By: Gabrielle Ried, PANGEA-RISK

Africa possesses some of the world’s largest oil, gas, and renewable energy resources, yet remains highly vulnerable to external energy shocks. As the 2026 Gulf War exposed the risks of import dependence, a new wave of refinery developments, renewable energy investments, and regional integration initiatives is reshaping the continent’s energy landscape. By enhancing domestic refining, diversification, and integration, Africa is increasingly leveraging energy security, infrastructure investment, and intra-African trade to reduce vulnerability, accelerate industrialisation, and unlock long-term economic growth.

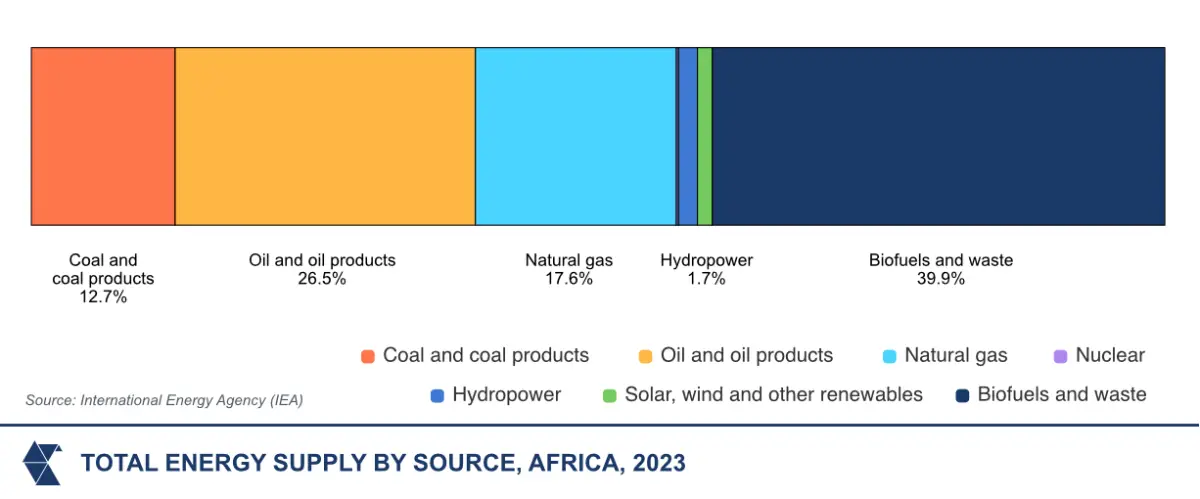

Africa holds approximately 125 billion barrels of proven oil reserves, vast natural gas deposits, and some of the world’s most abundant solar and hydropower resources. Yet, it remains among the most energy-insecure regions globally. Decades of underinvestment in downstream infrastructure, including refineries, power grids, pipelines, and storage, have left African economies reliant on imported energy supplies. The result is a continent that drives energy systems for other regions while its own economies endure fuel price volatility, power outages, and a persistent hurdle to industrialisation.

