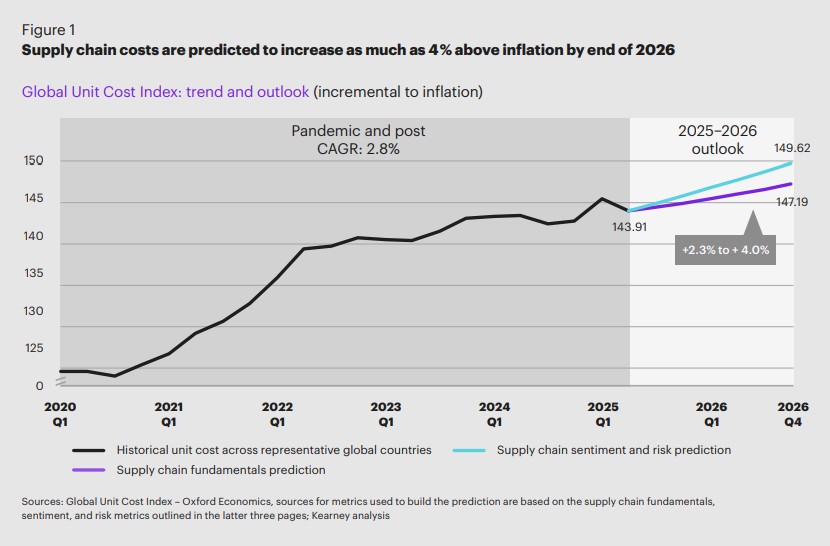

Global supply chain costs will increase between 2.3% and 4.0% above baseline inflation by the end of 2026, despite a moderation in container shipping rates and selected commodity prices, says the Kearney Supply Chain Institute’s Supply Chain Navigator 2026 H1 Briefing.

This forecast challenges the prevailing narrative of broad cost normalisation, highlighting a rising structural cost floor that traditional cyclical indicators fail to capture.

According to the briefing, the Global Unit Cost Index illustrates this trend clearly. The index tracks incremental supply chain costs relative to inflation across representative countries, including China, India, the United States, Germany, and Mexico.

From early 2020 through 2025, unit costs steadily increased, with a compound annual growth rate (CAGR) of 2.8% during the pandemic and post-pandemic period. The forecast for Q4 2026 shows a further increase, driven by persistent structural factors rather than temporary disruptions.

This sustained cost inflation reflects the embedding of new cost layers across supply chains, signalling a fundamental shift in the cost baseline that enterprises must recognise and manage proactively.

Structural drivers of persistent cost inflation

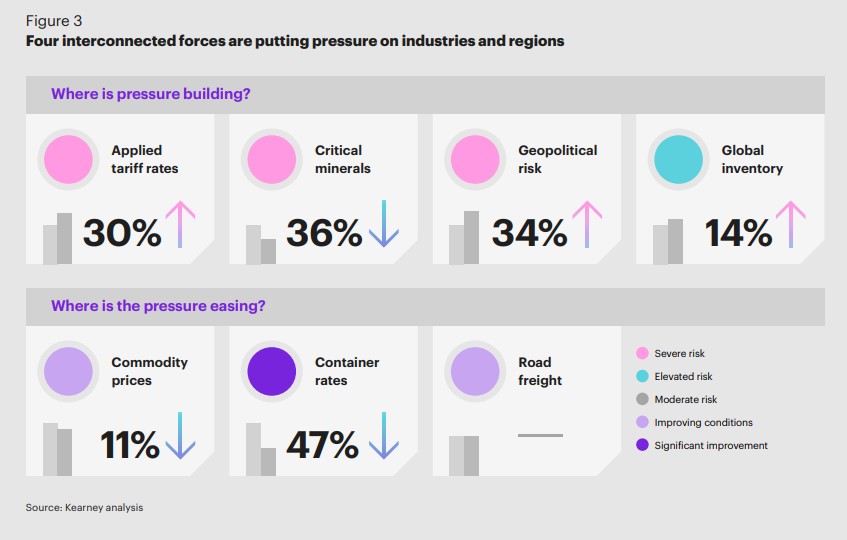

Geopolitical tensions and changing trade policies are disrupting global trade. New tariffs, sanctions, and regulations increase business costs. Ongoing tensions raise operational and compliance expenses, making supply chains more expensive.

Constraints in critical minerals for the manufacturing and technology sectors further exacerbate input cost inflation and supply risks. Minerals found in geopolitically sensitive regions make sourcing them more complicated and unpredictable.

Also, inventory levels are high in total, even though they have returned to typical levels compared to sales. This ties up capital and increases carrying costs, reflecting cautious inventory buildup as firms hedge against ongoing uncertainty.

The tight labour market and problems in transportation and warehousing lead to higher wages and delays in operations. These challenges are magnified by overall inflation, unionisation efforts, and policy changes, which all contribute to rising manufacturing labour costs.

Container shipping rates rose sharply during the pandemic but have since dropped significantly. This decline is due to reduced demand from tariffs, too much capacity, and less port congestion. In contrast, truckload rates have stabilised, with regional differences affected by export cycles and seasonal increases, which keep logistics costs high.

The risks of complexity and uncertainty

Supply chain risks have become more complex. Traditional issues such as natural disasters and supplier failures are now joined by geopolitical tensions, trade policy changes, sanctions, and technological disruptions. Current risk models often overlook this complexity, putting organisations at risk of unexpected shocks.

Trade fragmentation from tariffs, sanctions, and regulations pushes companies to reevaluate their sourcing and distribution strategies.

