Lately, it has been hard to miss the headlines about defence budgets.

In the US, Congress has approved a record-breaking 901-billion-dollar defence bill for 2026, with its President already talking about increasing that figure by more than 50% to $1.5 trillion for 2027. At the Hague NATO summit in 2025, member states pledged to increase defence spending to five per cent of GDP, up from the previous targets of two per cent, which, until recently, only a handful had even been able to meet. In Europe, the Russian invasion of Ukraine has exposed how far decades of complacency have weakened the continent’s ability to defend itself against serious threats. Many are discovering that “catching up” carries a very real price tag.

The cost of modern military equipment is a big part of that story. Today, a single air defence battery can run into the billions. Individual interceptor missiles and precision-guided shells are counted in millions or hundreds of thousands per shot. Indeed, Operation Midnight Hammer, the United States’ June 2025 strike against Iranian nuclear facilities, is estimated to have cost taxpayers more than $200 million.

For as long as states have built militaries and fought wars, they have had to work out how to pay for them. As we will see, many of the financial innovations and improvisations that have been put in place over the centuries because of wartime desperation have gone on to become staples of national and international financial systems, long outliving the conflicts out of which they were born.

The rest of this article aims to step back into that longer history of Western war finance, travelling from tribute in antiquity, through the rise of national debt in early modern Europe, to the financial engineering of the world wars, and the weaponisation of finance in our own time.

As with any study of history, the aim is not to discover a solution in the pages of the past, but rather to understand the context with which the current situation fits into the broader narrative, and use that refined understanding to ask better questions. The hope is that, with this history in mind, today’s conversations about rising defence spending will feel a little more like the latest chapter in an old war story that dates back to ancient times.

And that is just where we will begin.

The ancient world and the earliest foundations of war finance

In antiquity, warfare often paid for itself – well, at least for the victor. Conquering states usually levied tribute on subjugated peoples, which brought in more resources that the state could use for further conquests. The Persian Empire, for example, organised a vast system of tributes from its provinces to pay for its armies. This system ultimately created a cycle in which war begot tribute, and tribute financed more war.

But even in antiquity, the need to pay for war required some financial innovation. Temple treasuries, which were among the largest repositories of wealth in many ancient societies, often came to the aid of the state during emergencies. In 5th-century BCE Athens, for example, sacred temples lent significant sums to the city to meet its wartime needs. Inscriptions from the Peloponnesian War era record how Athens borrowed from the temples of Athena and other gods, effectively tapping religious funds as war loans to be repaid with interest. In Rome, an array of fiscal pressures, including the need to pay for troops, caused emperors to repeatedly reduce the silver content of the denarius coin (in a process that is known as debasement), effectively inflating away costs at the expense of the currency’s value.

While these ancient war financing methods do not seem particularly innovative by today’s standards, they did lay an early foundation for the more sophisticated and long-lasting innovations that would come in later periods. Que: early modern Europe.

Early modern Europe and the birth of national debt

By the 16th and 17th centuries, warfare had come to be fought on a much grander and more technologically sophisticated scale. This added scale and complexity made the cost of war far higher for states that found themselves engaging with their adversaries, and required far deeper pockets than sporadic plunder and fickle bankers could provide. The era saw an array of experiments in managing the crushing costs of conflict, the most notable of which came from Spain, the Dutch Republic, and England.

Spain, rich with New World silver in the 1500s, fought wars (against everyone from the French to the Ottomans) so incessantly under its Habsburg rulers that they bankrupted the treasury multiple times. Spain’s King Philip II had inherited a system of juros (royal bonds) and relied on Genoese banking syndicates to advance huge loans that were backed by incoming silver fleets and tax revenues. The Genoese bankers innovated sophisticated instruments known as asientos and bills of exchange, routed through settlement networks, to move funds across Europe through fairs in Lyon and Besançon to pay Spain’s armies.

Painting of Philip II by Sir Anthony More (Source: Encyclopaedia Britannica)

This system worked remarkably well, at least as long as times were good for the Spanish. When wars went badly or treasure fleets sank, Spain simply suspended payments, and the system effectively fell apart. Astonishingly, Philip II’s Spain defaulted four times between 1557 and 1596, earning the King his moniker as the “Borrower from Hell”. By the 17th century, perpetual war forced Spain to cede its financial primacy to more creditworthy rivals. Out of Spain’s shadow came the Dutch Republic, which pioneered a stable, low-interest public finance system that is often hailed as the world’s first financial revolution.

