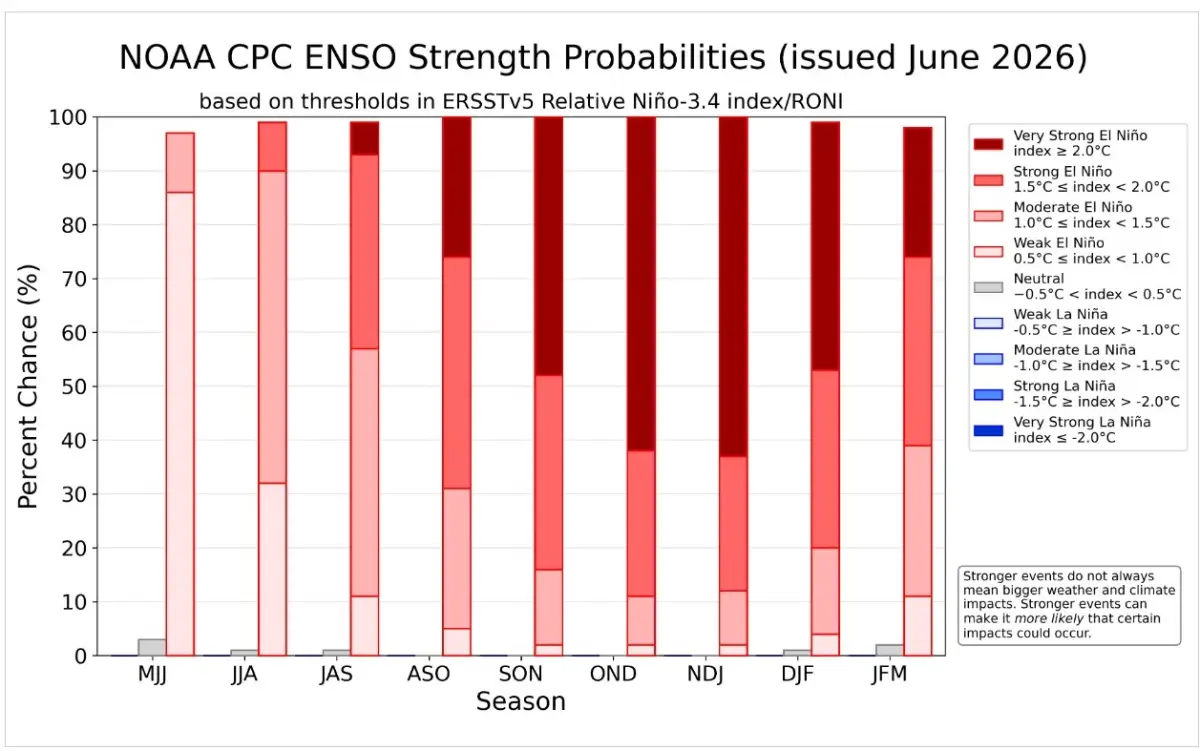

The National Oceanic and Atmospheric Administration (NOAA) confirmed in June 2026 that an El Niño event has officially formed over the Pacific Ocean, with early forecasts suggesting the phenomenon could develop into one of the most intense climate episodes in recorded history.

The World Meteorological Organization has placed the probability of El Niño conditions at over 80% for the June-August 2026 period, rising to 90% for the final quarter of the year. NOAA’s latest projections also indicate a 48% to 63% probability that sea surface temperatures in the tropical Pacific will exceed 2.0°C above average from September 2026 to January 2027, a threshold that would classify the event as “very strong” and potentially comparable to the most severe El Niño episodes on record.

The announcement has prompted urgent warnings about potential disruptions that could cascade through global trade networks and inflict trillions of dollars in economic losses over the coming years.

El Niño: The origin story

The story of El Niño began with observations of coastal fishermen along the shores of Peru and Ecuador in the 17th century. These fishermen noticed a recurring phenomenon – every few years, around the Christmas season, the usually cold, nutrient-rich waters of the Pacific Ocean would warm unexpectedly.

