As 2025 winds to a close, we wanted to speculate a little and make a few predictions about what we think the worlds of trade, treasury, and payments can expect in 2026. But we did not want this piece to be based only on our own opinions, so we sent a short survey to our Global Advisory Panel and our trusted experts on what they think will matter most in 2026.

After letting this panel of experts do the hard thinking for us, we settled on this list of 5 predictions for the year ahead. Agree? Disagree? Let’s check back in a year’s time and see how we did!

Until then, here are TTP’s top 5 predictions for 2026.

Prediction 1) Private credit will expand rapidly into trade finance in 2026, filling gaps banks cannot

Our first prediction for 2026 is that private credit will become a more central source of trade and working-capital finance, particularly for mid-market firms and commodity traders that struggle to fit bank balance-sheet constraints. While our survey respondents consistently pointed to tighter counterparty risk, capital treatment pressures, and de-risking by banks, several also highlighted the search for alternative sources of liquidity as a defining feature of the year ahead.

As private credit expands its footprint in trade finance, the challenge quickly shifts from capital availability to how these exposures are originated, verified, and distributed—bringing real-world asset structures and tokenisation into focus.

Marina Goche, CEO of AltDigitize, said, “History will look back at 2026 as the year when] tokenization matured, regulation clarified, institutional adoption accelerated and real world assets meaningfully transitioned onchain.

Andre Casterman, Founder of Casterman Advisory, said, “The dominant trend shaping lending and trade finance in 2026 and beyond will be the continued growth of private credit as a flexible, partnership-driven alternative to traditional bank lending. With global private credit projected to double to $4.5 trillion by 2030, it will unlock untapped revenue opportunities for middle-market traders and commodity firms across the US, EU, and UK. Strategically, this evolution promises to address the trade finance gap that banks and their current partners won’t be able to close.”

This suggests that more trade flows will be financed through non-bank partnerships and hybrid models, especially considering that private credit does not always have the same limits that banks face, which can allow them to offer greater speed and a greater tolerance for complexity. In 2026, the trade finance gap will not close, but we may begin to see it being increasingly bridged from outside the banking system.

Prediction 2) E-bills of lading will be the most adopted digital trade instrument in 2026

Our second prediction for 2026 is that electronic bills of lading (eBLs) will see higher adoption than other digital trade instruments, even as broader paperless trade reform continues to move slowly and unevenly. When asked which reforms or standards will have the greatest impact, the greatest number of respondents selected e-bills of lading (71%), followed by cross-platform interoperability (57%), and artificial-intelligence-driven compliance (43%).

One respondent who preferred to remain anonymous said that 2026 will be a “Pivotal year for the electronic transferable record (ETR) digitalisation journey as financial institutions recognise the value of eBLs as digital security and source of digital data.”

New legal frameworks for electronic trade documents and adoption of the Model Law on Electronic Transferable Records (MLETR) were both repeatedly identified as important, but respondents were less confident that these reforms would translate into broad, end-to-end digitisation within a single year.

According to the International Chamber of Commerce (ICC), today, 61.5% of global exports come from economies aligned with, or committed to MLETR, that’s a remarkable leap from just 34% in 2023.

On aggregate, however, respondents were optimistic for digital trade in 2026, with Merisa Lee Gimpel, Founder and MD of consultancy Digital Trade Works predicting that, “[History will look back at 2026 as the year when] paperless trade finally scaled.”

Prediction 3) Corporate payment terms will lengthen in 2026

Our next prediction for 2026 is that corporate payment terms will lengthen, and “pay later” will become the default working-capital choice for many large buyers. In our survey, eighty-six per cent of respondents identified the most visible shift in corporate behaviour they expect to see next year as longer payment terms to preserve cash.

Forty-three per cent also anticipate an expansion of supplier-finance programmes, which suggests that longer payment terms may increasingly be paired with structured financing to prevent supplier distress.

According to the results of our survey, supplier fragility was the most frequently cited pressure for 2026, ahead of both higher financing costs or payment delays.

Against that backdrop, regulatory attempts to hard-limit payment terms sit uneasily with market reality. International Credit Insurance & Surety Association (ICISA), in its 2025 commentary on EU payment-term policy, emphasised that rigid maximum caps on payment terms, such as a proposed 30-day limit, would remove the ability of buyers and suppliers to “negotiate terms suited to their risk, seasonality and working-capital profiles,” underlining the continued importance of contractual flexibility in payment practices.

In that environment, stretching payables to longer term is the fastest lever available, but can only be used if buyers are able to selectively support their critical suppliers through finance. That balance, rather than headline cost of capital, is what will define payment-term behaviour in 2026.

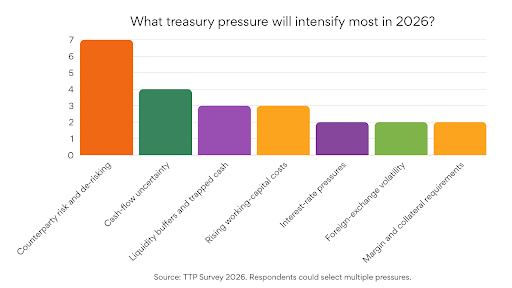

Prediction 4) Counterparty risk will be treasury’s number-one headache in 2026

Our next prediction for 2026 is that counterparty risk will become treasury’s dominant concern, overtaking pure interest-rate moves and funding costs.

In our survey, 57 per cent of respondents identified counterparty risk and de-risking as the pressure most likely to intensify next year, ahead of liquidity buffers, margin requirements, or cash-flow uncertainty. Risk is no longer coming from a single direction, nor is it confined to weaker credits or peripheral markets.

That concern persists even as the interest-rate backdrop stabilises. When asked how the cost of capital would evolve in 2026, two-thirds of respondents expect it to remain broadly unchanged, with only one-third anticipating a moderate increase. In other words, rate volatility is no longer the primary variable shaping treasury behaviour. Instead, attention is shifting to whether counterparties remain bankable, insurable, and operationally reliable in a more fragmented global economy.

This aligns with Deloitte’s 2026 outlook, which points to persistent geopolitical realignment, trade policy uncertainty, and uneven regional growth as structural features of the year ahead, even as inflation eases and monetary policy becomes less restrictive in many major economies. For treasurers, that combination matters: lower or stable funding costs do little to offset the risk of sanctions exposure, trade disruption, weakened suppliers, or sudden withdrawal of insurance and bank appetite.

In that environment, the binding constraint in 2026 will not be how expensive capital is, but whether counterparties can still be trusted across credit, compliance, and continuity dimensions. Treasury risk management is therefore becoming less about optimising cost and more about preserving optionality, resilience, and access in an increasingly selective financial system.

Prediction 5) Supplier fragility will replace high financing costs as the main working-capital stress point for corporates in 2026

Our final prediction for 2026 is that supplier fragility will be a working-capital stress point in 2026. Our survey results show that 43% of respondents picked supplier fragility as the single most important working-capital pressure corporates will face next year, while only 14% chose higher financing costs.

When asked to select which three corporate behaviours they expect to see most clearly in 2026, 71% of respondents indicated that they expect greater diversification of procurement, while 43% indicated more regional sourcing, and 29% indicated higher inventory buffers.

Those are expensive choices that firms make when they are more concerned with continuity than cost optimisation, which leads us to believe that in 2026, working capital decisions will be made with resilience in mind as much as cost.

Despite this, there are some indications that this year show some promising signs for working capital solutions. John Pfisterer, Managing Director, Global Head of Revenue Strategy at LiquidX, said “[History will look back at 2026 as the year when] increased transparency to working capital solutions began to show signs of progress.”