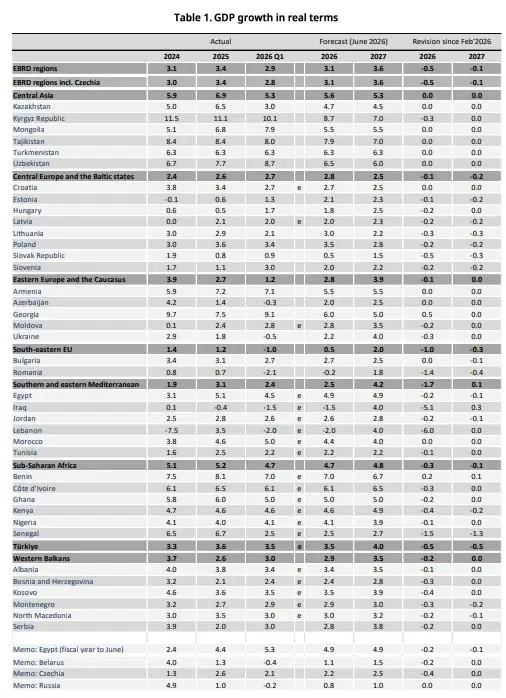

The European Bank for Reconstruction and Development (EBRD) projects a slowdown in aggregate economic growth across its regions from 3.4% in 2025 to 3.1% in 2026, followed by a recovery to 3.6% in 2027 in its latest regional outlook report titled “Strai(gh)t talk”.

This revised outlook, published in June 2026, indicates a decrease of 0.5 percentage points for 2026 and 0.1 percentage points for 2027, compared to the February 2026 forecast.

The main reason for this revision is the rising conflict in the Middle East, which has disrupted energy markets and trade, negatively affecting regional economic growth.

Year-on-year growth for the first quarter of 2026 is estimated at 2.9%, with significant underperformance in key economies like Egypt, Kazakhstan, Romania, Türkiye, and Ukraine.

The report highlights that the conflict has compounded an already challenging external environment marked by weak manufacturing momentum and rising global trade tensions.

Beata Javorcik, EBRD Chief Economist, said, “The conflict in the Middle East has delivered a new shock to regions already navigating weakness in manufacturing industries and fragile fiscal positions.”

“Higher energy costs are squeezing competitiveness, reigniting inflation and tightening fiscal space at a time when many economies can least afford it.”

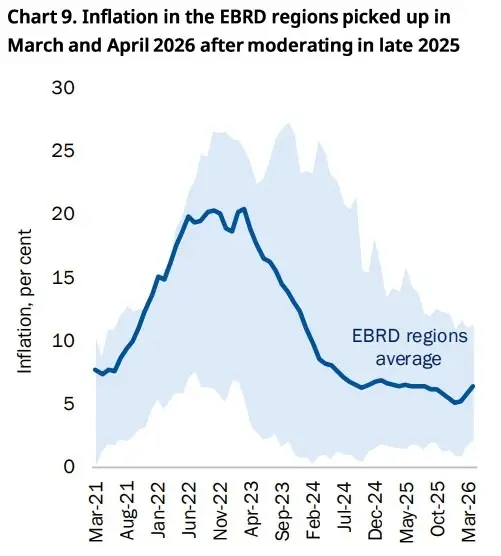

Inflation dynamics and energy price pressures

Inflation in the EBRD regions, which had eased in late 2025 due to favourable real interest rates and slower wage growth, surged again in early 2026.

From February to April 2026, average inflation rose by 1.2 percentage points to 6.4%, mainly due to rising energy and food prices.

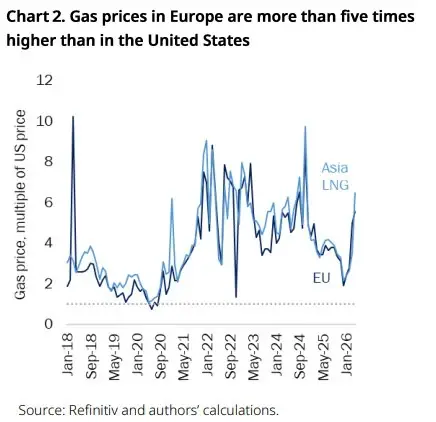

The conflict in the Middle East has caused significant damage to energy infrastructure and disrupted shipping through the Strait of Hormuz, leading to sharp rises in oil and gas prices.

The widening gap between European and US energy costs, particularly gas prices, which now exceed a factor of five, has undermined European industrial competitiveness.

Electricity prices in Europe remain substantially higher than in the United States, reinforcing a structural shift away from energy-intensive industries toward less energy-dependent sectors.

Energy and food constitute larger shares of consumer baskets in the EBRD regions than in advanced economies, exacerbating inflationary pressures. Currency depreciations against the US dollar in some economies have further intensified inflation.