This warming was accompanied by a significant decline in fish catches, disrupting local fishing activities. Because this warming tended to occur near the birth of Christ, it was called El Niño de Navidad, which means “the Christ Child”, a term later shortened simply to El Niño, which is Spanish for “the little boy.”

For many generations, this was regarded as a local seasonal event, a natural pause that allowed fishermen to repair their nets and spend time with family.

The broader scientific comprehension of El Niño’s climatic significance only emerged in the 20th century. In 1904, Sir Gilbert Walker, a British mathematician and then head of the Indian Meteorological Department, was tasked with explaining the unpredictable failures of the Asian monsoon, which had contributed to the devastating famine of 1876-78.

By analysing global atmospheric pressure data, Walker identified a seesaw-like pattern of pressure fluctuations between the eastern and western tropical Pacific, which he named the “Southern Oscillation.” Despite this important discovery, Walker’s Southern Oscillation and the Peruvian fishermen’s warm current remained unconnected in scientific circles for several decades.

It was not until the late 1960s that Norwegian-American meteorologist Jacob Bjerknes linked these phenomena. Bjerknes demonstrated that the ocean warming off South America and the atmospheric pressure oscillations across the Pacific were interconnected components of a single coupled system.

He named the atmospheric circulation loop the “Walker Circulation” in honour of Walker’s pioneering work. This integration gave rise to the term El Niño-Southern Oscillation (ENSO), which today forms the foundation for monitoring and understanding the phenomenon.

Currently, El Niño events are tracked using the Oceanic Niño Index (ONI), which defines an El Niño as occurring when sea surface temperatures in the central Pacific exceed the long-term average by at least 0.5°C for five consecutive overlapping three-month periods.

Events are classified as “Super” or “very strong” when anomalies exceed approximately 2°C, thresholds associated with significant global climatic and economic impacts.

The economic impact of El Niño

The magnitude of potential economic disruption becomes apparent when we examine the costs associated with previous super El Niño events.

A 2023 study published in the journal Science analysed two particularly intense episodes that occurred in 1982-83 and 1997-98, finding that the resulting changes in weather patterns caused global income losses of $4.1 trillion and $5.7 trillion, respectively. It is likely to reach $84 trillion by the end of this century. These costs manifested primarily through damages from extreme weather events, including lost agricultural output owing to heat waves, flooding, and prolonged droughts.

The last super El Niño occurred a decade ago in 2015-16, when surface temperatures surged by 2.8°C, creating one of the strongest climate events of the modern era and devastating food security whilst disrupting industrial supply chains worldwide. That event impaired nutrition and food security for some 60 million people worldwide.

The macroeconomic impact of El Niño varies dramatically across economies, determined by their agricultural dependence, fiscal position, and food’s weight in consumer price indices.

Ethiopia leads emerging markets with agriculture representing over 30% of gross domestic product, whilst Nigeria, Pakistan, and Tanzania all exceed 20%. For these economies, sustained weather shocks feed directly into output, rural employment, trade balances, and government revenue.

Pakistan and Nigeria face particularly acute vulnerability, combining high agricultural GDP shares with significant fiscal deficits. An El Niño-driven production shock in these economies simultaneously pressures growth, strains public finances, and transmits rapidly into consumer prices.

This is not the case for lower-dependency markets such as Russia, Poland, and South Africa, which do not rely on agricultural income.

The overall impact depends on local rainfall patterns, heat intensity, crop calendars, starting soil moisture levels, government response capabilities, market conditions, and whether other climate patterns such as the Indian Ocean Dipole reinforce or offset El Niño effects.

Severely impacted commodity markets

The agricultural sector faces particularly acute exposure to El Niño-related disruptions, with production systems across multiple continents confronting weather patterns that deviate substantially from historical norms.