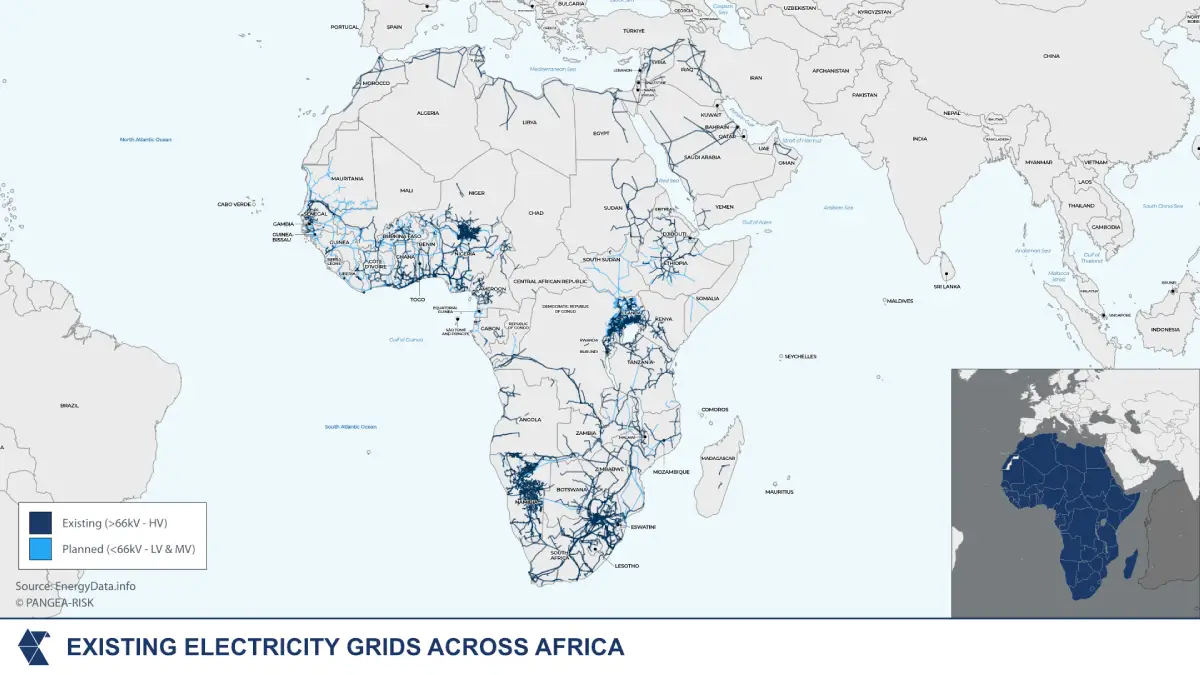

More than 600 million people across sub-Saharan Africa lack access to reliable electricity. The International Energy Agency projects that Africa’s electricity demand will have increased by approximately 75 per cent between 2020 and 2030, growing from 680 terawatt-hours to 1,180 terawatt-hours, even as investment in generation and distribution lags critically behind. The 2026 Gulf War, the commissioning of major new refinery projects across Africa, and a global shift in energy policy from energy transition to energy security have fundamentally altered the continent’s energy landscape. Together, these developments have created both an urgent need and a unique opportunity for African states to take greater control of their own energy futures.

PANGEA-RISK assesses that the countries that act now to build domestic refining capacity, forge intra-African energy supply chains, and scale renewable generation will be positioned to capture the industrial dividends of cheaper, reliable energy. Those that do not will remain structurally exposed to geopolitical shocks beyond their control as the events of early 2026 have shown.

The Gulf War and Africa’s energy vulnerability

The conflict between the United States (US), Israel, and Iran in early 2026 sent immediate shockwaves through global oil markets. Attacks on energy infrastructure and disruptions to shipping in the wider region, particularly through the Strait of Hormuz, which carries approximately 20 per cent of global oil and liquefied natural gas trade, generated sharp price spikes of over USD 100 per barrel and acute supply uncertainty. At the same time, the Gulf War and its impact on global energy prices reiterated the vulnerability of high energy imports for many African states. As Kenyan President William Ruto stated during the Nairobi Business Summit in April 2026, “We do not want to be held hostage any more by the Strait of Hormuz. We do not want to be held hostage by wars that are started by other people. We have our resources here, and we are saying we are going to use our African resources to industrialise our region.”

