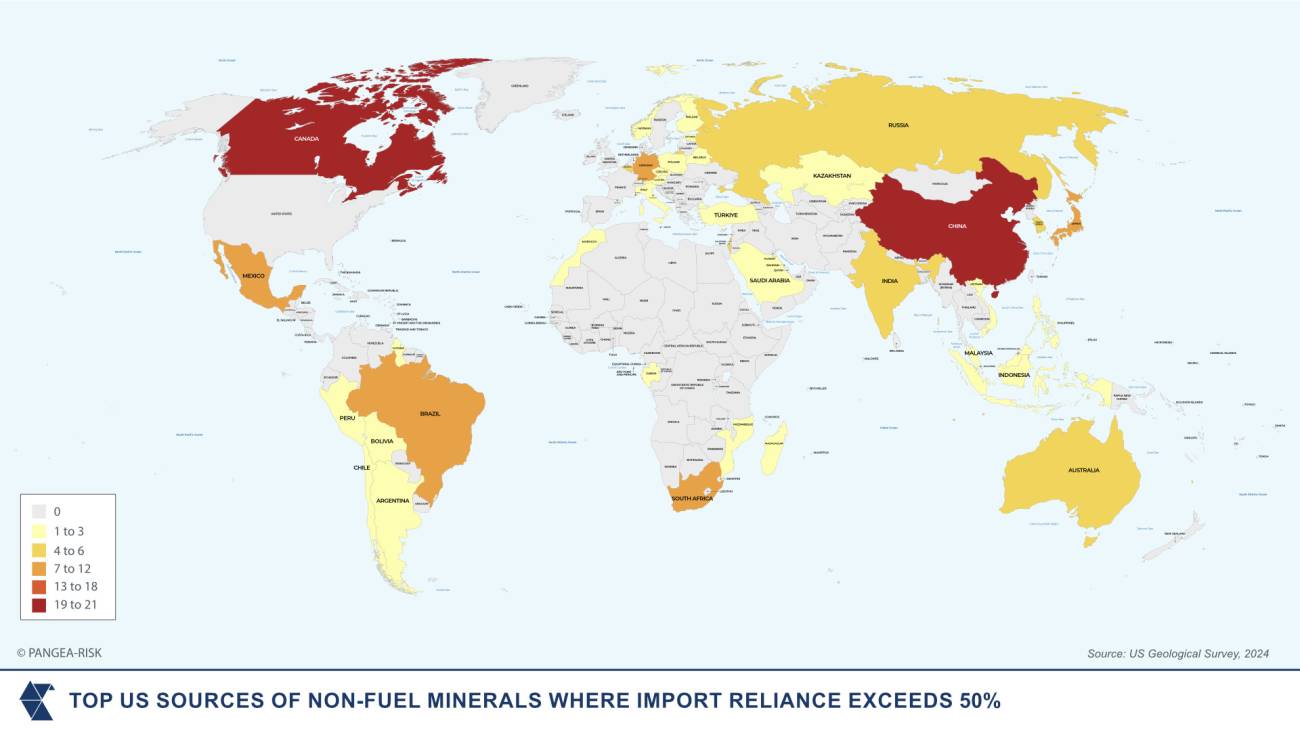

Under US President Donald Trump’s administration, critical minerals have become tools of transactional diplomacy, with bilateral deals tied to security, access, and political alignment, exemplified by proposed agreements with Ukraine and the DRC. The US is increasingly relying on Gulf states to close financing and processing gaps in its mineral strategy, with the UAE and Saudi Arabia expanding their roles in the global supply chain. Resource-rich governments in Africa and beyond are leveraging heightened demand to renegotiate terms, assert control over exports, and extract greater economic and political value. (box)

Since United States (US) President Donald Trump was inaugurated in January, a series of executive and foreign policy actions have placed his objective of “restoring America’s mineral dominance” at the centre of the new administration’s agenda. These include efforts to compel Ukraine to grant access to its mineral and energy assets as a condition for continued US support in the war against Russia, and renewed interest in securing control over mineral resources in Greenland. The administration has also issued executive orders seeking to expand domestic mineral production and processing, eroding due diligence requirements in the financing of foreign mining projects, and suspending anti-bribery provisions to secure what it terms “strategic business advantages” in the international minerals market.

