By: Scott Sanchon, Trade Treasury Payments

Banking is undergoing a shift from “product-centric” to “customer-oriented propositions”.

A new report from Celent, a research and advisory firm, titled “Enterprise Pricing and Product Management in Banking: Next-Generation Platforms”, finds that traditional product-based models are no longer sufficient in the modern banking system.

The report emphasises a new form of value creation across pricing and product management to maximise customer value. However, traditional banking ecosystems generally operate under a product-centric approach, which limits their ability to deliver personalised experiences.

These increasing influences on customer expectations pressure fintechs to evolve toward enterprise-wide pricing models. Next-generation platforms introduce a core mechanism that enables banking systems and customer engagement to emerge, and enables banks to manage products more effectively. Technologies such as cloud-native architectures, APIs, and AI are enabling dynamic personalisation while optimising operations and increasing profitability.

The concept is not new, and there has been renewed interest across the banking sector (both retail and corporate) in enterprise pricing over the 2020s, driven by several factors. New models such as Banking-as-a-Platform and subscription pricing have been widely adopted across industries. Regulatory attention is shifting to ensuring that the value delivered is reflected in customer-level pricing.

In parallel, next-generation architecture, such as APIs, low-code platforms, and a shift to composable platforms, has changed the dynamics of usable capabilities while ensuring alignment in operations across existing systems. Enterprise pricing and product management not only enable banks to enhance innovation and foster efficiency, but also give them greater control and visibility into the business.

Source: Celent (2026), p. 5

The triple win: Experience, growth, efficiency

Across banking operations, enterprise pricing and product management platforms deliver significant value. These platforms, according to the Celent report, enhance the customer experience by enabling personalised pricing and bundled offerings, improving onboarding efficiency, and reducing disputes. Clearer fee structures and customer-focused pricing also drive revenue growth through relationship-based pricing, enabling banks to design their products to align with customer value and reduce revenue leakage. These technological changes translate to a “triple win” by improving customer experience, increasing revenue, and enhancing efficiency and compliance.

Beyond these benefits, the new generation of fintech landscape has expanded across the banking industry. Platforms such as Oracle, SunTec, and Zafin have been dominating the market. However, new core providers, such as core banking, telecom firms, and pricing specialists, are emerging in the market, offering banks a wider range of options to improve efficiency.

AI and analytics are key forces that orchestrate these shifts. Cloud-native and microservices-based architectures are great examples of emerging systems that improve scalability and flexibility. Low-code and no-code tools further fuel agility by enabling business users to configure pricing without relying on IT. Platforms are also shifting from traditional pricing tools to revenue management systems, enabling banks to design and manage products across entire ecosystems.

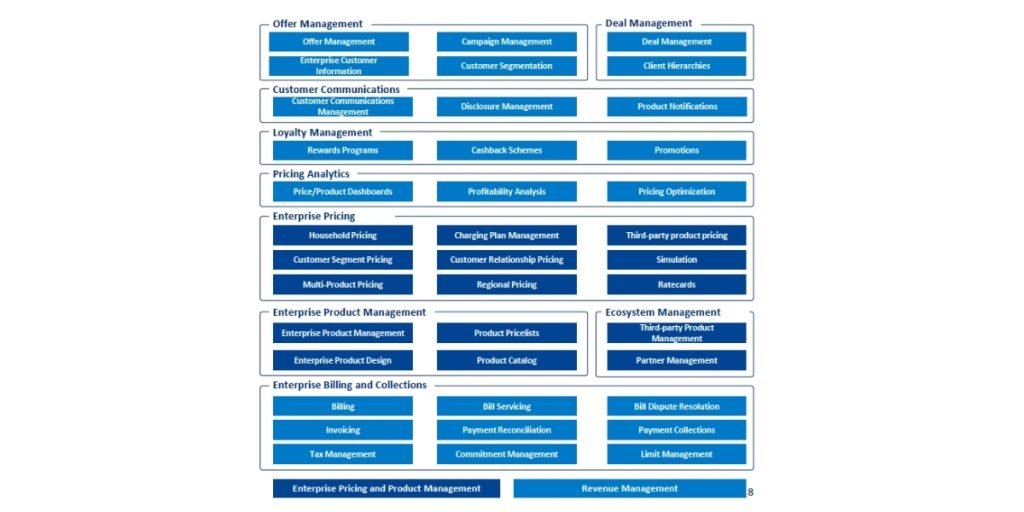

The distinction between enterprise pricing and product management in corporate and retail banking

Customer needs define the distinct nature of enterprise pricing in retail and corporate banking. This diagram from the Celent report shows enterprise architecture mapping of key functionality areas that typically form part of vendor enterprise pricing and product management platforms, as well as broader revenue management.