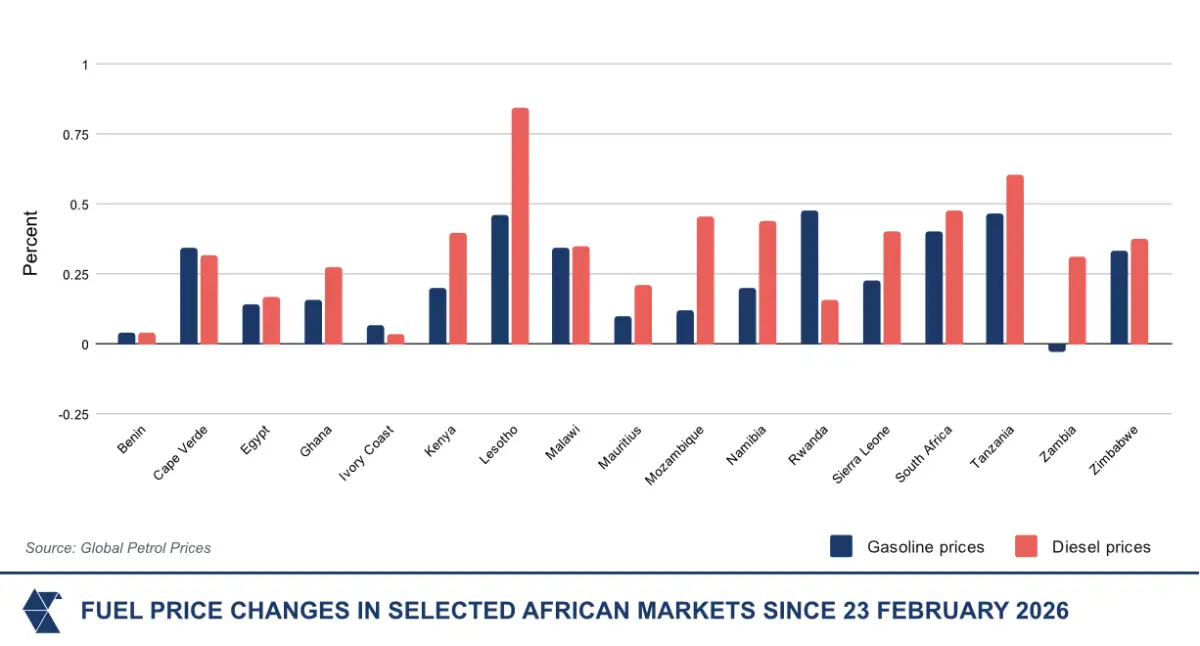

For African economies, the consequences run deeper than a price hike at the pump. Countries including Ethiopia, Ghana, Kenya, Senegal, and South Africa import significant volumes of refined petroleum products, exposing their economies to fuel price volatility that directly increases electricity generation costs, squeezes government subsidy budgets, and raises consumer prices across the supply chain. Fuel price hikes were reported in Nigeria and Uganda within weeks of Gulf escalation, while authorities in Ghana, Kenya, and South Africa have issued warnings of further increases despite a fragile ceasefire between the US and Iran as global oil supplies continue to recalibrate.

This energy vulnerability is not insulated to the oil and gas sector, and the renewable energy sector also faces challenges. Despite its large renewable energy potential, Africa is heavily dependent on imports of renewable energy inputs such as solar panels, batteries, and inverters, which are largely manufactured in Asia and shipped through routes including the Red Sea, the Suez Canal, and the Bab el-Mandeb Strait. Recent shipping disruptions and vessel rerouting around the Cape of Good Hope have extended freight times and increased insurance premiums, raising capital costs for African clean energy projects. These delays underscore that Africa’s energy vulnerability extends beyond production and generation, affecting the entire energy value chain.

Breaking Africa’s imported energy reliance

For decades, Africa’s postcolonial ambitions to develop a domestic downstream energy sector were blighted by underinvestment, political interference, and the perverse economics of small-scale refineries competing against larger, more efficient facilities in the Middle East and elsewhere. The continent’s refineries operated below global average utilisation rates. Many became liabilities rather than assets, surviving only through government subsidies that distorted markets without achieving energy security. Without scale, refineries could not be profitable, and maintenance and utilisation waned.