A glance at the sectoral and regional impacts

The energy shock has sped up structural changes in industrial production across the EBRD regions. Manufacturing sectors are still struggling, while construction, ICT services, and trade are showing resilience.

The report says that specific disruptions, including a three-month outage of the Druzhba pipeline in Hungary, highlight vulnerabilities linked to energy dependence.

Regional growth projections vary significantly.

In Central Europe and the Baltic States, growth increased to 2.6% in 2025 and is forecast to rise slightly to 2.8% in 2026 before moderating to 2.5% in 2027.

This downward revision reflects the impact of the energy shock but is partly offset by rising investment ahead of Recovery and Resilience Facility deadlines.

In the South-eastern EU, growth was 1.2% in 2025 and is expected to decelerate further to 0.5% in 2026, largely due to fiscal consolidation and political uncertainty in Romania, before rebounding to 2.0% in 2027.

Growth in the Western Balkans is expected to slow to 2.6% in 2025, with a slight rebound to 2.9% in 2026 and an acceleration to 3.5% in 2027, driven by public investment and infrastructure projects.

Central Asia saw growth peak at 6.9% in 2025 and is expected to moderate to 5.6% in 2026, and 5.3% in 2027, with the Kyrgyz Republic’s 2026 forecast revised downward due to anticipated EU sanctions.

In Eastern Europe and the Caucasus, growth slowed to 2.7% in 2025 and is projected to be around 2.8% in 2026. It is weighed down by higher energy import costs and weaker tourism, before rising to 3.9% in 2027.

Ukraine’s 2026 growth forecast has been lowered to 2.2% due to ongoing conflict-related disruptions.

Turkey’s growth was at 3.6% for 2025, slowing slightly to 3.5% in 2026, and rising to 4.0% in 2027. The downgrade was due to high energy costs, inflation, and potential impacts from the Middle East conflict.

The Southern and Eastern Mediterranean region would see growth decline from 3.1% in 2025 to 2.5% in 2026, with Lebanon and Iraq facing the largest decreases. A recovery to 4.2% is anticipated in 2027, although risks remain.

Sub-Saharan Africa’s growth is projected to decrease from 5.2% in 2025 to 4.7% in 2026 and then 4.8% in 2027, due to trade disruptions, rising energy import costs, and weak investment.

Policy responses and fiscal challenges

Nearly 75% of EBRD economies have implemented measures such as energy tax cuts, fuel price caps, and targeted subsidies to support consumers and conserve energy in response to the energy price shock.

Central banks have adopted varying monetary policy approaches, with some maintaining or increasing policy rates to combat inflation, while others have paused rate cuts.

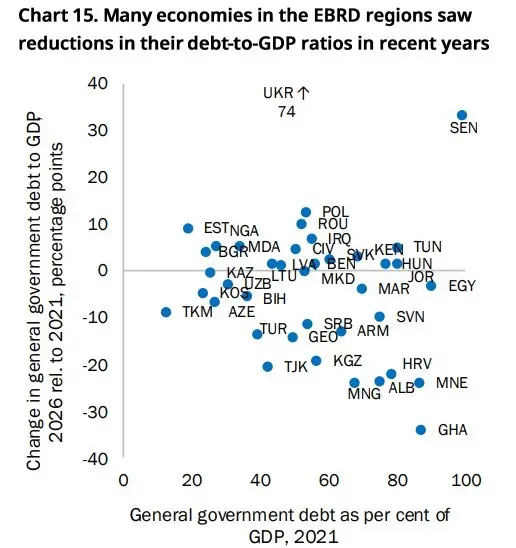

Fiscal positions have deteriorated, particularly in the southern and eastern Mediterranean and sub-Saharan Africa, where debt-to-GDP ratios and interest burdens were already elevated. Tighter global financing conditions have increased borrowing costs, especially for highly indebted economies.

The report also discusses the European Commission’s Industrial Accelerator Act, aimed at boosting industrial competitiveness and reducing foreign dependency in strategic sectors. Emerging European industrialised economies are best positioned to benefit, though opportunities for third countries depend on eligibility criteria yet to be defined.

The risks involved and outlook ahead

The report highlights major risks to the regional outlook, mainly due to the ongoing Middle East conflict and its economic effects. Rising energy and food prices are likely to limit domestic consumption and continue inflation.

Other risks include weaker demand from trading partners, delays in infrastructure projects like Rail Baltica, and geopolitical uncertainties.

Some economies could benefit from structural reforms, increased investment, and diversification efforts despite current challenges. Growth is expected to slow down in 2026 but may recover in 2027 if external shocks are resolved and effective policies are implemented.

Staright to the Strai(gh)t talk.