Businesses need to manage risks while keeping costs low and maintaining good service. To do this, they need to improve their understanding of situations, integrate real-time data, and be flexible in their operations.

Strategic shift in patterns shaping operational performance

The operational performance in today’s supply chains is being fundamentally reshaped by three interrelated patterns.

The first is persistent cost inflation driven by geopolitical tensions, resource constraints, and labour market pressures. This increases operational costs beyond standard inflation rates. This ongoing cost pressure requires improved cost management and strategic sourcing.

Second, increased volatility and uncertainty have become the norm. Supply chains are frequently disrupted by changing trade patterns, regulatory shifts, and unpredictable customer demands. This constant change means organisations need to shift from simply responding to problems to actively managing them.

Third, accelerated digital transformation and ecosystem collaboration are critical enablers of operational agility. Advanced analytics, real-time data integration, and cross-organisational partnerships empower companies to sense risks early, optimise resource allocation, and coordinate responses across complex networks.

These trends make it necessary to shift towards managing supply chains in a more dynamic, data-driven, and collaborative way.

External environment, supply chain fundamentals, and sentiment outlook

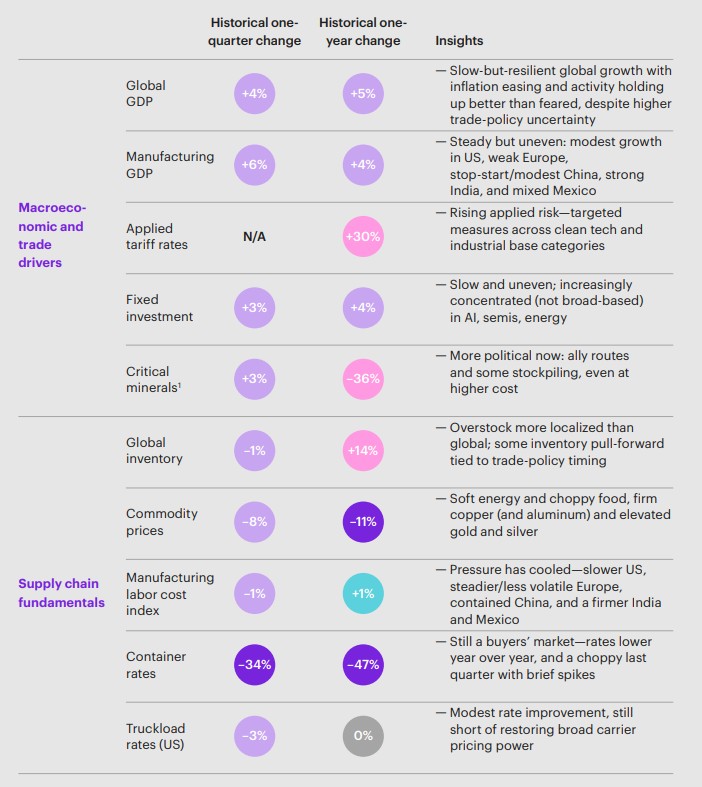

Kearney’s analysis shows that global supply chains are under pressure, even as some signs of stabilisation appear. Global GDP growth is slow but stable at 5% year-on-year, with manufacturing GDP rising slightly by 4%. However, applied tariff rates have jumped by 30%, driven by ongoing trade tensions that are increasing costs in targeted industries.

Fixed investment rose slightly by 4%, yet remains uneven and concentrated in select regions such as India, semiconductors, and energy sectors. Exports of critical minerals fell significantly by 36%, highlighting geopolitical risks and supply shortages in essential raw materials.

Global inventory levels dropped by 14%, showing some normalisation, but there are still areas of overstock due to trade policy timing. Commodity prices fell 11% year-on-year, primarily because of weaker energy and food markets, while precious metals like gold and silver remain high due to geopolitical uncertainty.

Manufacturing labour costs increased marginally by 1%, reflecting inflation and policy-driven wage pressures, while container shipping rates dropped dramatically by 47%, signalling a buyer’s market with excess capacity. Truckload rates in the US showed no significant change, indicating a modest stabilisation in road freight costs.

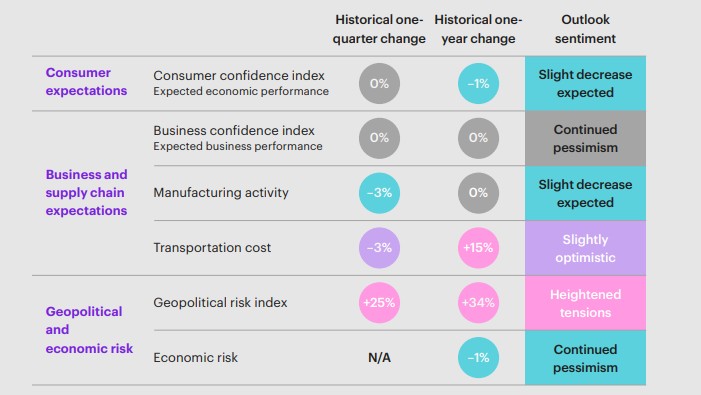

Sentiment and risk outlook remain cautious. Consumer confidence and manufacturing activity have dipped, indicating weak growth expectations. Business confidence is pessimistic, although transportation cost sentiment is slightly optimistic due to lower shipping rates. Geopolitical risk has increased by 34% compared to last year, indicating ongoing uncertainty in supply chain decisions.

These data points reveal a supply chain impacted by cost pressures, uneven recovery, and high uncertainty. Firms must navigate rising tariffs, volatile commodity markets, and geopolitical tensions while managing inventory and labour costs in a landscape where traditional stability has given way to persistent volatility.

Read the full report here.