During their lengthy war for independence from Spain (known as the Eighty Years’ War, as it lasted from 1568-1648), the Dutch provinces (especially Holland) transformed their finances by consolidating numerous short-term, high-interest loans into long-term bonds and annuities that were funded by an extensive tax base (with large excise taxes on popular items like beer and salt). The Dutch faithfully serviced these debts, which made investors confident enough to accept lower interest rates for their capital.

By the mid-17th century, the Dutch Republic enjoyed such good credit that it could borrow voluntarily at rates around 5% or less. This was radically different from Spain’s rates of 20-30%. The result was that the Dutch could raise money in war far more cheaply than their adversaries. And raise money they did. By the late 1600s, the Dutch public debt was enormous by the standards of the time (coming in at an estimated 120-140 million guilders), yet sustainable. Their financial techniques soon inspired their upstart neighbour across the North Sea.

In England, the decisive shift in war finance arrived in 1694 with the creation of the Bank of England, which helped convert emergency wartime borrowing into a repeatable system backed by parliamentary taxation.

Case study: The Bank of EnglandBy the early 1690s, England was struggling to finance its war against Louis XIV of France. Military spending had soared, and the Crown’s already shaky credit had been damaged by years of political instability. After a costly naval defeat in 1690 at the Battle of Beachy Head, the government urgently needed fresh capital and had no credible way to raise it. In 1694, a group of financiers led by Scottish trader William Paterson proposed a permanent joint-stock bank capitalised by private investors, with the funds immediately lent to the government. In exchange, the subscribers would be incorporated as “The Governor and Company of the Bank of England” and receive certain privileges, including the right to issue notes. Parliament approved the plan, and investors quickly subscribed £1.2 million at 8% interest, secured by new customs duties.

Sir William Paterson (Source: The British Museum) The money went straight to the war effort. Government pay offices, including the army and navy departments, held funds at the Bank and made payments by drafts on it. The arrangement gave England a stable institution capable of issuing paper money and giving lenders confidence that interest would be repaid through Parliament-controlled taxation, something the country had never had before. This credibility arguably became England’s greatest military asset. Through the War of Spanish Succession (1701-1714), the Seven Years’ War (1756-1763), and the Napoleonic Wars (1803-1815), the Bank took an array of measures, including arranging loans, issuing notes, and creating secondary markets for government bonds. This meant that investors could buy and sell these securities, which kept the state’s borrowing costs manageable even as the national debt grew. The contrast with France (whose Revolutionary paper money collapsed in value) was stark. Over time, the Bank of England evolved into the backbone of Britain’s financial system, with its notes becoming widely accepted as currency. Although it remained a private institution until it was nationalised in 1946, its interests were deeply aligned with those of the state, and its fortunes rose and fell with Britain’s ability to win wars and maintain its credit. Born of wartime desperation, the bank has since become the anchor of one of the world’s most influential economic systems. |

Britain’s financial model gave it a clear military advantage as it was able to finance heavy military expenditures while France, its biggest rival, was unable to do so without enduring financial ruin. Nowhere was this more evident than in the Napoleonic Wars.

The Napoleonic era and the rise of total mobilisation

The Napoleonic Era ushered in an age of industrial-scale mobilisation, complete with mass conscription and astronomical war expenditures. While earlier European wars could be vast, they were usually fought by relatively small professional forces that states tried to sustain without permanently reorganising society. That was no longer the case by the turn of the 19th century.

To confront Napoleon’s France (a state with nearly three times Great Britain’s population by some estimates), Britain had to harness its growing industrial economy and its now-mature financial system, which had been built in the previous century.

For Britain, the wars, despite being ruinously expensive, ultimately proved to be affordable as a result of its prudent fiscal planning. At the outset in 1793, Britain’s national debt was already high (over 120% of GDP), but the government initially leaned on more debt. In the first campaigns against revolutionary France (1793-1798), fully 90% of British war expenditures were financed by loans, much of which was facilitated by the Bank of England by creating money and credit.

