Export credit agencies are often described as the scaffolding of global trade, but in Africa, they have become a test of political will. A comparative study of non-African ECAs, submitted in 2023 and recently published, highlights two very different models.

UK Export Finance was positioned as an example of a more proactive, strategic approach.

Euler Hermes was used as a contrasting case, reflecting a more cautious and risk-averse stance. The intention of the research was not to single out any one institution but to show how strategy, presence and product design shape outcomes in practice.

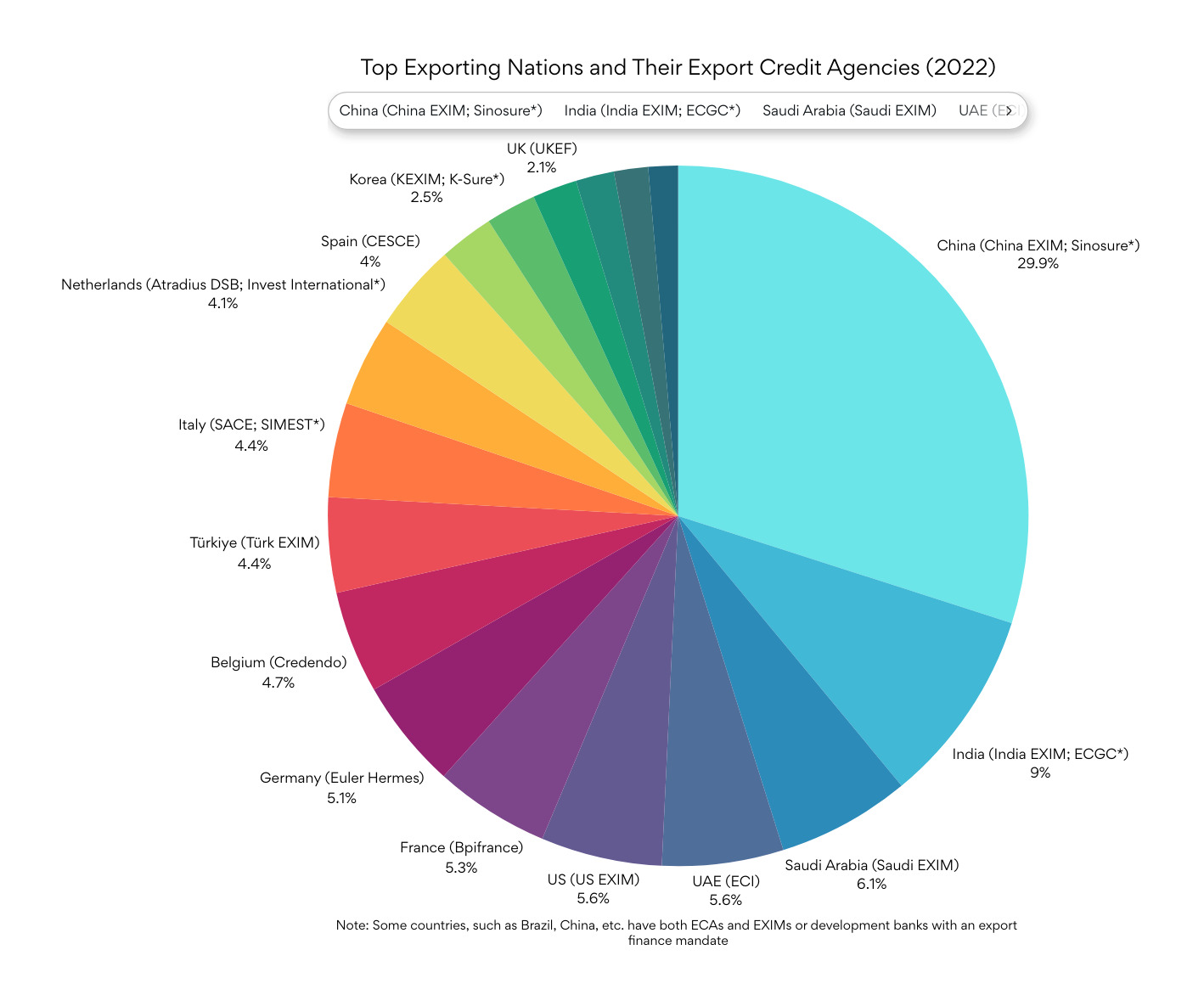

The stakes are significant. Africa faces a trade finance gap of between 80 and 120 billion dollars each year, even as the African Continental Free Trade Area (AfCFTA) promises to redraw routes and integrate markets. ECAs can either help narrow that gap or entrench it. The study led by Andreas Klasen, Alexander Koldau, and Roseline Wanjiru demonstrates that success depends on three elements.