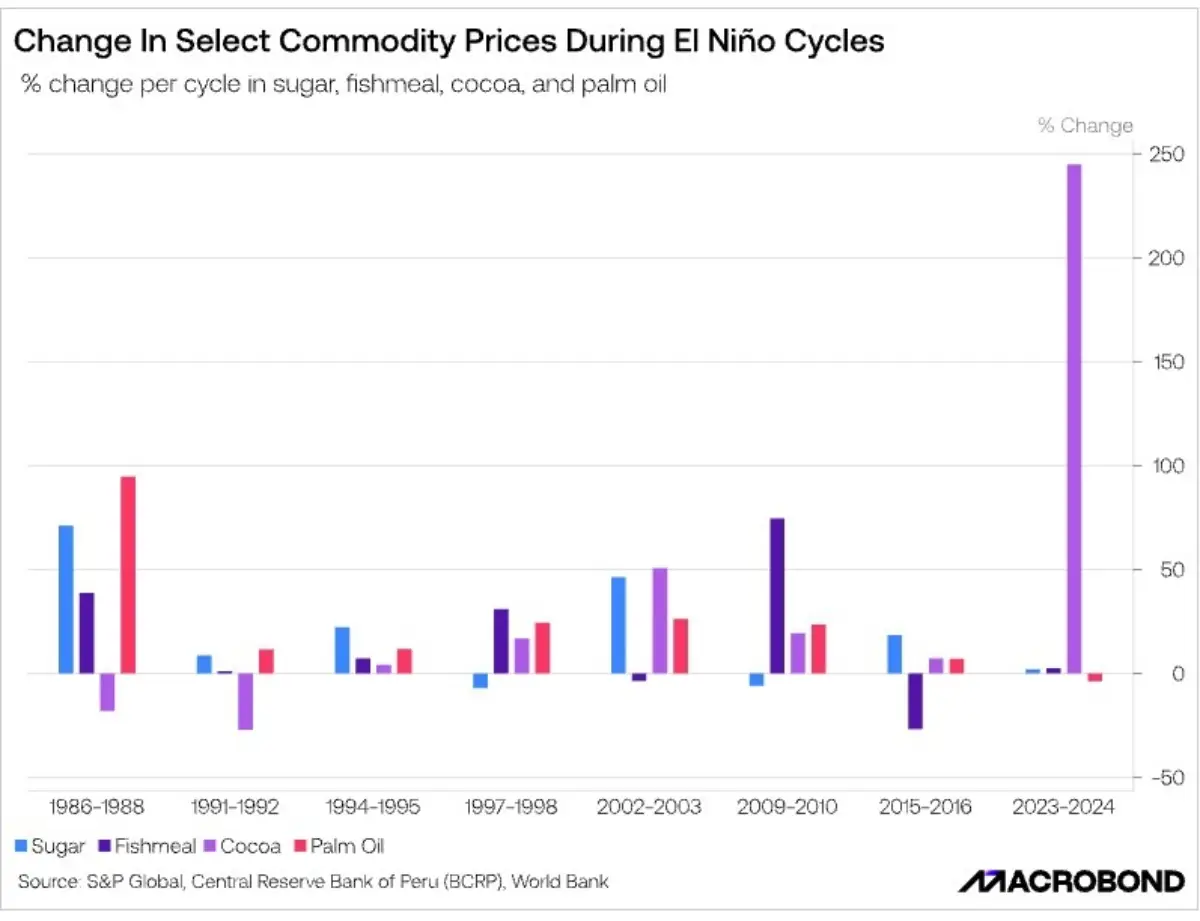

The 2023-2024 El Niño event has produced unprecedented commodity price movements, with cocoa experiencing an extraordinary 250% price increase during the cycle.

