Trade finance remains a critical enabler of Africa’s international trade, yet the continent continues to face significant challenges in meeting the demand for financing cross-border transactions. The African Development Bank’s 2026 report, Trade Finance Supply in Africa: Post-COVID Trends and Emerging Opportunities, highlights the evolving landscape of trade finance amid the lingering effects of the COVID-19 pandemic and emerging geopolitical tensions.

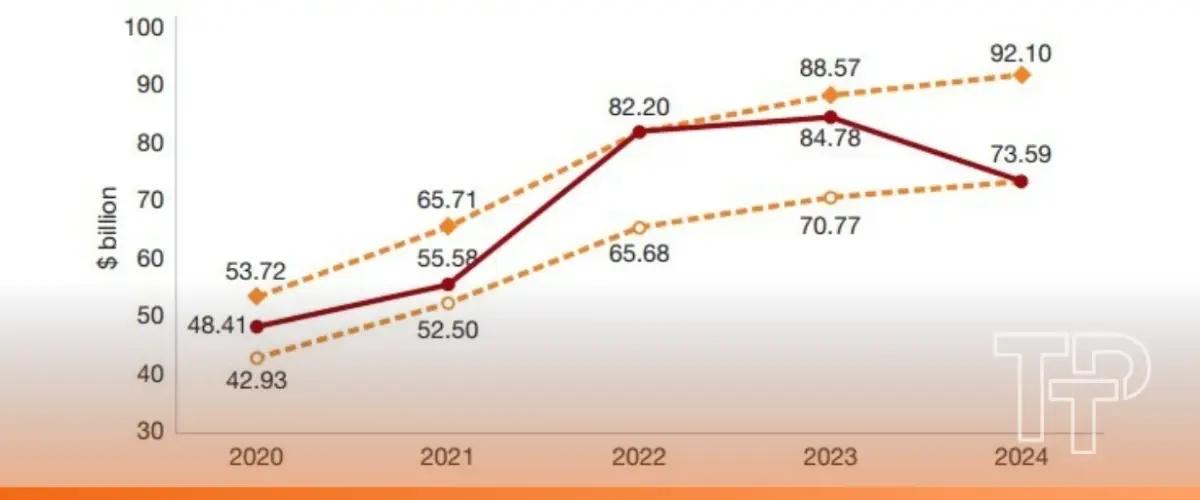

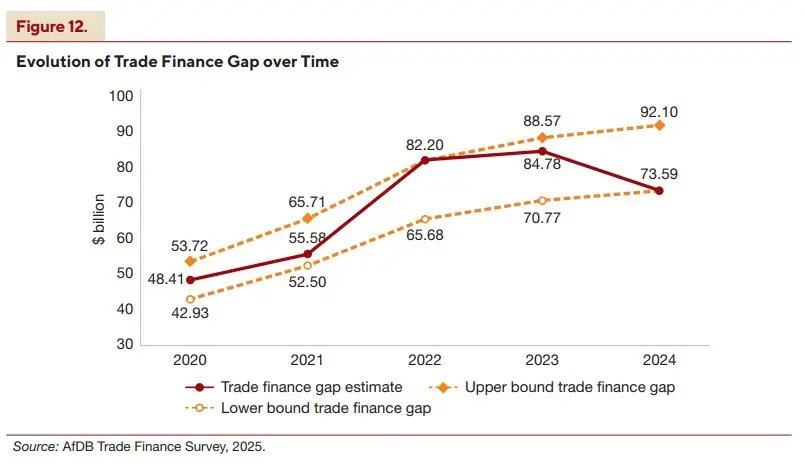

Despite some recovery, the unmet demand for trade finance in Africa was estimated between $74 billion and $92 billion in 2024, representing approximately 5.4% of the continent’s total merchandise trade value.

The report shows that renewed global uncertainties, including elevated energy prices, supply chain disruptions, and tighter correspondent banking relationships, threaten to reverse progress made in narrowing the trade finance gap.

Under moderate to severe scenarios, this gap could widen to as much as $102.6 billion by 2027, erasing nearly a decade of gains in trade finance accessibility.

A glance at bank participation and trade finance assets

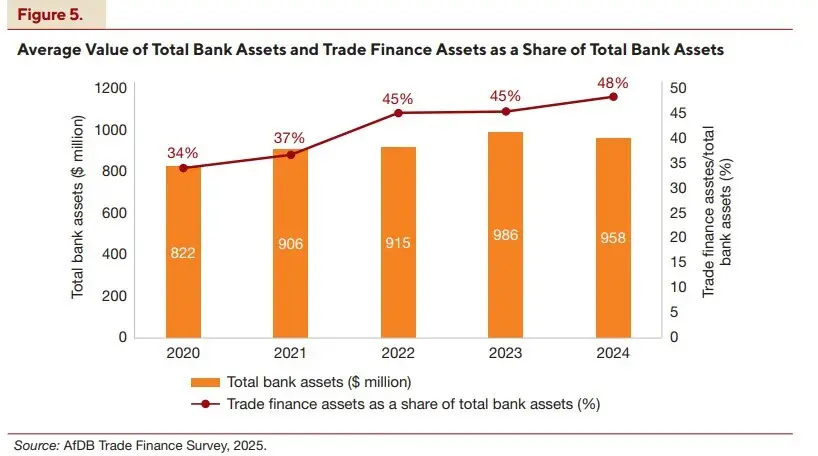

African banks continue to play an important role in providing trade finance, with participation rates steadily increasing over recent years.