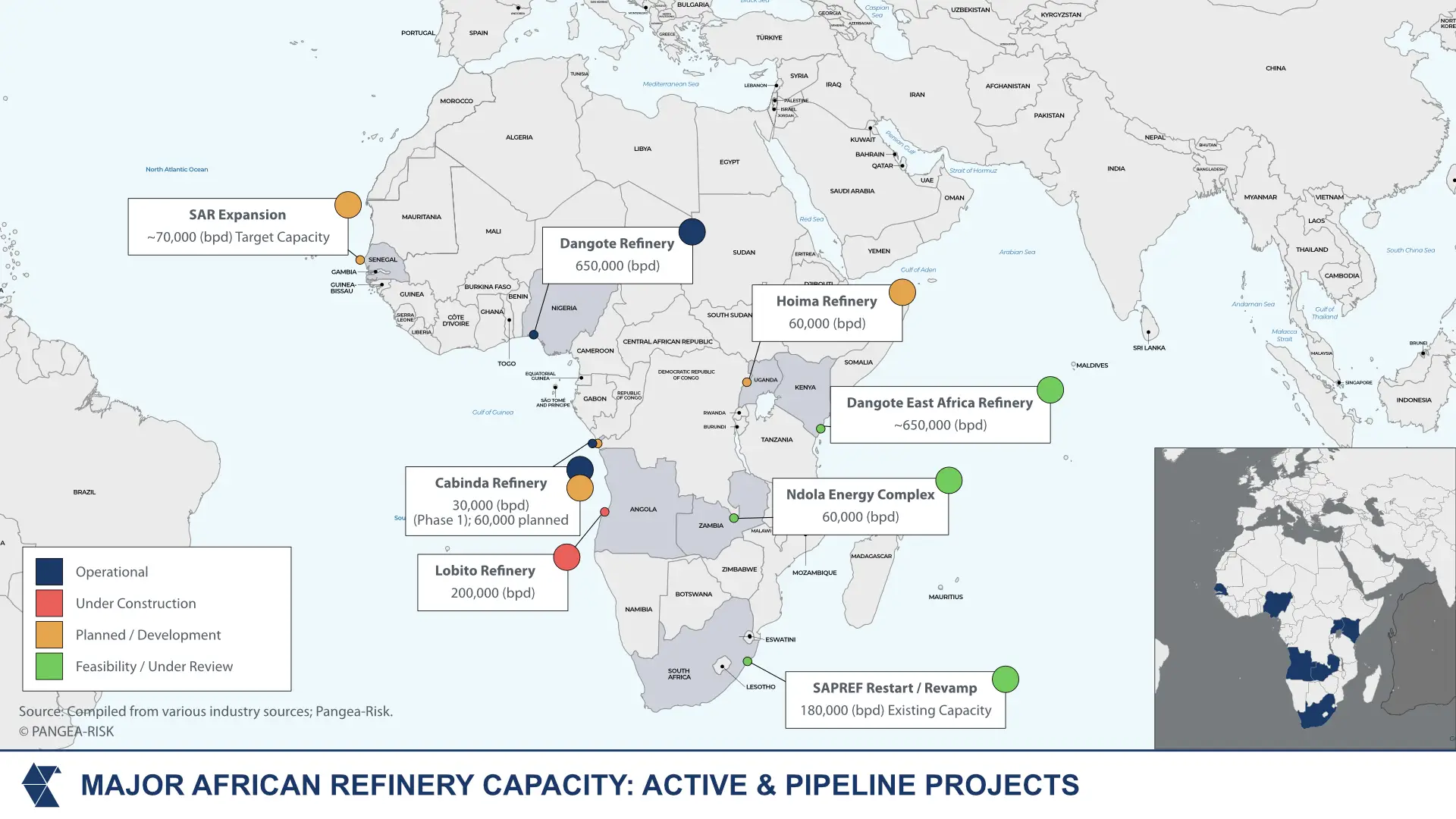

Today, that picture is changing materially. A wave of new capacity, led by landmark projects in Nigeria and Angola, with significant developments in Zambia, Senegal, Uganda, Ghana, and the Republic of Congo, is reorienting the continent’s downstream energy landscape. The critical shift is one of scale and intent, comprising strategic national and regional infrastructure investments designed to capture value from Africa’s own hydrocarbon resources and reduce exposure to import markets.