For African mineral-producing countries, the evolving global political environment introduces both elevated risks and prospects of enhanced leverage. Whereas competition over mineral access has traditionally been shaped by intersecting economic and national interests, the present posture of the US government reflects a more explicitly transactional orientation. Several African governments are already adapting to this recalibrated environment. Amid an ongoing offensive by M23 insurgents in its eastern provinces, the government of the Democratic Republic of the Congo (DRC) has explored an arrangement with the US involving the exchange of mineral access for security assistance.

PANGEA-RISK assesses President Trump’s mineral diplomacy, Gulf state integration into US supply chain strategy, Africa’s evolving bargaining power, and rising state control over mineral production.

Trump’s mineral diplomacy

The Trump administration’s pursuit of foreign mineral access has amplified a transactional mode of engagement in global resource politics. Critical minerals, now central to both security and industrial agendas, are increasingly framed not only as commodities but as bargaining tools. The unresolved case of Ukraine reflects the broader fragility of this approach.

Following the collapse of a proposed critical minerals agreement between the US and Ukraine during a high-profile diplomatic breakdown in February, both parties have expressed willingness to renegotiate. The draft framework envisaged the creation of a jointly managed fund drawing on future revenues from untapped natural resources, excluding Ukraine’s existing state-run energy entities, such as Naftogaz and Ukrnafta. Ukraine’s contribution was set to derive from new ventures, backed by foreign investment. However, the viability of this framework remains uncertain. Much of Ukraine’s infrastructure has been damaged during the ongoing fighting, reducing national power generation to approximately one-third of its pre-conflict capacity.

Compounding this is the absence of accurate geological data. Ukraine’s most recent comprehensive mineral surveys were conducted between 30 and 60 years ago under Soviet administration, using methods that are now outdated. Without verified reserve estimates or modern assessments, attracting the scale of investment required, estimated between USD 500 million and USD 1 billion per mine, is unlikely. Even where deposits are confirmed, the global development timeline for a mine averages around 18 years. The Trump administration’s expectation of short- to medium-term strategic returns therefore faces clear temporal and financial constraints.

The minerals initiative with Ukraine is not isolated. Similar overtures have been directed at Greenland, Canada, and Russia. However, a parallel case has emerged in Africa. The government of the DRC, facing insecurity in its eastern provinces, has approached the US with a proposition to exchange access to critical mineral reserves for security support. The offer echoes the structure of the Ukraine proposal, revealing a pattern in the Trump administration’s external engagements: states facing acute security threats are implicitly encouraged to commodify resource access as an entry point for bilateral support. This creates a model of transactionalism, where political and military cooperation are increasingly conditioned on resource-linked reciprocity.