The outbreak of the war with France stoked fear and panic among the British public, causing so many people to hoard gold that the Bank of England’s reserves were nearly depleted by February 1797. This prompted the government to suspend the gold convertibility of Bank of England notes later that same year, which allowed it to print additional paper money to lend to the Treasury. By sidelining the gold standard, Britain avoided running out of hard currency and could sustain the fight with fiat money, though at the cost of some price inflation. Britain also dramatically raised taxation during the Napoleonic Wars. In 1799, Prime Minister William Pitt the Younger introduced Britain’s first-ever income tax specifically to help pay for the war. Over the course of the war, the rate rose to 10% on incomes over £200, a significant but not crippling rate.

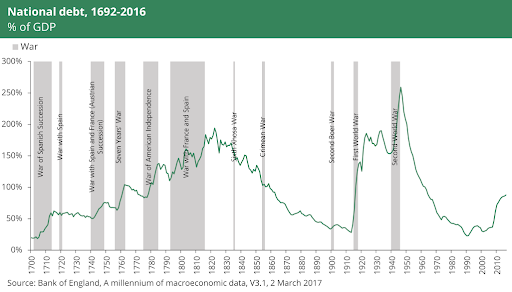

By the final campaigns against Napoleon, this income tax and higher excises became major wartime revenue sources. By war’s end in 1815, the UK national debt had ballooned to the staggering sum of £848 million. This was an unprecedented debt burden (one that would not be equalled until the World Wars of the 20th century), yet Britain did not default. The government honoured its obligations, and over the 19th century, gradually paid down and refinanced the debt on gentler terms.

(Source: House of Commons Library)

In addition to equipping its own forces during the period, British financial might also bankrolled those of its allies. During the Napoleonic Wars, London became the arsenal and banker of European resistance. Britain extended hefty subsidies to Prussia, Austria, Russia, and smaller states to keep them in the fight against France. These war subsidies, nicknamed the “Golden Cavalry of St. George” after the gold guinea coins bearing England’s patron saint, reached peaks of over £5 million annually (hundreds of millions in today’s pounds).

The Guinea, issued by the Royal Mint between 1663 and 1816. (Source: Royal Mint)

For example, in 1813, Britain was subsidising nearly 450,000 allied troops in Europe, helping offset Napoleon’s numerical advantages. It was effectively an early form of Lend-Lease, where Britain used its superior access to credit and industry to furnish allies with money and matériel, recognising that bankrolling coalitions was cheaper than fighting alone. This strategy of subsidising allies to bleed the enemy had been used in prior wars (Pitt had subsidised continental powers against Revolutionary France in the 1790s as well), but never on the scale seen in the final push against Napoleon.

On the French side, Napoleonic war finance remained more contingent on conquest and extraction than on deep domestic borrowing. Napoleon’s regime drew heavily from occupied territories, and when those flows began to dry up, it resorted to taxation and requisitions at home and across the Empire. Napoleon’s creation of the Banque de France in 1800 helped, but it still did not give France Britain’s capacity to fund long wars. The continental giant was thus increasingly forced to resort to measures that strained the economy, perhaps uncoincidentally, just as its military fortunes began to turn for the worse.

In contrast, Britain’s economy was booming under wartime demand, and the Royal Navy’s control of the seas kept trade flowing (albeit re-routed) and customs revenues healthy. Ultimately, Britain’s deep pockets and financial planning proved as decisive as Wellington’s troops at Waterloo.

The Napoleonic era thus demonstrated the coming of total war economics. Indeed, after 1815, Britain chose not to extinguish its huge debt but to manage it long-term via the sinking fund and refinancing (interestingly, much of that wartime debt remained on the books for over a century, with some undated gilts still outstanding into the 21st century and major remnants redeemed in 2015). The need to finance the seismic wars of the era had, in essence, helped build the financial institutions that would power Britain’s 19th-century industrial rise.

The American Civil War and the remaking of America’s financial system

Across the Atlantic, the mid-19th century provided another watershed in war finance during the American Civil War (1861-1865). Confronted with the colossal expenses of raising million-man armies and supplying a modern war, the US federal government was also forced to innovate financially. By war’s end, many of these innovations had reshaped the American economy and laid the groundwork for US financial power in the following century.