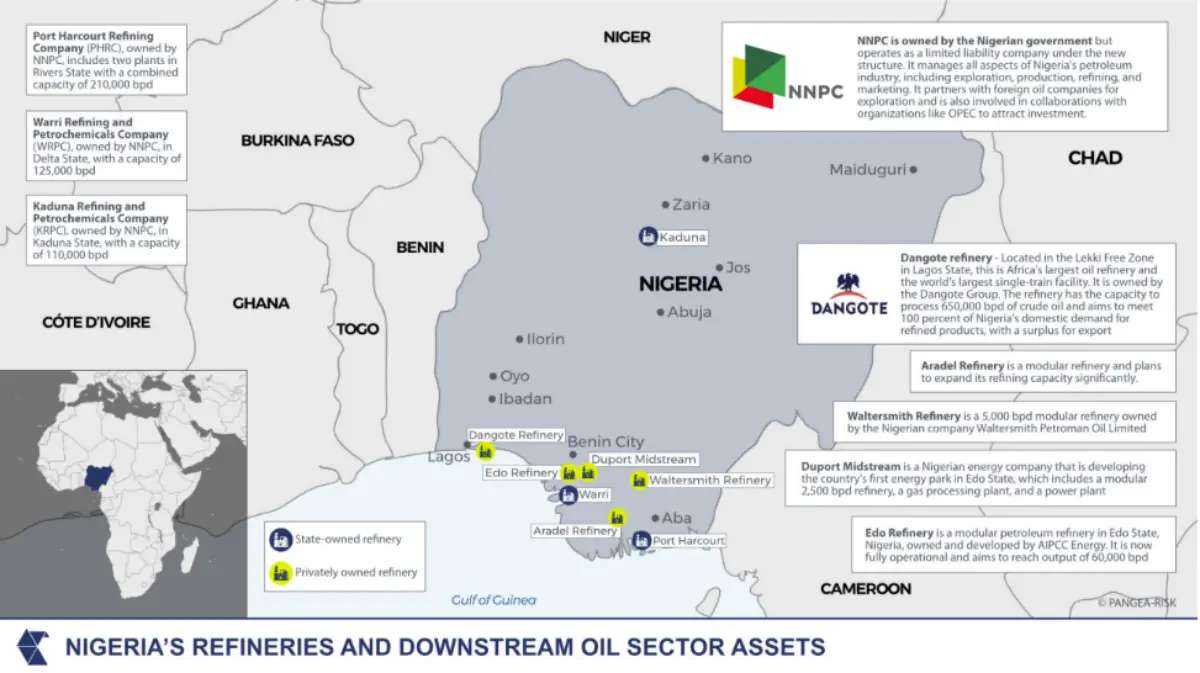

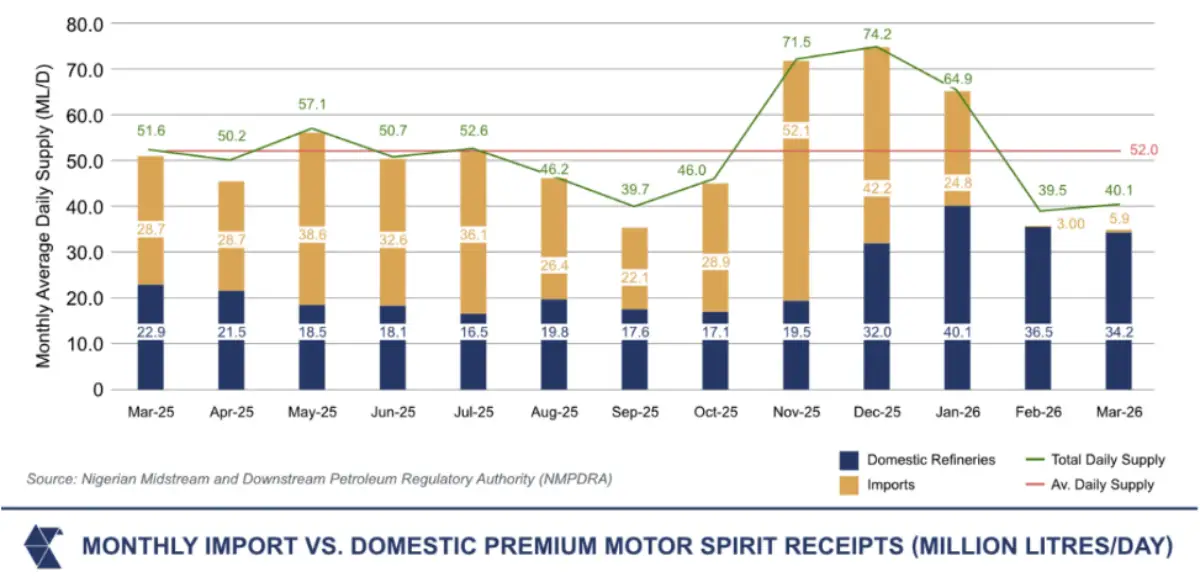

The Dangote Petroleum Refinery in Lagos, Nigeria, now operational at 650,000 barrels per day and among the largest single-train refineries in the world, represents among the largest downstream investments in Africa’s history. The refinery was designed from inception to reshape the regional fuel market. With sufficient capacity to satisfy Nigeria and export across West Africa and beyond, Dangote has already begun driving down regional fuel prices and reducing the foreign exchange drain associated with Nigeria’s historically paradoxical reliance on imported petroleum products. Nigeria’s midstream regulator reported that by late 2025, the refinery was supplying approximately 18 million litres of petrol per day on average, with a declared target of 50 million litres daily.

The Dangote model is now being replicated eastward. In April 2026, Kenya’s President William Ruto announced, alongside Aliko Dangote, that East African countries were exploring the development of a regional oil refinery to strengthen energy security and reduce fuel import dependence. Dangote has since expressed support for locating the proposed refinery in Mombasa, citing its superior port infrastructure, established fuel distribution networks, and larger regional market compared to, for example, Tanzania’s Tanga. A feasibility study is currently assessing potential sites, including Mombasa, Lamu, and Tanga, with the project’s viability expected to depend on government support, financing arrangements, and regional market integration.