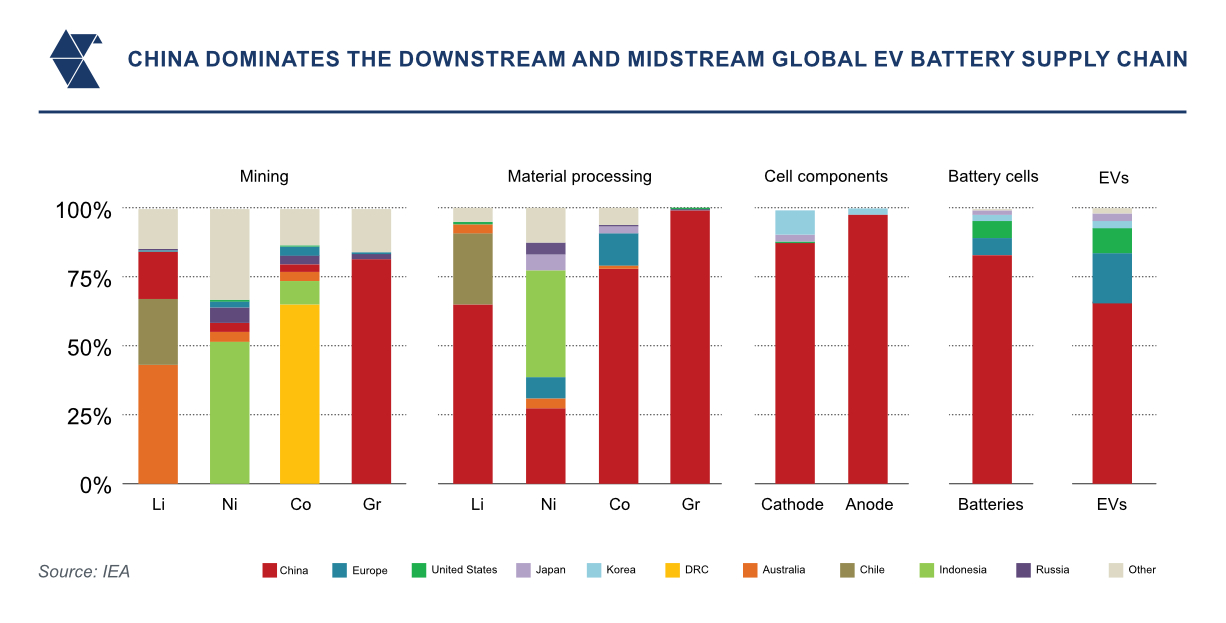

Yet, even if raw minerals are secured, the US remains constrained by its limited processing capacity. Both the Trump and Biden administrations have acknowledged China’s market dominance in refining and processing critical minerals, a bottleneck that undermines the strategic value of raw material access. To date, investment in domestic US processing facilities has not altered the global distribution of refining capabilities. The current asymmetry leaves any sourcing strategy exposed to external dependencies.

The Ukraine case, when viewed alongside the DRC’s proposition and broader US ambitions, illustrates a pivot in foreign resource engagement. However, this model is constrained by its reliance on unstable partners, underdeveloped infrastructure, and deferred returns. Without parallel investment in processing capacity and a departure from improvised bilateralism, the transactional model risks delivering volatility instead of resilience.