When the Civil War began, the US government was ill-prepared to pay for it. In 1860, with less than $65 million in federal debt on the books, the Union did not have a mature federal bond market to turn to. To make matters worse, the country also lacked both a central bank (the Second Bank of the US had expired in 1836) and a uniform paper currency (most money was issued by private banks). Treasury Secretary Salmon P. Chase had to improvise fast.

His solutions came as a series of landmark laws. First was the Legal Tender Act of 1862, which authorised the printing of $150 million in new paper money called “Greenbacks” (named for the green ink on one side). These notes were declared legal tender for all debts, though they were not redeemable for gold or silver during the war. Over the course of the war, the Union issued more than $450 million in Greenbacks, which were pure fiat money backed only by the government’s promise and tax power.

A one-dollar Greenback, first issued in 1862, featuring Salmon Chase.

This was the first time the US government floated a national fiat currency on such a scale. It was a controversial step (Greenbacks did indeed depreciate against gold in the market), but it helped the Union avoid insolvency when gold reserves ran low.

Simultaneously, the Union government undertook massive bond sales to the public. Under the energetic efforts of Philadelphia banker Jay Cooke, the Treasury marketed war bonds to ordinary investors with a nationwide sales effort. Cooke was engaged in 1862 to sell $500 million in bonds, and in 1865, he again led a major campaign, disposing of three series’ totalling $830 million.

To support both the issuance of Greenbacks and the marketing of bonds, Congress next passed the National Banking Act of 1863. This act created a system of nationally chartered banks that were required to hold Union bonds as reserves and could issue uniform banknotes for up to 90% of those bond holdings. The Act, through a new tax on their use, also effectively drove old state-bank notes out of circulation, ensuring that the new National Bank Notes (and Greenbacks) dominated the currency. This was the birth of the national currency and a more centralised banking structure within the United States.

These measures translated into unprecedented federal spending. The Union’s war expenditure totalled about $3.4 billion (equivalent to many tens of billions today), dwarfing all previous US budgets combined. Government debt swelled from $65 million to $2.6 billion by 1865, a 40-fold increase in just four years. Yet, thanks to these new fiscal tools, the Union did not default or collapse financially. Inflation did occur (Greenbacks fell to as low as 35 cents on the dollar at their weakest), but the economy adjusted, and after the war, the US gradually redeemed Greenbacks for gold (resuming specie payments in 1879 following the passing of the Resumption Act of 1875).

In contrast to their northern adversaries, the Confederate States lacked comparable financial depth. Cut off from tariff revenue by the Union blockade and reluctant to levy sufficient taxes, the Confederacy financed most of its war by printing paper money (over $1 billion worth of Confederate notes), far outstripping what the economy could bear. By the war’s end, these notes were worth about six cents on the dollar. Echoing the historical trend, this financial collapse was a considerable precursor to the Confederacy’s military collapse.

The world wars and the creation of the postwar economic order

The twentieth century again brought warfare to a previously unimagined degree, both in terms of technological sophistication and destructive capabilities. World War I (1914-1918) introduced the era of the truly total war economy, where entire national finances were subordinated to the war effort. Then World War II (1939-1945) went even further, blurring the line between soldiers and civilians on the economic front and giving birth to the international financial order that still, albeit increasingly fragilely, exists to this day.

Both wars turned to many of the now-familiar tools that we have explored from previous conflicts, such as massive bond drives, new taxes, and inflationary money-printing, but each conflict also spurred unique financial strategies.

In World War I, all the major powers abandoned the gold standard early on and financed their war efforts through some combination of inflation and debt, most popularly in the form of war bonds, which became easier to sell because of an inflated sense of patriotism that accompanied the conflict. The United States, for instance, raised $20 billion during its relatively brief stint in the conflict through its Liberty Loan and Victory Loan drives. In Britain, the public subscribed to multiple issues of War Loans, while France issued rentes and victory bonds to its populace.

By war’s end, roughly half of the war costs of Britain and France were covered by domestic bond sales and savings certificates. The other half, however, often came from less benign sources like heavy taxation (income taxes rose sharply, reaching up to 30% in Britain by 1918) and central bank credit creation. All major central banks (i.e., the Bank of England, Banque de France, Reichsbank, etc.) expanded the money supply to purchase government bonds or lend to the treasury, which naturally resulted in inflation. By spring 1918, the US Federal Reserve (created only in 1913) had also bought about $10 billion of US bonds and Treasury certificates to support the war effort.