Source: Celent (2026), p. 8

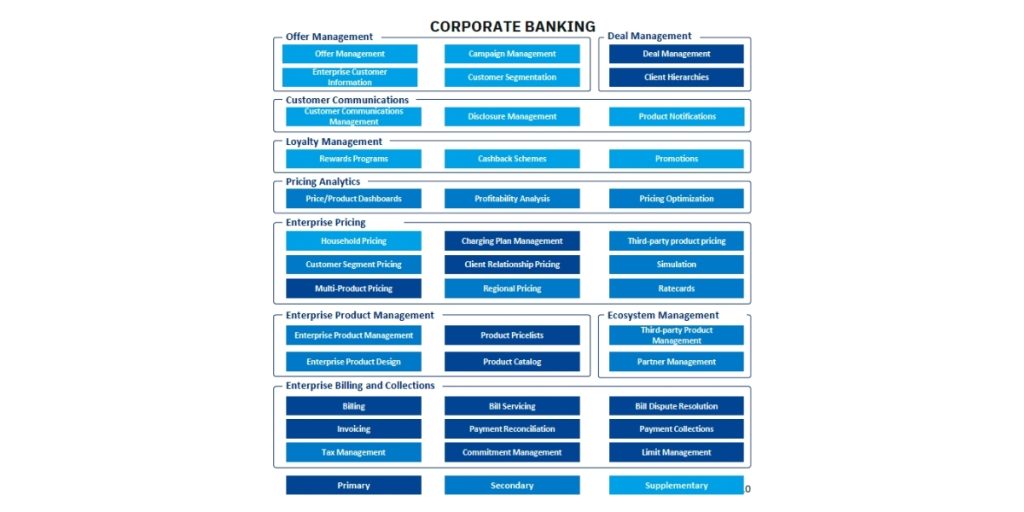

In the retail space, it often comes with limited variations based on customer segments or product types. Enterprise pricing platforms in this segment offer products such as loyalty programs, promotions, and customer services.

Source: Celent (2026), p. 9

From a different perspective, corporate banking requires highly personalised pricing models. Pricing in this system is negotiated on a case-by-case basis. Corporations often have multi-layered pricing structures, which are more complex and require customisation. For example, a corporate client may have pricing structures based on transaction volumes and contractual commitments, whereas another firm may rely more on account balances.

Source: Celent (2026), p. 10

For banks, recognising these key differences is a foundation for implementing enterprise pricing solutions. Choosing an approach is subjective. Strategic priorities that align with the institution’s business model are essential to drive successful enterprise pricing solutions.