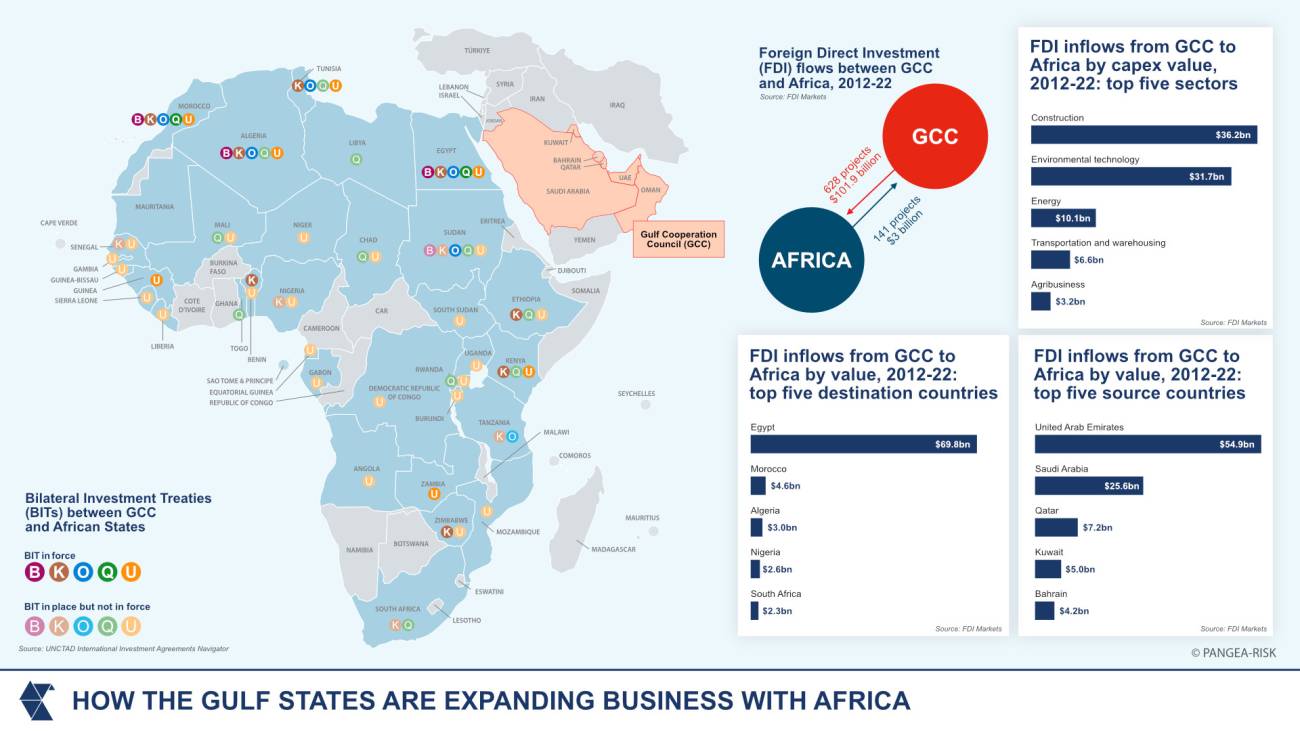

Gulf to play pivotal role in US minerals strategy

The US is increasingly using Gulf states as pivotal enablers in its effort to restructure global mineral supply chains away from Chinese dominance. While domestic US initiatives such as the Inflation Reduction Act and the CHIPS and Science Act seek to stimulate internal capacity, these are insufficient to meet current demand, particularly in mineral processing. The growing involvement of Gulf states in critical mineral value chains offers the US access to capital, logistics capacity, and emerging industrial capabilities aligned with “friendshoring” imperatives.

Gulf Cooperation Council (GCC) countries are advancing long-term strategies to integrate into global critical mineral networks. The United Arab Emirates (UAE) and Saudi Arabia have taken distinct yet complementary approaches. The UAE is leveraging its existing industrial base, including a large aluminium sector, and abundant, affordable energy to develop domestic processing capacity. State-owned Emirates Global Aluminium anchors this industrialisation strategy, while the government targets a five percent contribution from mining to non-oil gross domestic product by 2030.

In parallel, the UAE is mobilising capital through joint ventures such as the USD 1.2 billion partnership between Abu Dhabi’s ADQ and Orion Resource Partners. This venture will focus on securing upstream assets, with initial investment in Morocco’s copper sector, and an openness to midstream investments in processing infrastructure. The UAE’s geographic positioning, port access, and neutral geopolitical posture enhance its appeal as a strategic logistics and refining hub.

Saudi Arabia’s approach is grounded in the exploitation of its untapped domestic reserves, estimated at USD 2.5 trillion. The kingdom is expanding its mining sector through both public and private channels, including state-owned Ma’aden and its joint venture with US-based Ivanhoe Electric to explore the Arabian Shield region. The Public Investment Fund’s vehicle, Manara Minerals, is actively acquiring international mining assets. Concurrently, Saudi Arabia is attracting midstream capital, exemplified by Vedanta’s USD 2 billion copper smelting and refining commitment.

The alignment of Gulf capital with US strategic objectives is accelerating through investment structures that prioritise long-term returns over short-term profitability. Unlike commercial investors in the West, Gulf sovereign entities exhibit greater tolerance for risk and longer return horizons, positioning them as suitable partners in early-stage mining ventures that traditional markets avoid. Gulf participation also offers the US alternative routes for financing projects currently exposed to Chinese influence or state-backed competition.