The upheaval of WWI’s finance was perhaps most dramatic in those empires that collapsed. Germany, blockaded and unable to borrow externally, resorted to printing enormous quantities of marks, which led to the famous postwar hyperinflation of 1922-3 as the delayed financial cost of war was paid. By contrast, countries like Britain and the US, despite coming out with heavy debts, had only moderate inflation, thanks to stronger tax regimes and credible institutions.

The end of WWI left a tangle of inter-Allied debts and German reparations, which became a source of instability in the 1920s. Many experts argue that the war’s financial hangover contributed to the Great Depression (c. 1929-1939) and set the stage for renewed conflict. Germany’s rearmament in the 1930s also produced one of the era’s most inventive – and dangerous – financing workarounds.

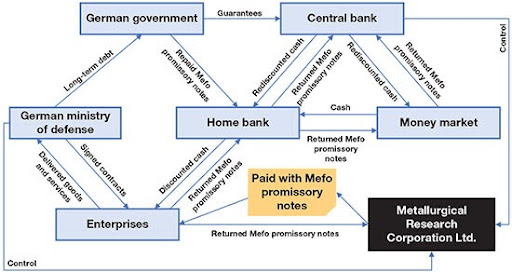

Case study: Nazi Germany’s Mefo billsAfter Hitler came to power in 1933, Germany was still bound (at least ostensibly) by the Versailles Treaty’s limits on armaments and by a strict 4.5% interest ceiling on public borrowing. Since the hyperinflation of the early 1920s, the Reichsbank, by law, could not lend more than 100 million Reichsmarks directly to the government. Yet Nazi rearmament ambitions required billions of Reichsmarks. The answer to this conundrum came from Hjalmar Schacht, Hitler’s Economics Minister and former head of the Reichsbank. Schlact created a shell company called Metallurgische Forschungsgesellschaft, m.b.H. (nicknamed Mefo). This dummy corporation, with merely 1 million Reichsmarks capital, had no real operations. It existed solely to issue “Mefo bills”, which were essentially promissory notes that arms manufacturers and contractors could use as payment. When a firm delivered armaments (say, producing tanks or planes for the Wehrmacht), instead of immediate cash, it received a Mefo bill drawn on the dummy company. These bills were short-term (6 months maturity, extendable repeatedly) and carried a 4% interest rate, which made them attractive enough for banks to accept. Crucially, these bills could be rediscounted at any German bank or ultimately at the Reichsbank for cash. In practice, that meant they were as liquid as a government check. However, because they were technically obligations of Mefo (the private company), not directly of the German state, they did not show up in official budget debt figures. The scale of this operation was enormous, yet kept secret. By 1938, a staggering 12 billion Reichsmarks worth of Mefo bills were outstanding, equivalent to about 40% of Germany’s entire public debt. To put it in perspective, standard government bonds at that time were around 19 billion RM, meaning a huge chunk of Nazi rearmament was essentially financed off the books.

The design of Mefo Bills (Source: Debt and entanglements between the wars (Chap. 6), published by the IMF) Schacht continually extended the bills’ maturities (eventually to 5 years) to avoid redemption in cash, thus preventing an outflow of funds that could trigger inflation. As long as everyone had confidence in the Reichsbank’s guarantee of these bills, they circulated almost like currency. Indeed, they were a form of proto-shadow currency fueling the armament boom. Factories could use Mefo bills to pay sub-suppliers or to secure bank loans, thereby increasing the money supply without formally printing Reichsmarks. Between 1933 and 1938, German military spending skyrocketed, with industrial output soaring and unemployment plunging. All the while, official inflation figures remained unusually modest. Prices didn’t explode in part because the government rarely had to actually redeem Mefo bills for cash, as most investors rolled them over, trusting eventually they’d be paid. The risk, of course, was what would happen if confidence faltered or if redemption was demanded en masse. By April 1938, with war looming, the Nazis finally discontinued new Mefo issues. The outstanding 12 billion Reichsmarks in bills were gradually converted to long-term government debt or paid off as wartime inflation set in. Schacht himself was pushed out of the government by 1939 (he had disagreements with Hitler, and once rearmament reached an irreversible point, Nazi leadership cared less about hiding it). In a way, the regime had run a national-scale Ponzi scheme for rearmament, issuing paper claims to wealth that did not yet exist, betting on future conquests to make good on them. The legacy of Mefo is a cautionary tale. Such artifices can facilitate rapid armament, but they accumulate hidden debt that can destabilise an economy. In Germany’s case, had the war not started by 1939, the Reich would likely have faced a financial reckoning; Schacht himself warned that by the 1940s, Germany might go bankrupt if it didn’t slow spending or go to war (in fact, the guns of WWII masked and then erased the Mefo obligations in the flood of wartime finance). By conjuring money from an imaginary company, the Nazis bought crucial time to build their war machine. It was a triumph of financial engineering, and a precursor to the destruction that that engineering would help unleash. |