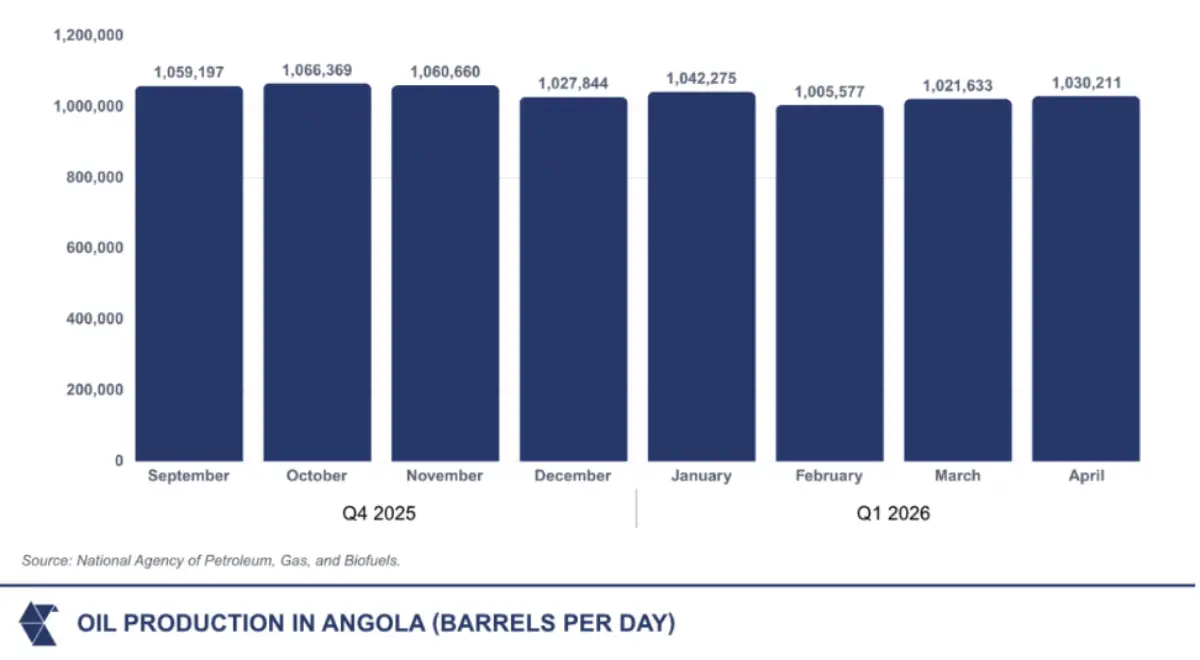

Angola’s refining ambitions also extend beyond domestic supply. The country’s strategy is explicitly regional, positioning Angola as an energy hub for Central and Southern Africa by leveraging the Lobito corridor, which connects the Democratic Republic of Congo and Zambia to Angola’s Atlantic coastline. The separate and government-backed 200,000-barrel-per-day Lobito Refinery is designed to process approximately half of Angola’s 440,000-barrel-per-day daily consumption while generating a significant export surplus. Angola’s existing Luanda refinery produces 65,000 barrels per day; the new facility would transform Angola’s refining capacity and export reach entirely.

Angola’s Cabinda refinery, backed by UK-based Gemcorp Capital, began supplying domestic and foreign markets in early 2026. With initial capacity of 30,000 barrels per day and plans to double by the end of 2026, it represents a first tangible step toward the broader Lobito vision.

Ending energy poverty

The strategic case for building Africa’s domestic energy capacity is inseparable from the development imperative. The IEA estimates that Africa holds more people in energy poverty than any other continent. When the measure is extended beyond basic access to reliable electricity, defined as no more than a few outages per month, the true scale of the deficit becomes even starker. The inability to access affordable, reliable power is an economic constraint that fundamentally limits manufacturing, services, agriculture, and ultimately the tax revenues that fund public goods and services. Energy security in Africa is therefore increasingly a dual challenge linked to securing hydrocarbon products for transport and industry while simultaneously expanding domestic generation to meet rising electricity demand.

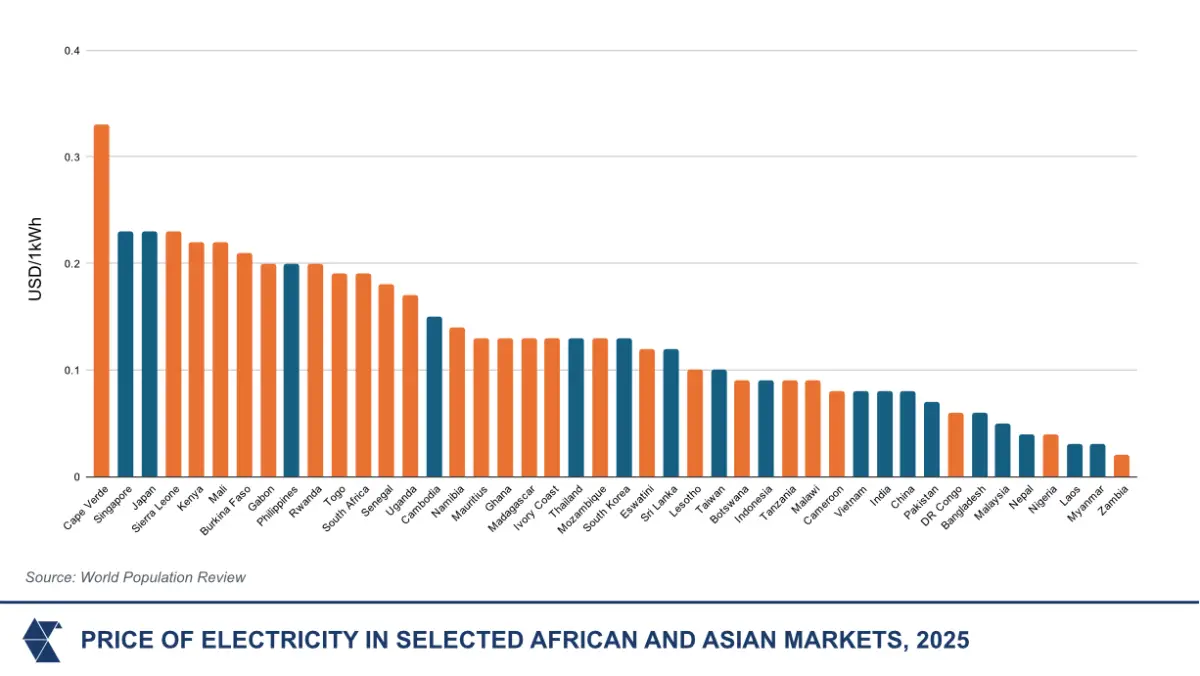

Africa’s manufacturing value added remains around 10 per cent of GDP, according to the World Bank, compared with a global average of roughly 17 per cent. High electricity costs and unreliable power supply are among the most significant factors constraining industrial competitiveness. Industrial power tariffs in many sub-Saharan African markets are substantially higher than those in leading manufacturing economies in Southeast Asia, increasing production costs for energy-intensive industries such as cement, steel, chemicals, and food processing. Lower fuel and energy costs can reduce transport expenses, factory operating costs, and ultimately consumer prices, improving the competitiveness of domestic manufacturing and regional value chains.

