Africa’s economic outlook in 2026 is shaped by diverging forces. On one side, a fragmented global environment marked by heightened geopolitical risk, especially due to the conflict in the Middle East, is creating volatility in energy and food markets.

On the other hand, emerging growth corridors driven by the energy transition, improvements in logistics, digital expansion, and increased investment in critical minerals offer new opportunities, states the first edition of the African Economic Compass, published by Mauritius Commercial Bank Limited (MCB) Research, published in April 2026.

Arnaud Levasseur, Executive Vice President, Global Trade Solutions at Mauritius Commercial Bank Limited, said, “Africa’s cross-border trade is accelerating, signalling a continent on the move. By embracing innovation and collaboration, we can transform our systems to match the ambition of Africa’s people, unlocking new opportunities for prosperity and unity with a sustainability lens.”

The report highlights that while a tentative two-week US-Iran ceasefire provides momentary relief, the durability of peace is uncertain.

Impact of the Middle East conflict on Sub-Saharan Africa’s growth

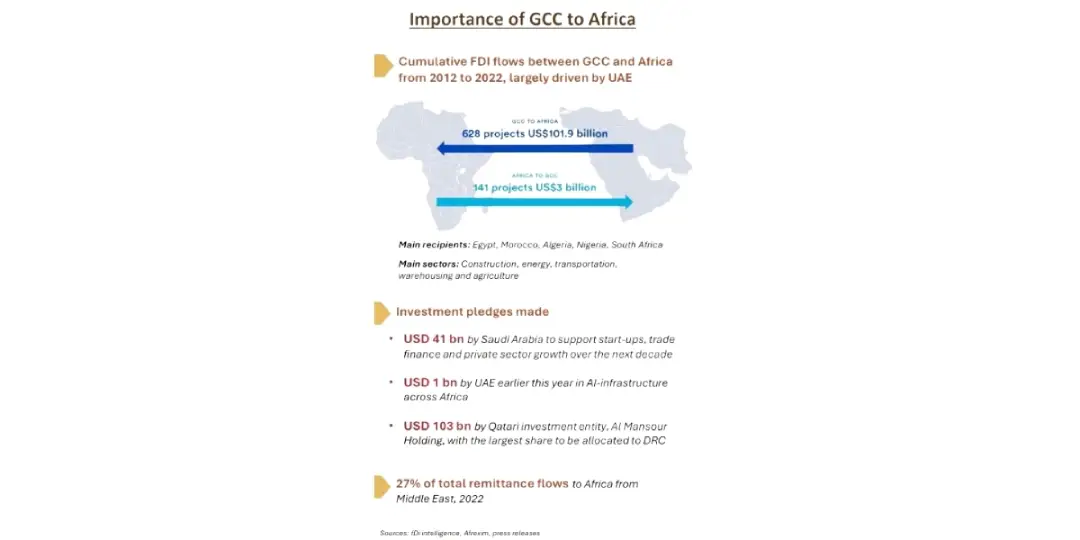

Gulf economies have played a growing role in Africa’s development, supporting infrastructure and energy projects through investment and remittance flows, particularly in North and East Africa.

Before the Middle East conflict began, Sub-Saharan Africa was expected to grow by 4.5% in 2026. This figure was similar to the IMF’s forecast of 4.6% from January 2026, assuming that Brent crude oil prices would average between $60 and $62 per barrel. However, now it has reached the estimation to be around 3.4% (protracted) to 4% (moderate) as a post-war scenario.

“Africa’s macroeconomic fundamentals are stronger than in the past, but its resilience is now being tested by the fallout from the Middle East conflict,” said Vicky Hurynag, Head of Strategy, Research and Development at the Mauritius Commercial Bank Limited.

The escalation has led to a significant external shock, driven primarily by higher, more volatile energy prices and tighter global financial conditions.

The conflict raises risks of delays or reprioritisation of Gulf-backed investments and weaker remittances, which could dampen consumption in countries with strong financial ties to the region, such as Egypt and Kenya.

Inflationary pressures are on the rise, with tanker freight rates and insurance costs rising sharply due to increased war-risk premia for vessels transiting the Persian Gulf. Fertiliser prices are also climbing amid supply disruptions in the Strait of Hormuz, which handles about one-third of global seaborne fertiliser trade.

This is likely to increase agricultural input costs, especially in East African economies like Tanzania, Kenya, and Mozambique, which rely heavily on fertiliser imports from the Gulf region.