The share of banks engaged in trade finance rose from 34% in 2019 to nearly 48% of total bank assets dedicated to trade finance by 2024.

This growth reflects banks’ recognition of trade finance as a strategic business line, supported by increasing volumes of both funded and unfunded trade finance instruments.

However, participation varies by bank ownership type. Majority foreign-owned banks tend to have higher capitalisation and better risk management frameworks, enabling them to provide more trade finance relative to government-owned or locally owned banks. Correspondent banking relationships remain essential, with Citibank and several regional African banks among the top confirming banks facilitating trade finance flows.

The relation between small and medium-sized enterprises and trade finance

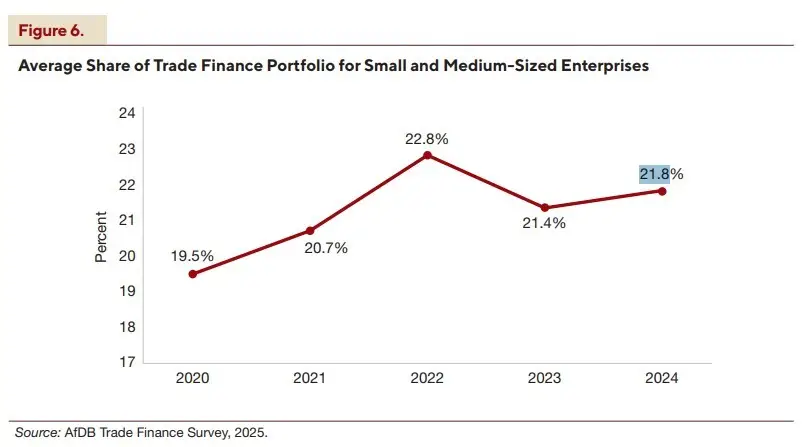

SMEs are a crucial part of Africa’s business environment but struggle to access trade finance.

The allocation of trade finance assets to SMEs varied from 19.5% in 2020 to 21.8% in 2024, largely due to volatility caused by the pandemic.

Despite some recovery efforts, SMEs still experience lower approval rates compared to larger enterprises.

Key challenges for SMEs include insufficient collateral, higher transaction costs, and limited understanding of trade finance products. Default rates among SMEs are higher than the overall trade finance portfolio but remain stable and predictable, presenting an opportunity for development finance institutions (DFIs) to intervene with targeted programs.

Enhancing SME access to trade finance is critical for integrating these businesses into regional and global value chains, thereby supporting economic growth and employment.

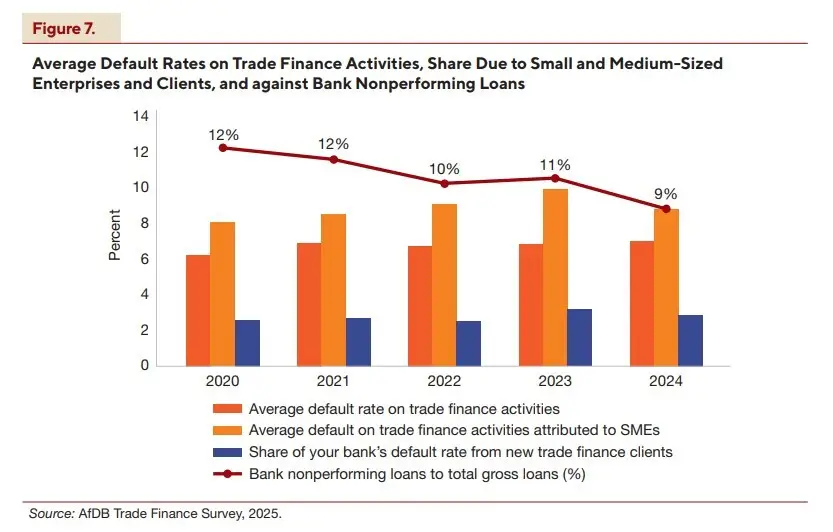

Average default rate in Africa consistent with pre-pandemic time

The average default rates on trade finance loans in Africa have fluctuated between 6% and 7% from 2020 to 2024, remaining consistent with pre-pandemic levels.

Trade finance transactions generally have lower risk due to their asset-backed, self-liquidating, and short-term nature. Nonetheless, default rates in Africa exceed global averages, where defaults on trade-related instruments range from 0.02% to 0.62%.

Defaults attributed to new clients are lower than the overall portfolio, while SME-related defaults have hovered around 9%, reflecting the financing challenges faced by smaller firms.

These figures show the need for risk mitigation and capacity-building initiatives to support sustainable growth in trade finance.