However, this escalation cannot be attributed solely to El Niño-related weather patterns. The price surge resulted from a confluence of factors: extreme rainfall in December 2023 causing black pod disease, immediately followed by El Niño-driven drought in February 2024, which struck crops already weakened by ageing tree stock and Cocoa Swollen Shoot Virus following two consecutive below-average harvests.

In terms of select commodities, El Niño’s impact varies when combined with external factors.

Palm oil markets have shown consistent vulnerability across multiple El Niño cycles. Indonesia and Malaysia, which together supply the majority of global palm oil, experienced export disruptions during the 1997-1998, 2015-2016, and 2023-2024 episodes.

Sugar, fishmeal, and palm oil have shown consistent positive price movements across El Niño cycles, though these commodities face multiple independent price drivers beyond climatic patterns.

Palm oil prices respond to Indonesian and Malaysian policy decisions, biofuel mandates, and broader Southeast Asian weather conditions. Fishmeal markets are influenced by Peru’s anchovy quota management and fishing regulations independent of the El Niño Southern Oscillation. Sugar prices reflect Brazilian ethanol policy, Indian export restrictions, and currency movements in the Real.

El Niño typically brings prolonged dry conditions to Southeast Asia, suppressing yields across the oil palm regions of Sumatra, Kalimantan, and Peninsular Malaysia. Any meaningful yield reduction tightens global vegetable oil markets and exerts upward pressure on food prices across import-dependent economies.

Southeast Asia and India, where El Niño typically correlates with below-normal rainfall, face significant risks to crop yields during the current cycle.

Cocoa production in West Africa faces heightened risks in the current cycle, with potential implications for global chocolate prices.

The European Commission published forecasts on 17th June 2026 indicating that several staple crops commonly grown in vulnerable countries, including wheat, corn, and rice, will likely experience price increases throughout the El Niño cycle.

These agricultural pressures occur against a backdrop of existing supply chain stress, with the consequences of a strong El Niño colliding with lingering effects from the Middle East conflict, which has already impacted global prices for agricultural inputs such as fertiliser.

For the current conditions, Malaysia’s economic minister has warned that El Niño could cause crop yields to fall by an average of 8% to 10% this year. Indonesian rice farmers have accelerated planting schedules in an attempt to mitigate the threat of a lengthy dry spell anticipated during the latter half of 2026.

From Panama to Mississippi: The supply chain disruption is real

El Niño-induced weather extremes disrupt transportation infrastructure essential to supply chain operations. Flooding damages roads, railways, and port facilities in regions experiencing above-average rainfall.

The Panama Canal, through which around 5% of global commerce transits, faces operational constraints during El Niño-related droughts that reduce water levels in Gatun Lake, limiting vessel transit capacity and increasing shipping costs.

The waterway has already begun evaluating preventive measures in anticipation of a potentially intense event. A recent update from the Panama Canal Authority projected few material changes to transit volume during 2026, but signalled preparations for operational modifications in 2027, when the effect of El Niño on water levels is forecasted to peak.

The 2023-24 El Niño event demonstrated the vulnerability of this vital shipping route when a prolonged drought in Central America brought water levels in the canal to historic lows. The event forced operators to reduce daily transits from 36 ships to just 25, creating cascading delays throughout global supply chains and elevating transportation costs across multiple sectors.

Drought conditions in major river systems reduce barge transportation capacity for bulk commodities. The Mississippi River system, crucial to United States agricultural exports, experiences reduced navigability during droughts, forcing cargo onto more expensive rail and truck transportation.

Similar constraints affect the Paraná-Paraguay waterway system in South America, which handles substantial volumes of soybeans, corn, and wheat exports from Brazil, Argentina, and Paraguay.

California faces particular exposure to infrastructure disruption during the current cycle. Federal forecasters have indicated that the state will likely experience a wetter, stormier winter with elevated stakes for flooding, infrastructure damage, and volatility in the state’s water cycle.

Southern California and portions of the Central Coast often receive above-normal rainfall during strong El Niño years, raising the risk of urban flooding, debris flows, and dangerous conditions in recent burn scar areas.