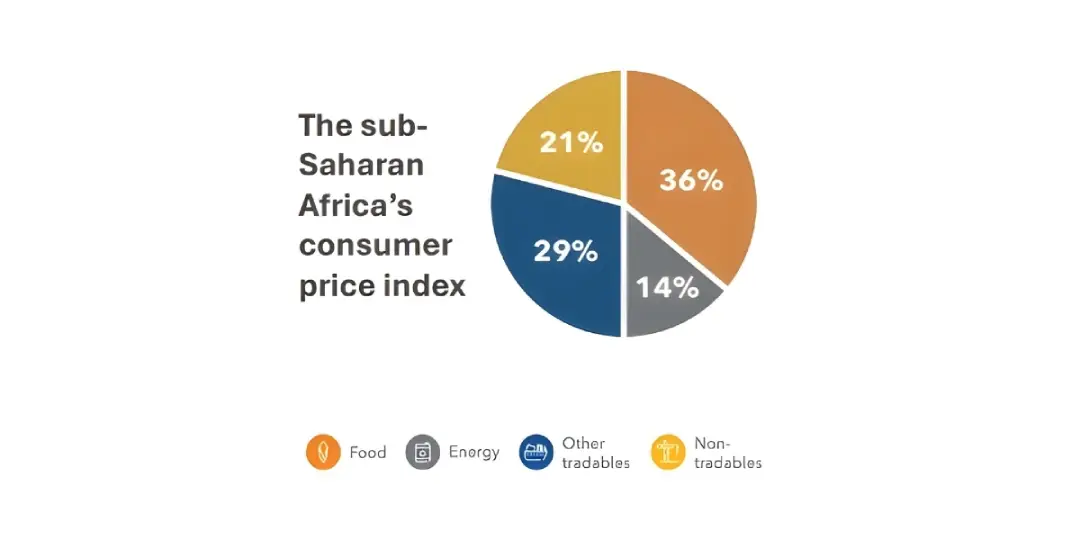

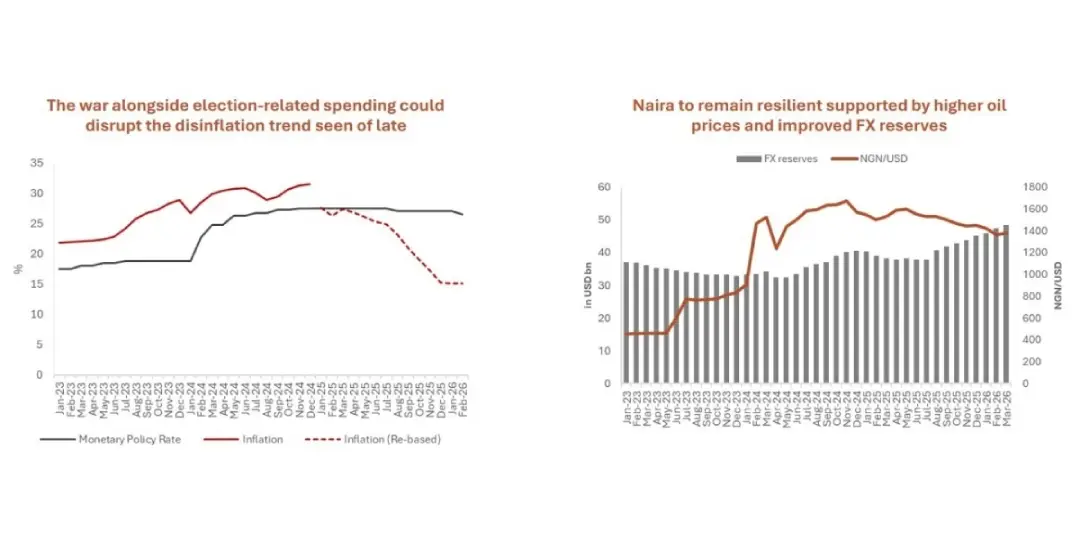

Given that food and energy constitute roughly half of the consumer price index basket in Sub-Saharan Africa, the region is particularly vulnerable to inflationary shocks. This could slow or reverse the recent disinflation trend and compel central banks to adopt a more cautious approach to monetary easing. Should the conflict persist, central banks may face the difficult task of balancing inflation control with growth support, potentially necessitating interest rate hikes to prevent inflation from becoming entrenched.

Commodity prices and the race for critical minerals

Rising commodity prices and demand for critical minerals create varied opportunities across Africa. Elevated oil prices benefit exporters like Nigeria, while Angola’s gains remain limited due to subdued production. The Dangote refinery has become an important supplier for the region, as it meets the growing demand in Africa.

