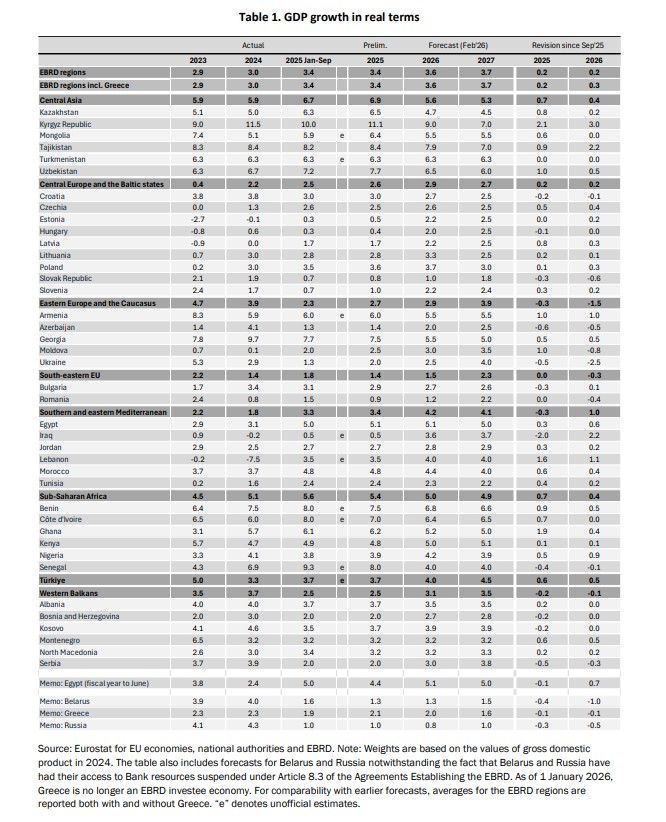

Economic growth in the EBRD regions increased from 2.9% in 2023 and 3.0% in 2024 to 3.4% in 2025. This outcome slightly exceeded earlier projections made before the intensification of trade tensions in April 2025, which had raised concerns about potential disruptions to external demand and supply chains, says the European Bank for Reconstruction and Development (EBRD) Regional Economic Prospects report of February 2026.

The report says that although trade and economic policy uncertainty is high, the negative effects on external demand have been alleviated by quick supply chain adjustments and increased demand for AI-related products. Additionally, the early import of US goods in 2025, anticipating tariff increases, helped reduce the immediate impact of those tariffs.

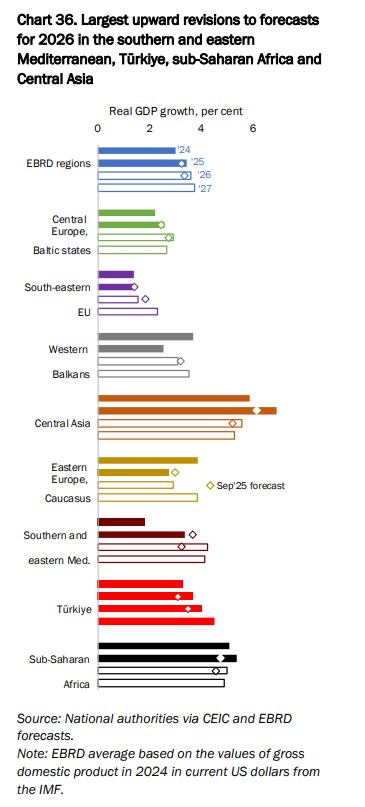

Looking ahead, growth is forecast to strengthen further to 3.6% in 2026 and 3.7% in 2027, representing a 0.2% point upward revision for 2026 compared to the September 2025 forecast. This positive adjustment reflects stronger-than-expected performance in several subregions, including the southern and eastern Mediterranean, Türkiye, Central Asia, sub-Saharan Africa, and parts of central Europe and the Baltic states.

A glance at trade dynamics and supply chain reconfiguration

Trade tensions between China and the United States have led to a significant decrease in trade between the two countries. This is accompanied by a shift in the diversification of trade flows.

The US has increasingly sourced imports from economies within the EBRD regions, especially in product categories such as precious metals, computers, phones, and chocolate. This shift happened as the US reduced its imports from China.

Simultaneously, China’s exports to the EBRD regions have risen, driven by increased production capacity, price competitiveness, and shifting global demand patterns, especially for AI-related goods.

The report says that most EBRD economies now export a more diverse basket of goods than two decades ago, with a growing share of products in which they hold a revealed comparative advantage (RCA).

This diversification improves resilience to external shocks and supports sustainable export growth.

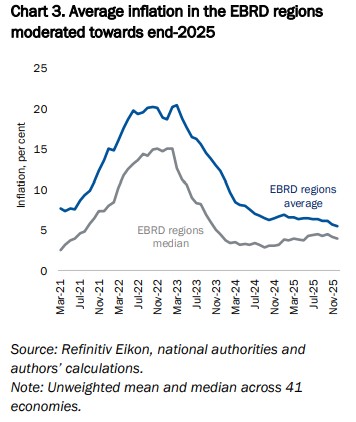

Average inflation eased across the region

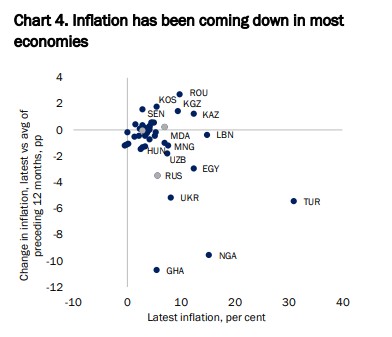

Average inflation across the EBRD regions eased to 5.5% by December 2025, with the median economy experiencing a decline to 4%. This downward trend in inflation was observed in most economies within the region.