Extreme weather events associated with El Niño increase the frequency of port closures, flight cancellations, and road network disruptions. These interruptions create cascading delays throughout supply chains, increasing inventory costs, reducing just-in-time manufacturing efficiency, and elevating the risk of stockouts for time-sensitive products.

Heavy storms associated with El Niño can damage roads, trigger landslides, and slow transportation networks across affected regions. Coastal erosion and high surf events also threaten shoreline infrastructure.

These disruptions translate rapidly into supply chain complications – delays in shipments, port congestion, extended transit times, increased logistics costs, greater exposure of cargo to damage during transport, and potential contractual penalties for missed delivery commitments.

Timber, forest, manufacturing, insurance: The sectoral impact

El Niño’s relationship with forest fires has severe implications for timber supply chains and carbon storage. The two most recent strong El Niño events, in 2015-2016 and 2023-2024, both produced record-breaking fire seasons in Brazil. In both 2016 and 2024, fires burned more than 2.3 million hectares of forest in Brazil, more than four times the annual average from 2001 to 2025.

El Niño tends to reduce rainfall during the wet season in South America, leaving the subsequent dry season even more arid and fire-prone. This pattern proves particularly damaging in the Amazon, where forests are not well-adapted to fire.

The resulting fires cause damage requiring decades to recover from and release enormous quantities of carbon that accelerate climate change, triggering a cycle that renders forests increasingly vulnerable to fire.

The 2023-2024 El Niño contributed to Canada’s warmest winters on record, a thinned snowpack, and dry weather in autumn, leading to the country’s record wildfire season of 2023. El Niño tends to bring hotter, drier summers and reduced winter snowpack to Canada, elevating fire risk across timber-producing regions.

Southeast Asia and Australia face high fire risk during El Niño events, though impacts vary depending on how other climate phenomena, such as the Indian Ocean Dipole, interact with El Niño.

These disruptions affect not only timber supply chains but also paper production, construction materials, and furniture manufacturing networks that depend on the consistent availability of forest products.

El Niño impacts rainfall, causing operational challenges for manufacturing sectors reliant on consistent water supplies.

For example, industries such as semiconductor fabrication, textile production, food processing, and chemical manufacturing require significant water inputs.

Disruptions in water availability lead to production cuts, higher costs, and bottlenecks in global manufacturing networks.

The insurance sector faces mixed implications from the current El Niño cycle. The weather pattern typically reduces the frequency of hurricanes and severe thunderstorms, lowering insurance claims from damages caused by those events. However, this benefit could be offset partially by rising claims caused by increased incidents of wildfires and floods in regions experiencing above-average precipitation.