Gold prices started 2026 strong but have recently fallen due to conflicts and a stronger US dollar.

Prices are expected to gradually rise to between $5,500 and $6,000 per ounce by the end of the year. This increase will help boost export earnings for Ghana, South Africa, and Tanzania. South Africa retains more value through refining gold. Ghana primarily exports artisanal gold, while Tanzania is growing its refining capabilities but still exports mostly unrefined gold.

Copper prices are stable between $12,000 and $12,800 per tonne. This stability comes from limited supply and strong demand, especially from electrification and renewable energy projects.

The Democratic Republic of the Congo (DRC) produces about 3 million tonnes of copper each year, while Zambia plans to triple its production by 2031.

Price increases will depend on improving mining infrastructure, increasing production, and enhancing local processing to keep more value within the country.

Inflation and monetary policy: Pressures and prospects

Before the recent regional tensions, Egypt was on a path of easing inflation. This allowed the Central Bank of Egypt (CBE) to start lowering interest rates gradually.

In February 2026, the CBE cut the policy rate by 1% to 19%, with plans to lower it further to 15% by the end of the year.

However, the surge in global energy prices and currency depreciation has reversed this trajectory. Domestic fuel prices increased by 14-17%, feeding through to inflation and prompting the CBE to adopt a more cautious stance on further easing.

The policy rate is now likely to be around 23.5% by year-end. It shows upside inflation risks and increased fiscal spending ahead of the 2027 elections.

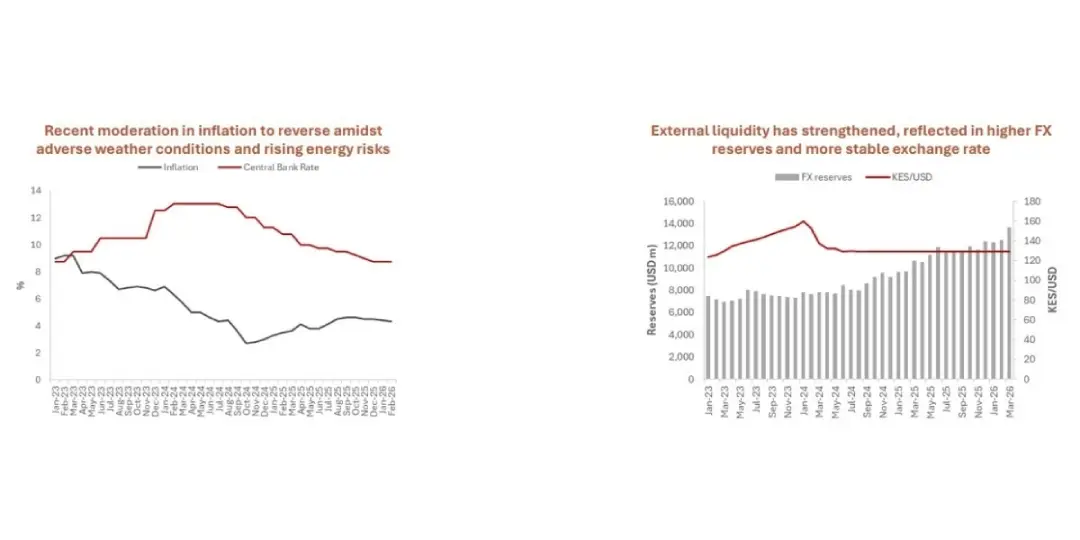

Kenya’s inflation had moderated in 2025 but is now facing renewed pressures from energy shocks and adverse weather events. Severe flooding around Nairobi has disrupted transport and logistics, adding to inflationary and growth challenges.

The Central Bank of Kenya (CBK) has taken a cautious approach. In 2026, it reduced interest rates by just 25 basis points once. Headline inflation is expected to be slightly above the midpoint of the target range, which is 5% ± 2.5%.

The Kenyan shilling has traded in a relatively narrow band around KES 129/USD, supported by improved current account positions and remittance inflows.

Nigeria’s inflation outlook is influenced by rising global oil prices and domestic policy reforms. The economy is transitioning towards macroeconomic stabilisation following exchange rate liberalisation, fuel subsidy removal, and tighter monetary policy under President Tinubu.

Higher oil prices, now assumed at $80-85 per barrel, support export revenues, while the Dangote refinery’s ramp-up reduces reliance on imported fuels, easing foreign exchange pressures.

However, inflation is still a problem, as interest payments take up more than 30% of government revenue, limiting what the government can spend.

