Claims and recoveries form one of the most important stages in the lifecycle of a trade credit insurance policy as they are the point at which credit insurance proves its worth. When a buyer defaults, the claims process determines whether the policyholder is compensated and how quickly. For the insurer, it is the test of paying valid claims while protecting against losses that fall outside the policy. This chapter explains how claims are handled.

The claims timeline

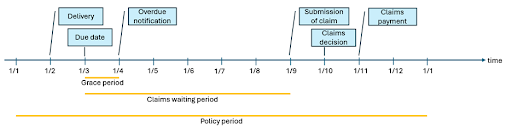

Every claim in trade credit insurance follows a set sequence of events. Understanding these steps helps the policyholder know when to act and shows how the insurer will respond.

The process begins with the delivery of goods or services and the issue of an invoice with a due date. If payment is not made by that date, the policy allows for a short grace (or overdue) period – often around 30 days – during which cover still applies. If the buyer still has not paid, the policyholder must submit an overdue notification to the insurer.

From this point, the claims waiting period (CWP) starts. This period, typically three to six months from the due date, gives both the policyholder and insurer time to continue to chase payment from the buyer. If the buyer still does not settle, the policyholder may submit a claim once the CWP ends, supported by the required documentation.

The insurer then reviews the claim, makes a claims decision, and, if approved, issues the claims payment within the timeframe set out in the policy (often 30 days after the decision).

The policyholder’s role in a claims situation

From the policyholder’s side, making a claim follows a set of general steps that start when a buyer fails to pay and end when the insurer issues an indemnity. Each step has specific requirements and deadlines that must be met to keep the claim valid. What follows is the claims process from the policyholder’s perspective.

- Identify a non-payment event: The process begins when a buyer either fails to pay on time or becomes insolvent. This is the moment that could give rise to a claim.

- Notify the insurance company: The insurer must be informed within the timeframe set out in the policy. This early notice shows that the policyholder is following the agreed-upon rules.

- Documentation preparation: The credit manager gathers all supporting documents to show that the debt is valid and unpaid. This usually includes contracts, invoices, account statements, and proof of collection efforts such as reminder emails or letters.

- Documentation submission: The formal claim is lodged by sending the completed claim form together with the supporting evidence to the insurer.

- Provide further information: If the insurer asks for clarification or extra documents, the policyholder must respond quickly to keep the process moving.

- Wait for assessment and receive decision: The insurer reviews the claim and makes a decision. The outcome may be an approval for compensation, a rejection, or a request for further clarification.

- Claim payment: If the claim is approved, the insurer pays the indemnity according to the timelines set in the policy.

Throughout, the most important things for the policyholder are timing, accuracy, and clear documentation. A well-prepared claim gives the insurer less reason to delay or dispute payment.

Readers who want to understand how the claims process links with underwriting, limits, and debt recovery can explore the full Trade Credit Insurance Guide for a complete breakdown of the policy lifecycle.