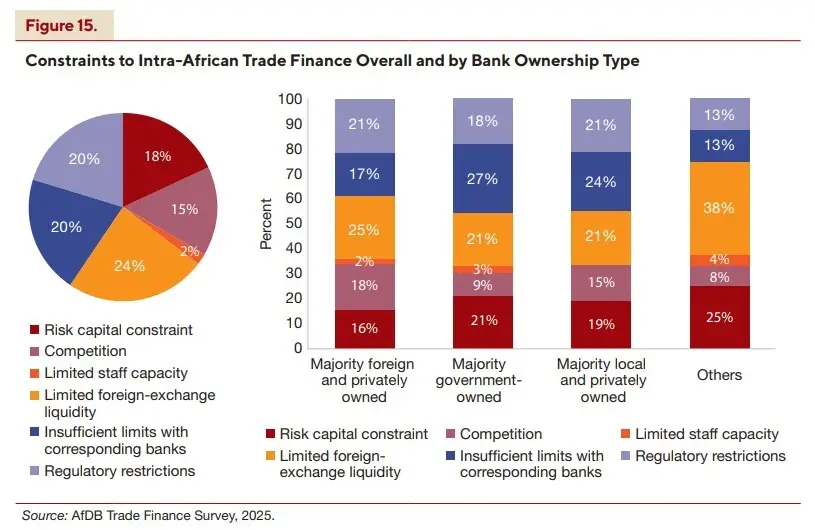

Intra-African trade finance: status and constraints

In 2024, intra-African trade represents just 15.1% of the continent’s total trade, falling behind Europe and Asia.

The African Continental Free Trade Area (AfCFTA) aims to boost this figure by eliminating tariffs and addressing non-tariff barriers, potentially increasing intra-African trade by 15–25% by 2040.

Intra-African trade finance faces challenges similar to general trade finance. This includes limited foreign-exchange liquidity (24%), insufficient correspondent bank limits (20%), risk-capital constraints (18%), and competition (15%).

Government-owned banks are more impacted by correspondent banking and risk-capital issues compared to foreign-owned banks.

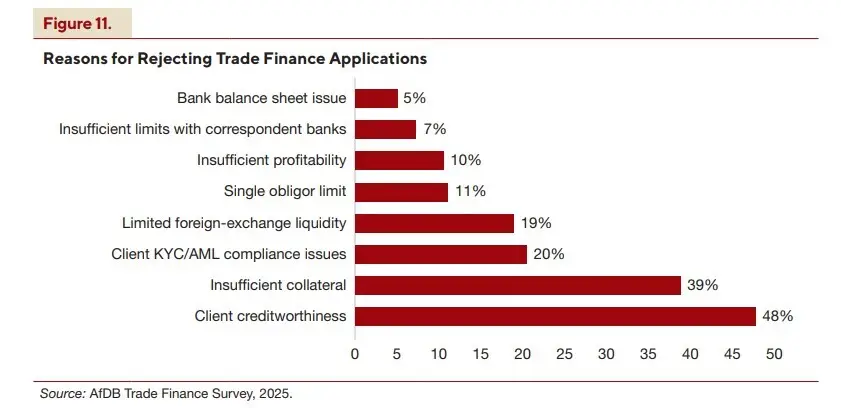

Trade finance gap and reasons for rejection

The trade finance gap remains a major impediment to Africa’s trade expansion. Banks report rejection rates for trade finance applications driven primarily by weak client creditworthiness (48%) and insufficient collateral (39%).

Strict international regulations, such as anti-money laundering (AML) and know-your-customer (KYC) requirements, lead to application rejections.

Structural challenges remain even with attempts by governments, development finance institutions, and partners to enhance credit information, collateral registries, and regulations.

It’s important to tackle these issues to increase access to trade finance, especially for SMEs and intra-African trade.

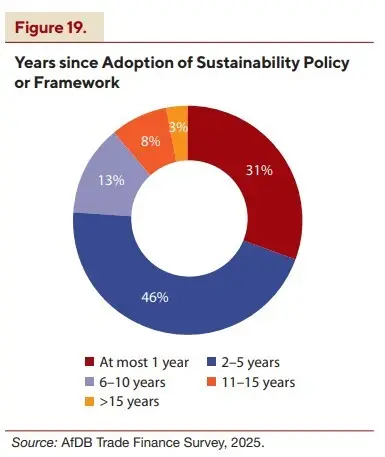

Challenges and opportunities: Digitalisation and sustainability

Digital trade finance solutions can lower transaction costs, increase operational efficiency, and expand access to finance. Only 28% of surveyed banks had adopted digital platforms for trade finance operations by 2025, and more than half anticipate increased digitalisation in the near term.

Sustainability is also gaining prominence, with 62% of banks expecting environmental, social, and governance (ESG) considerations to become central to trade finance activities.

However, challenges are there, including high implementation costs, limited green finance products, regulatory constraints, and low client awareness of ESG tools.

Development finance institutions help tackle important challenges by offering training, technical support, and ways to share risks. Their efforts have helped close the trade finance gap and promote the growth of sustainable and inclusive trade finance in Africa.

The report concludes that strengthening trade finance supply will not only facilitate increased trade volumes but also contribute to broader economic development and integration across the continent.Access the report here. This is the 5th edition of the AfDB’s Trade Finance Report