Following the outbreak of war, Allied governments applied some lessons of the previous war. The US and Britain again issued war bonds (the US “Series E” War Bonds and Britain’s “War Savings” campaign). Overall, 85 million Americans – over half the population – purchased war bonds, raising around $185 billion (over $3 trillion in today’s dollars) between 1941 and 1945. These bonds not only funded about half the cost of WWII for the US, but also helped keep inflation in check by absorbing excess purchasing power in an economy now flush with wartime jobs but short on consumer goods.

World War II also saw novel forms of international war finance. The most notable was the US Lend-Lease program. Starting in 1941, the United States (while still officially neutral) began “lending” war materiel to Britain (and later the USSR, China, and other Allies) on the understanding that payment could be made after the war, or in kind. Over the course of WWII, the US provided an astounding $50 billion (equivalent to nearly $900 billion today) worth of weapons, supplies, and food to Allied nations via Lend-Lease.

In reality, much of this aid was never repaid in dollars, and it did not have to be. Instead, as part of the Lend-Lease agreements, the Allies, especially Britain, committed to postwar economic cooperation. Article VII of the Lend-Lease accords famously stipulated that the assistance was given in exchange for a joint aim of establishing a liberalised international trade and monetary system after the war. It was a strategic investment by the US that helped win the war and pave the way for the Bretton Woods Conference in 1944 and the creation of the postwar economic order.

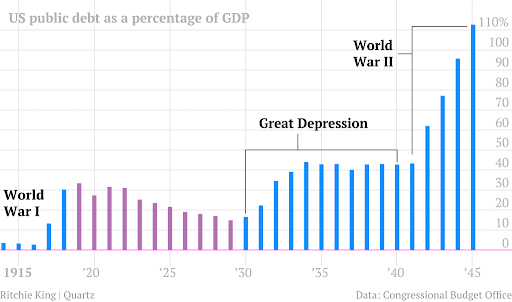

By 1945, the global economic landscape had been remade. The war’s victors carried unprecedented debts (Britain was essentially bankrupt and dependent on a US loan; the US debt was over 110% of GDP after spending the equivalent of $4 trillion on war), but the institutions born of the war (like the Bretton Woods bodies) continued to influence peacetime. In the defeated nations, wartime financial collapse prompted a complete reset. Germany’s currency was refounded in 1948 (Deutsche Mark), as was Japan’s in 1949 under US guidance. These efforts set the two nations up for postwar recoveries.

(Source: The Atlantic)

From the Cold War to today: The weaponisation of finance

In the second half of the 20th century and into the 21st, direct great-power wars gave way to the proxy wars and arms races of the Cold War (c. 1947-1991). Financing these protracted struggles required its own innovations and adaptations.

During the ideologically-fuelled period, the United States and Soviet Union poured vast resources into military buildup (the US alone spent trillions on defence), but they generally avoided direct armed conflict with each other for fear of nuclear escalation. Instead, economic and financial pressure became a key front in the rivalry. The US imposed trade embargoes and sanctions on Communist bloc countries (for example, the long-standing embargo on Cuba and controls on technology exports to the USSR).

Washington also used financial aid as a weapon. The Marshall Plan after WWII injected $13 billion into Western Europe to fortify it against communism, while the Soviets responded with their own aid to Eastern Europe (albeit on a smaller scale). Both superpowers also subsidised allies, with the USSR propping up client regimes with cheap oil and loans (often never repaid), and the US similarly giving generous terms to allies like South Vietnam or Israel.