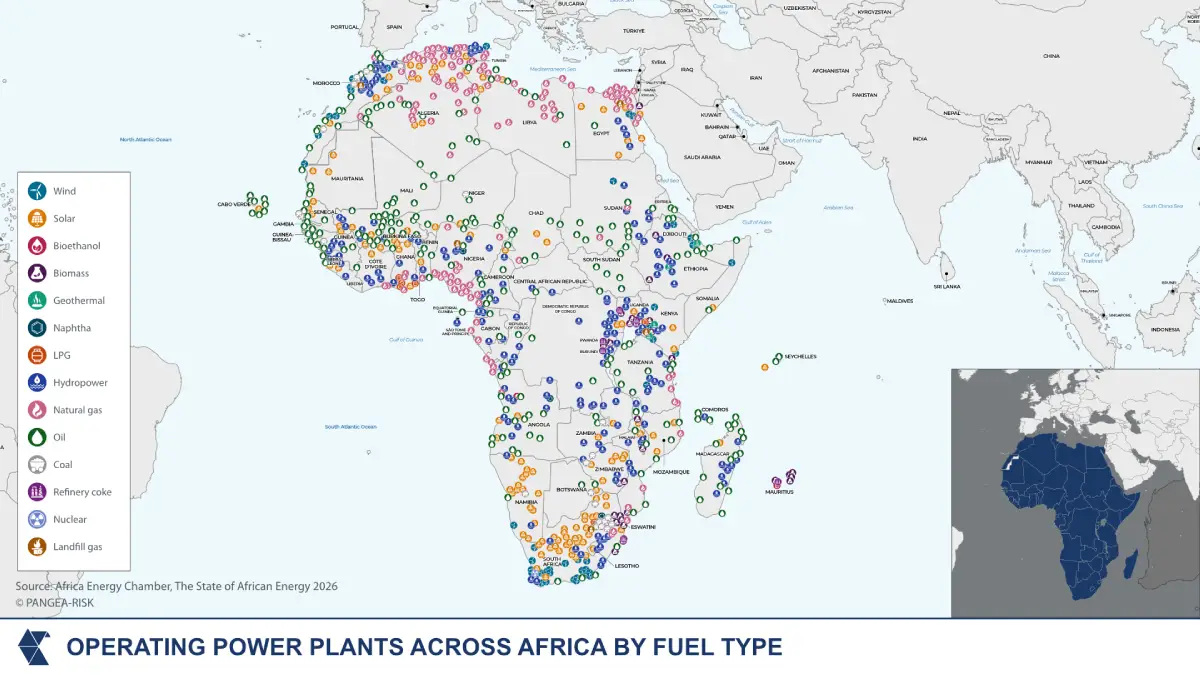

The African Development Bank has estimated that the continent faces an annual financing gap of USD 400 billion if it is to achieve the Sustainable Development Goals by 2030, a figure that dwarfs current investment flows. Less than 2 per cent of global renewable energy investment flows to Africa, despite the continent possessing some of the world’s richest solar, wind, and hydropower resources. The Sahel sub-region alone, with its high solar irradiance, has the potential to become a global leader in solar energy production. The African Development Bank’s Desert to Power Programme aims to harness solar energy to electrify 250 million people by 2030, with Mauritania, Senegal, and Mali among the early-mover countries, but more will be required to unlock Africa’s solar opportunities.

Intra-African Energy Trade: AfCFTA’s untapped potential

Africa’s energy security challenge is, in large part, a connectivity and trade challenge. Oil and gas pipelines on the continent have historically been oriented toward export rather than connecting areas of production to areas of domestic demand. In addition, intra-African trade in energy products remains a fraction of what the continent’s resources could support.