After the November 2024 election, the US dollar weakened, causing most currencies in EBRD regions to rise in value against it. Ghana’s currency gained significantly due to higher demand for its cocoa and gold exports and more positive investor sentiment. However, Türkiye’s currency has continued to lose value since April 2025.

Disinflation is expected to continue but at a slower pace than in previous episodes, requiring ongoing monetary tightening and fiscal consolidation to maintain price stability without undermining growth prospects.

Regional economic performance and prospects

Central Europe and the Baltic States

This subregion experienced growth acceleration to an estimated 2.6% in 2025, supported by robust domestic demand and improved export sentiment, particularly from Nordic economies and Germany. The report projects growth to increase to 2.9% in 2026 before moderating slightly to 2.7% in 2027. The region benefits from diversified economies and integration with European supply chains.

Growth in the south-eastern EU slowed from 2.2% in 2023 to 1.4% in both 2024 and 2025. It is projected to remain near this level in 2026, with a downward revision reflecting fiscal consolidation pressures dampening consumption in Romania, before accelerating to 2.3% in 2027.

In the Western Balkans, growth declined from 3.7% in 2024 to an estimated 2.5% in 2025, underperforming expectations mainly due to slower growth in Serbia. The region’s growth is expected to rebound to 3.1% in 2026 and further to 3.5% in 2027, supported by strong domestic demand and significant public investment in infrastructure projects.

Eastern Europe and the Caucasus

Growth in Eastern Europe and the Caucasus slowed from 3.9% in 2024 to an estimated 2.7% in 2025. This change happened as trade with Russia and the inflow of workers and investments into the Caucasus decreased. Ukraine’s economy faced challenges due to major energy and infrastructure damage from the ongoing conflict.

Growth in the region is expected to recover to 2.9% in 2026 and 3.9% in 2027. The 2026 forecast for Ukraine has been revised downward, reflecting the delayed economic benefits of a potential peace agreement.

In this, Türkiye’s economy grew robustly by 3.7% year-on-year in the first nine months of 2025, surpassing expectations. This expansion was fueled by strong private consumption and investment.

Central Asia

Growth in Central Asia increased from 5.9% in 2024 to an estimated 6.9% in 2025. This is better than expected due to stronger consumer spending, high credit growth, robust remittances, and increased investment.

The forecast for 2026 has also improved to 5.6% because of major investment projects, especially in the Kyrgyz Republic and Tajikistan. Growth is expected to slow down to 5.3% in 2027.

Under this geography, Kazakhstan experienced its fastest economic growth since 2011, with a GDP increase of 6.5% in 2025. This growth came from expanding oil fields, higher industrial output, and investments in infrastructure. However, inflation stayed high at 12.3% in December 2025. The fiscal deficit was about 2.5% of GDP.

Sub-Saharan Africa

Sub-Saharan Africa’s growth is expected to rise from 4.5% in 2023 to 5.1% in 2024, and it may reach 5.4% in 2025. This increase is better than what was previously predicted, thanks to higher earnings from commodity exports. Growth is likely to slow a bit to 5.0% in 2026 and 4.9% in 2027.

Southern and Eastern Mediterranean

In 2025, this region experienced strong growth due to the recovery of tourism, less political uncertainty, and good agricultural conditions. The future looks positive, with growth expected at 4.2% in 2026 and 4.1% in 2027, even with ongoing geopolitical risks.

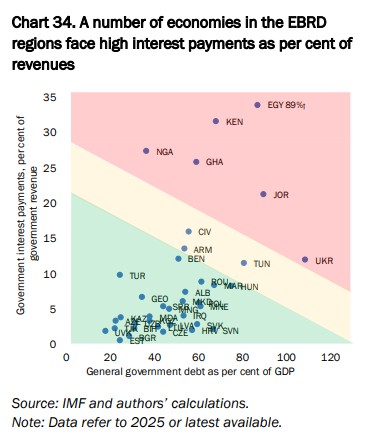

Fiscal challenges and debt sustainability remain a concern

Many EBRD economies are facing challenges with high government debt and significant interest payments, limiting their ability to invest in public services and social programs.

For instance, Egypt’s government interest payments accounted for 89% of revenues in 2025, while Kenya and Nigeria also face substantial debt servicing costs.

These challenges show the need for continued reforms to enhance revenue mobilisation, improve public financial management, and ensure debt sustainability.

The report highlights several risks that could hinder growth, including ongoing geopolitical tensions, escalating trade disputes, persistent inflation, and weaknesses in external demand. Additionally, climate-related shocks and fluctuations in commodity prices threaten economic stability and development.

Policymakers need to be vigilant and adopt flexible policy frameworks to mitigate these risks while supporting inclusive and sustainable growth.

Read the full report here.