Pouring hot water into a hot pot

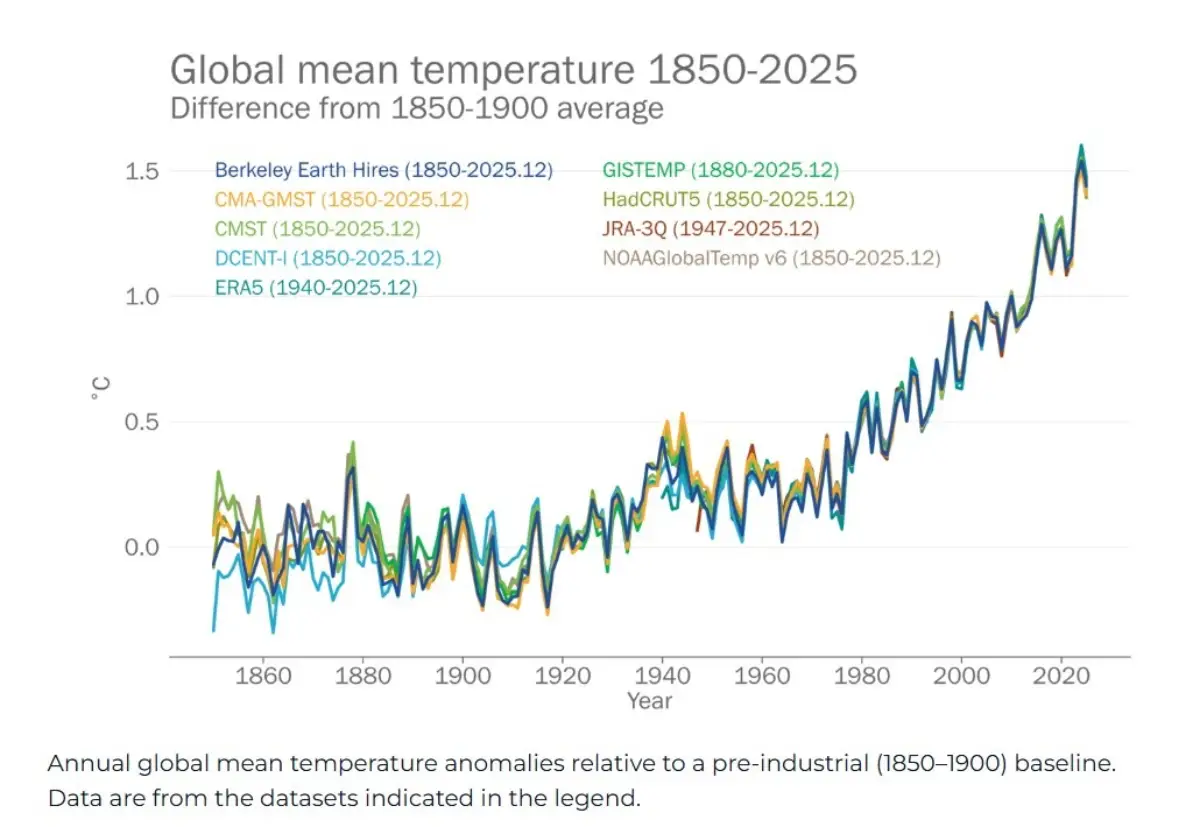

The 2026 El Niño develops against a climate baseline that amplifies the potential severity of impacts. The World Meteorological Organization has warned that the Earth’s climate is further out of balance than at any time in recorded history. The agency reported that the planet is gaining substantially more heat energy than it can release, driven by emissions of warming gases such as carbon dioxide.

The last eleven years were the Earth’s eleven warmest years in records extending back to 1850. In 2025, the global average air temperature was approximately 1.43°C above pre-industrial levels.

This warmer baseline intensifies the damage from identical climate shocks, as higher temperatures increase atmospheric moisture demand, extracting more water from soils and plants, accelerating crop desiccation, worsening heat stress for crops and livestock, and intensifying drought damage even when rainfall deficits match those of past El Niño events.

El Niño timeline and what can be done?

The effects of El Niño on supply chains and consumer prices follow a lagged temporal pattern. Crop disruptions typically require several months to translate into higher retail food prices, though consumers may experience earlier cost increases owing to fertiliser shortages. The World Economic Forum has projected that current fertiliser shortages will require six months to a year to affect food supply fully.

The global economy had been cautiously emerging from the energy crisis triggered by the Middle East conflict, which sent physical oil prices surging to $140 per barrel at one point, their highest level since 2008.

Markets and businesses registered relief when President Donald Trump announced a pending agreement with Iran to cease hostilities and reopen the Strait of Hormuz to ship traffic. However, the formation of a potentially severe El Niño introduces additional complexity to the economic outlook precisely as one crisis appeared to be resolving.

While combating this natural phenomenon is not entirely possible, implementing early warning systems, coupled with flexible procurement strategies and strengthened logistics networks, can help reduce its impact.

Will this El Niño’s (catastrophic) impact remain as consistent as Jerome Powell’s purple tie? Solo el tiempo lo dirá!