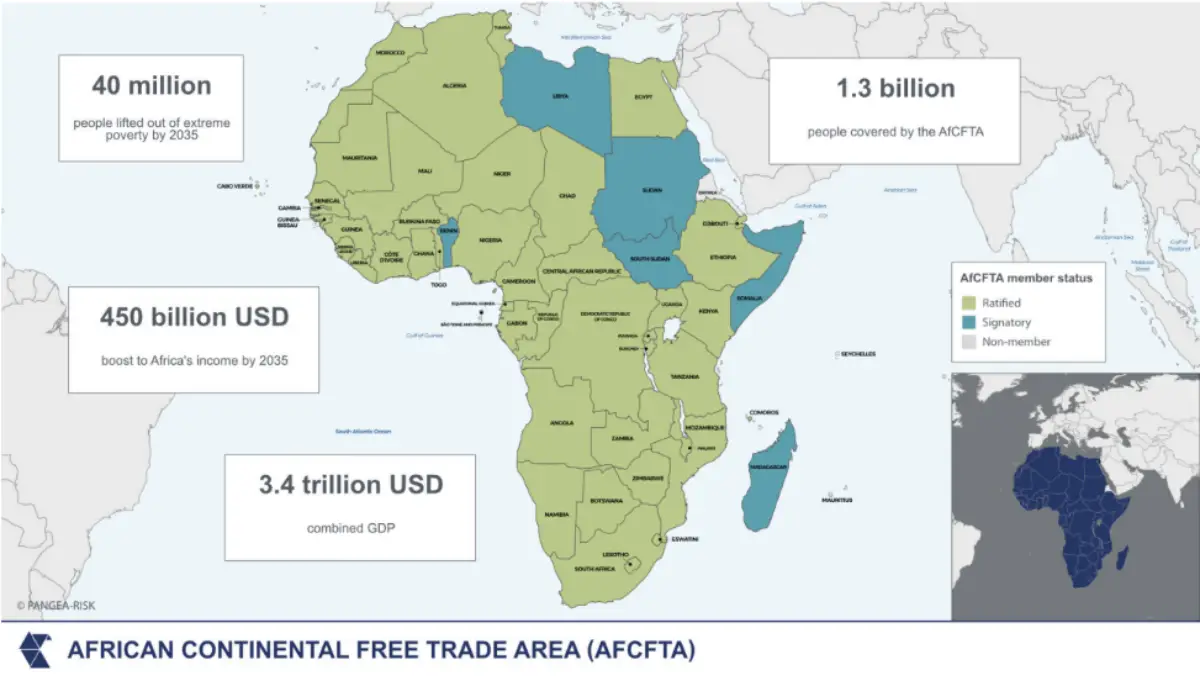

The African Continental Free Trade Area, now with 54 member states committed to removing trade barriers across goods and services, provides the institutional framework to change this dynamic. Under AfCFTA, Algeria’s refined petroleum products could more easily reach markets such as Chad, while Angola’s growing refining capacity could serve Zambia and Botswana under a more integrated continental trade framework. Similarly, a proposed East African refinery backed by Dangote could potentially supply Uganda, Rwanda, South Sudan, and the DRC, benefiting from reduced tariff and non-tariff barriers compared with the current patchwork of bilateral arrangements. The Africa Energy Bank, which is targeting USD 5 billion in initial capitalisation, is expected to finance upstream, midstream and downstream energy infrastructure across the continent. By supporting projects such as pipelines, storage facilities, refinery upgrades and distribution networks, the bank could help lower the transport and logistics costs that currently constrain the competitiveness of African refiners and fuel markets.

Kenya has revived discussions over extending fuel pipeline connections into Uganda and Rwanda through the proposed Eldoret–Kampala–Kigali products pipeline. Zambia and Angola are advancing plans for a refined products pipeline linking Lobito and Lusaka. In East Africa, the Kenya–Ethiopia Electricity Highway already enables Kenya to import Ethiopian hydropower, providing a model of cross-border energy integration that could be replicated across Africa’s power pools. Elsewhere in Central Africa, discussions have emerged around extending regional petroleum transport infrastructure into neighbouring markets, including the DRC, although no final investment decisions have been taken.

Insight

From Nigeria’s Dangote refinery and Angola’s Cabinda facility to emerging projects in East Africa and Zambia, the continent is entering a new phase of downstream industrial development that has the potential to reshape regional trade flows, energy security, and industrial competitiveness. New energy corridors, storage infrastructure, pipelines, logistics networks, petrochemical industries, and industrial zones are creating a broader ecosystem of investable opportunities. As governments seek to reduce import dependence and strengthen intra-African trade, strategic infrastructure is increasingly becoming a central pillar of economic policy.

However, success will depend on execution. Refinery utilisation rates, the pace and durability of fuel subsidy reform, and the development of cross-border pipeline infrastructure will be critical determinants of commercial viability. Operational underperformance, regulatory uncertainty, and infrastructure bottlenecks remain material risks that require rigorous assessment at both the national and sub-national levels. The geopolitical disruptions of recent years have reinforced the strategic costs of energy dependence and accelerated political support for domestic refining capacity. For commercial stakeholders, the key challenge is identifying where opportunities outweigh the risks.

Looking ahead, Africa’s energy story will be defined less by resource endowment and more by the ability to convert those resources into secure, affordable, and reliable energy systems. The convergence of geopolitical disruption, expanding refining capacity, and stronger continental trade frameworks has created a rare window for African states to reduce import dependence and build more integrated energy markets. Countries that successfully combine downstream investment with renewable generation, transmission infrastructure, and cross-border trade connectivity will be best positioned to accelerate industrialisation, attract investment, and strengthen economic resilience.