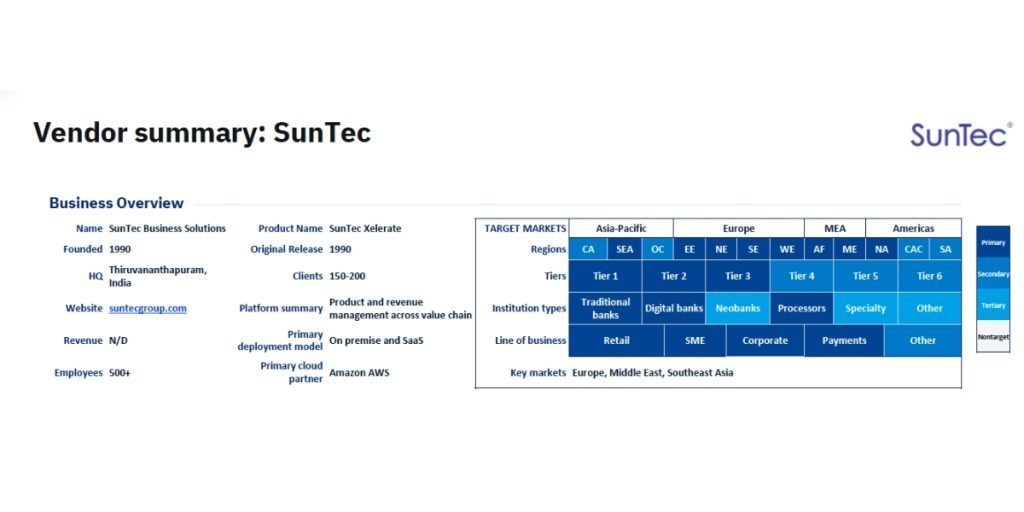

SunTec Xelerate: A next-generation platform example

Source: Celent (2026), p. 18

SunTec Xelerate offers end-to-end revenue management platforms, including product catalogue management, billing, taxation, e-invoicing and loyalty programs on a cloud-agnostic architecture. One of its key strengths is scalable relationship-based pricing that can compute charges for transactions based on multiple attributes and conditions associated with an entity profile. This service allows banks to calculate charges, transaction data, and service usage that support advanced features such as deal management and offer management.

Furthermore, SunTec Xelerate also leverages low-code/no-code configurability to enable rapid customisation, as well as an augmented AI layer that automates complex processes and provides context-specific insights to assist bank users.

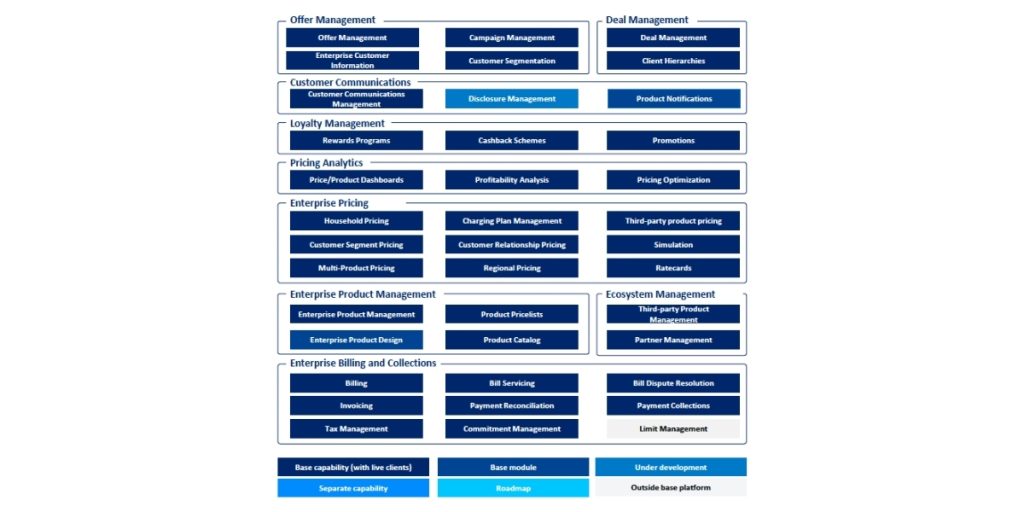

Functional Differentiators

According to Celent’s evaluation, SunTec Xelerate stands out for its breadth of functionality, particularly in corporate banking, where it has been recognised as a “Luminary” platform. The platform’s ecosystem allows banks to manage revenue lifecycles across functions. Its integration, such as framework (XConnect), enables connectivity with current banking systems, CRM platform and other third-party services, also making it a strong choice for banks seeking end-to-end product management solutions.

Source: Celent (2026), p. 19

The Celent report demonstrates the growing importance of enterprise pricing and product management in the banking industry. The Next-generation platforms provide the tools needed to transform towards customer-centric pricing and operational efficiency. With advancements in cloud computing, enterprise pricing solutions are becoming a strategic pillar of modern digital banking.

The competition and new customer expectations pressure banks to offer more flexibility and a customer-focused experience. Ultimately, the transformation requires banks to be better positioned to innovate, comply with regulations, and strategically approach new technology to maximise opportunities.