- Clear strategic direction

- Visible presence in market

- Fit for purpose lending and insurance products.

Co-author Roseline Wanjiru, Head of Strategy Group at Newcastle Business School, Northumbria University, and Senior Fellow at the Lill Institute for Public Value, highlights that “the case of UKEF shows what an alignment of strategy, people on the ground and proactive lending can unlock – where cover is pared back and loans are absent, exporters face higher barriers.” Since 2018, UKEF has treated Africa as a priority, stationing executives in five countries to originate deals and run supplier fairs while feeding intelligence back to London. Its cover ratios reach up to 95 per cent without systematic reductions for African markets. And unlike many peers it has been willing to provide direct loans where commercial banks hesitate. The effect has been to create more level competition for British exporters, particularly in sectors such as machinery and equipment.

The contrasting case is one of caution. Euler Hermes, in the period studied, applied lower cover ratios in some African markets and lacked direct lending authority. Its presence on the ground was limited. For researchers, this illustrated the risks of an ECA framework that leans heavily on subsidiarity and relies on others to assume the first layer of risk. Exporters in such a system may face higher barriers when entering riskier markets. Co-author Andreas Klasen, Director at the lill Institute for Public Value: “Recent developments, such as the establishment of a new presence by Euler Hermes in Côte d’Ivoire, are encouraging and highlight a key finding of our study. In Africa, local presence is policy. Risks can fall while opportunities arise.”

Both approaches raise important questions. UKEF’s activism exposes fragile sovereign balance sheets and has drawn criticism that its programmes can favour large contractors over local value chains. More cautious frameworks risk marginalising exporters altogether. The lesson is not that one is right and the other wrong, but that the design of mandates matters.

Table 1: Countries with highest export volumes in Africa and respective ECAs/EXIMs

Source: Adapted from: Klasen, Koldau & Wanjiru (2025), Journal of Entrepreneurship and Public Policy

Context from outside the study reinforces this. Berne Union members recently flagged growing concern about African sovereign risk, citing Senegal’s downgrade.

Yuichiro Akita, Berne Union President, told TTP, “Africa is a market of vast potential, offering significant infrastructure investment opportunities in energy, transport, communications, and healthcare, as well as in the mining sector—including critical minerals—where advancement along the value chain is pursued.

It remains an important market for BU members in the medium to long term. Each ECA, shaped by its own institutional framework and geographic or historical context, naturally adopts a different strategy toward Africa—there is no absolute right or wrong. However, a shared challenge lies in reassessing each institution’s risk appetite while effectively mobilising private capital through collaboration with MDBs, DFIs, PRIs, and other partners.”

George Wilson, CEO of the ARM Africa Trade Finance Fund, added, “It is somewhat surprising that, in light of the UN’s recent Sevilla Commitment advocating for innovative public-private blended partnerships to mobilise finance for sustainable development in regions like Africa, not all European ECAs have responded with greater enthusiasm and adaptability.”

Multilateral development banks have shown that balance sheets can be stretched through guarantees and risk transfers, mobilising multiples of their paid-in capital while maintaining AAA ratings. And the private credit and political risk insurance market is pivoting away from broad sovereign cover toward sector and project-specific underwriting in markets such as Morocco, Namibia and Zambia. ECAs should note these shifts. The demand is there, but risk must be managed with greater precision.

The broader question is whether governments are willing to use export credit with imagination and accountability. It is not the only lever. Africa’s financial future will also depend on stronger local banks, regional insurers, MDB capital and blended structures. But it is one of the few tools policymakers can control directly. Where ECAs are strategic, present and flexible, they can enable new trade and create jobs. Where they are absent, the field will be left to others.

As AfCFTA advances and climate commitments sharpen, ECAs in Africa will be judged not by the size of their portfolios but by whether they generate sustainable trade, durable employment and manageable debt. The research points to what works. The challenge now is for governments to adopt those lessons, wherever they sit, and to apply them with urgency.