One fascinating byproduct of Cold War paranoia was the birth of the Eurodollar market. In the late 1950s, the USSR feared its dollar deposits in New York could be frozen due to rising tensions. In response, Moscow shifted large dollar holdings to its bank in London (Moscow Narodny Bank) and had them placed as loans in Europe. This was the start of Eurodollars. Western banks quickly jumped in, appreciating that these offshore dollars were free of reserve requirements and US oversight.

As the Cold War wound down, major powers started to prefer economic warfare over traditional military force in many cases. The United Nations Security Council, which had only rarely used sanctions before, suddenly resorted to their use time and again against regimes in Iraq, Yugoslavia, Libya, and others. Indeed, the 1990s earned the label of the sanctions decade. Blocking trade, freezing assets, and denying adversaries access to global banking became seen as powerful, lower-cost weapons.

In an age of dollar dominance (which was institutionalised by Bretton Woods but reinforced over the following decades), the US also discovered that it could essentially weaponise access to the dollar-based financial system. Twenty-first-century conflicts increasingly involve these tactics. Sanctions on Iran, for example, have sought to curtail its nuclear program by cutting Iranian banks off from SWIFT and oil revenues. Russia’s 2022 invasion of Ukraine met with some of the harshest financial sanctions ever as Western nations froze hundreds of billions of Russia’s central bank reserves and expelled key Russian banks from international networks.

Meanwhile, the United States’ adversaries have been developing countermeasures. Russia and China, for example, have each built alternative payment systems (SPFS in Russia and CIPS in China). Many sanctioned states will also turn to cryptocurrencies, barter, or shadowy intermediaries to move money. Non-state actors (like the Islamic State at its height) rely on informal networks like smuggling to finance their wars, precisely to evade formal surveillance.

Thus, the landscape of war finance today is one of highly complex, interconnected networks, where much of the action takes place in the penumbra of the formal system. From clandestine arms funding to cyber-attacks on banking infrastructure, contemporary conflicts have increasingly played out in the financial domain.

But with military budgets suddenly on the rise and war coming “back in vogue”, as Pope Leo XIV orated in an address on 9 Jan 2026, the future of defence, and with it defence finance, may soon look quite different.

An old bill, due again

If there is a single thread running through this story, it is that every new way of fighting wars has eventually demanded a new way of paying for it. Tribute, temple loans and shaved coins gave way to national debts and chartered banks, which, in turn, morphed into mass bond drives, central banks, and, eventually, the use of whole financial systems as instruments of pressure in their own right.

Early rulers could squeeze tribute from conquered provinces or borrow from a narrow circle of bankers. Later governments turned to their own citizens, inviting them to lend through bonds or obliging them to shoulder higher taxes and inflation. More recently, states have learned to pass some of the cost outward, by leaning on allies, institutions like those that comprise the global monetary system, or sanctions that impose losses on others as well as themselves. At each stage, the question of “How to pay?” has always been inseparable from “Who ultimately pays?”

It is also hard to miss how often financial ingenuity has come with hidden risks. The Dutch and British discovered that deep, trusted capital markets could be a strategic asset, but also that large debts have a tendency to linger long after the guns fall silent. Mefo bills allowed Germany to rearm at speed, but left a pile of off-balance-sheet claims that could only really be cleared by the fires of war. Fiat money, war bonds, sanctions and offshore dollar markets have all, in their own way, pushed the immediate pressure of conflict into the future or onto someone else. That can buy time, but it also tends to store up tensions that surface years later in the form of inflation, political backlash, or other crises.

None of this makes the rising defence budgets of today inherently “good” or “bad”. What the longer view does show is that moments like the present are not entirely new. Previous generations also wrestled with the trade-offs between short-term necessity and long-term stability, even if the tools at their disposal looked very different from those being used today, or those that will be developed for use in the years and decades to come.

As defence needs continue to rise, so too will the debates about where the funds to pay for them come from. Looking back at the financial trials and tribulations of past warring generations does not hand us an easy answer, but it does provide a set of reference points that remind us that the decisions made in support of war finance today are liable to shape future institutions and leave marks on economies that can last for centuries.