Currency trends and external balances

Currency trends across the continent show vulnerabilities amid external shocks.

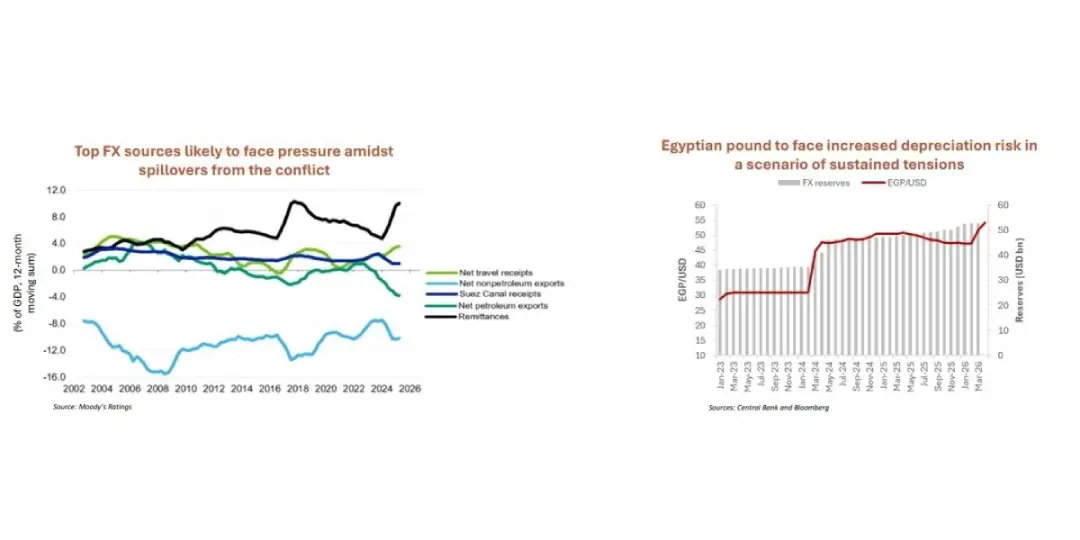

The Egyptian pound weakened beyond 50 pounds per US dollar following the onset of the Middle East conflict, with portfolio outflows estimated at approximately $7 billion. While some recovery is possible, the currency remains susceptible to further depreciation if the conflict persists.

The Kenyan shilling has remained stable, trading around 129 shillings for each US dollar. This stability comes from diaspora remittances and foreign participation in local bonds. However, there is a downside threat due to a change in energy supply and recent flooding.

The Nigerian naira’s resilience is bolstered by improved foreign exchange liquidity and exchange rate reforms, with portfolio inflows gradually returning, though pressures persist from a strengthening US dollar and domestic inflation.

Fiscal conditions and debt sustainability

Fiscal conditions remain a critical challenge, with elevated debt servicing costs limiting policy space.

Egypt’s debt-to-GDP ratio is over 80%. However, the bigger issue is how affordable the debt is. Interest-to-revenue ratios are estimated at 60% to 70%, which shows that revenue is low and interest rates are high. The government has a limited scope for monetary easing, with higher servicing costs.

Kenya has increased liquidity and eased rollover pressures by refinancing Eurobonds and benefiting from strong remittance flows. In January 2026, Moody’s upgraded Kenya’s sovereign rating to B3, indicating a lower risk of default.

However, about 60% of Kenya’s fuel comes from the Middle East. This reliance can lead to supply problems and increased costs for consumers.

Nigeria’s fiscal dynamics are shaped by a structurally narrow revenue base, with interest payments consuming over 30% of government revenue.

The 2026 budget focuses on boosting non-oil revenue with measures like raised capital gains taxes and a minimum effective tax rate for multinationals.

Effective execution of these reforms would be crucial for improving fiscal buffers.

External imbalances and foreign currency inflows

Disruptions to important foreign currency sources, particularly from the Suez Canal and tourism, have increased external risks. Traffic through the Suez Canal has dropped by about 50% since the conflict started, and further disruptions are likely to keep income levels low.

While the SUMED pipeline provides some relief, its capacity of 2.5 to 2.8 million barrels per day is inadequate to compensate for the reduction in canal revenues.

While tourism increased by about 21% in 2025, regional tensions could negatively impact travel due to advisories and limited air connectivity.

Also, remittances remain the most stable source of foreign currency, rising by 40.5% year-on-year in 2025. However, their outlook is closely tied to economic conditions in Gulf economies, where many African expatriates are employed.

Overall, Africa faces short-term challenges, but its long-term growth is supported by significant structural changes.

Access the report here.