions, because it is for non-containerised goods. |

|

||

| CFR – Cost and Freight (named port of destination) | Sea and Inland Waterway (non-containerised) | The seller pays for the transport of goods to the named port of destination, but the risk passes from the seller to the buyer once the goods are delivered to the port of departure and are on board the ship.

CFR is not suitable for FCL (full container load) or LCL (less than container load) transactions, because it is for non-containerised goods. |

|

||

| CIF – Cost, Insurance and Freight (named port of destination) | Sea and Inland Waterway (non-containerised) | The seller pays for the transport of goods to the named port of destination and is responsible for export formalities. The risk passes from the seller to the buyer once the goods are delivered to the port of departure and are on board the ship. Seller must contract for the insurance with the buyer being the beneficiary, and the buyer is responsible for import formalities/clearance.

CIF is not suitable for FCL (full container load) or LCL (less than container load) transactions, because it is for non-containerised goods. |

|

||

Please note that these Incoterms® rule diagrams are for indicative purposes, showing the general division of costs and risks under each Incoterms® 2020 rule. For the exact and detailed provisions, exporters should always refer to the official ICC publication.

For deeper analysis of Incoterms®, customs risk, and exporter obligations across jurisdictions, explore the full Exporters Guide here