Geopolitical alignment remains a conditional factor. While President Trump maintained strong personal relations with regional leaders, recent developments such as proposals to annex Gaza have introduced political sensitivities that could constrain cooperation. Nevertheless, Trump’s transactional approach to foreign policy, demonstrated in the draft USD 1 trillion US-Ukraine critical minerals agreement, aligns with the Gulf states’ interest in linking investment to strategic outcomes. Gulf capital could enter the Ukrainian minerals sector if conditions align, reinforcing cross-regional mineral diplomacy and further embedding the region in global resource governance.

As Gulf actors increase their exposure to Africa and Latin America’s mineral reserves, their capacity to serve as intermediaries in global supply chain restructuring will expand. Their engagement is not merely financial. It reflects a structural shift in global mineral geopolitics, where financial capability, processing potential, and geopolitical neutrality collectively confer strategic relevance.

Africa’s growing bargaining power

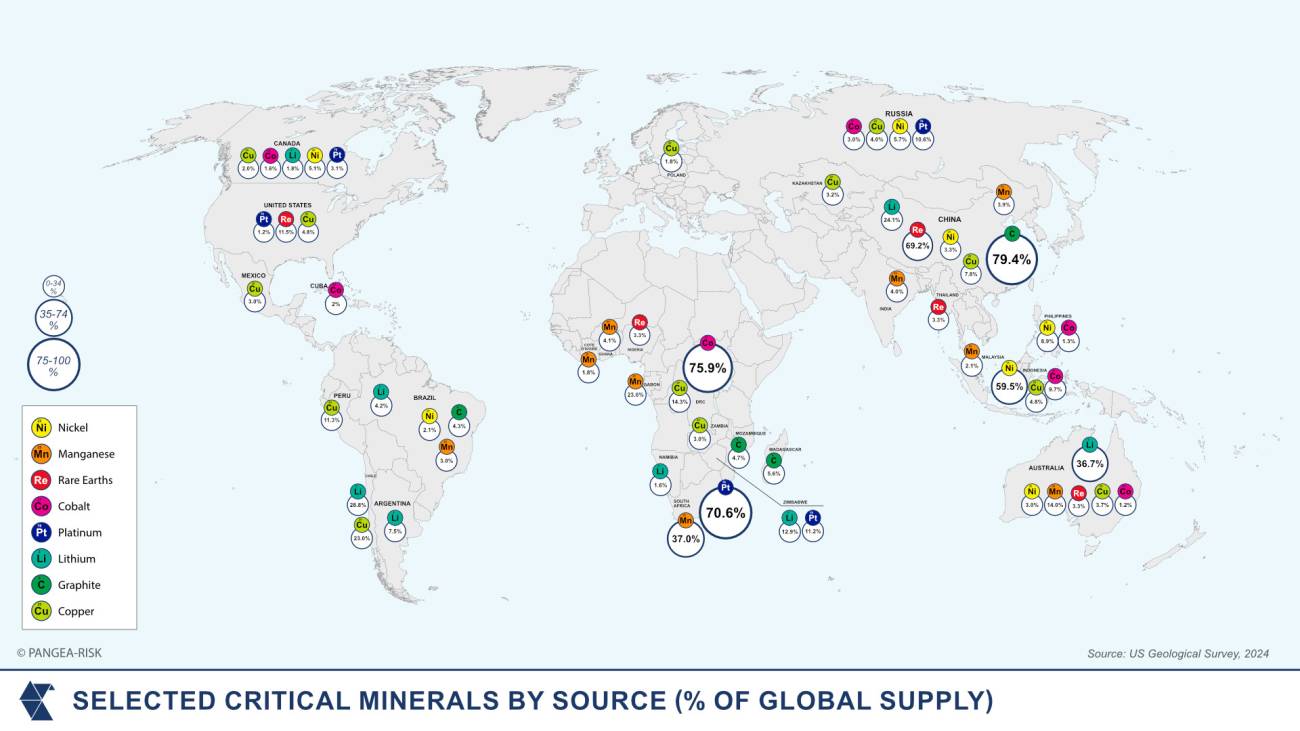

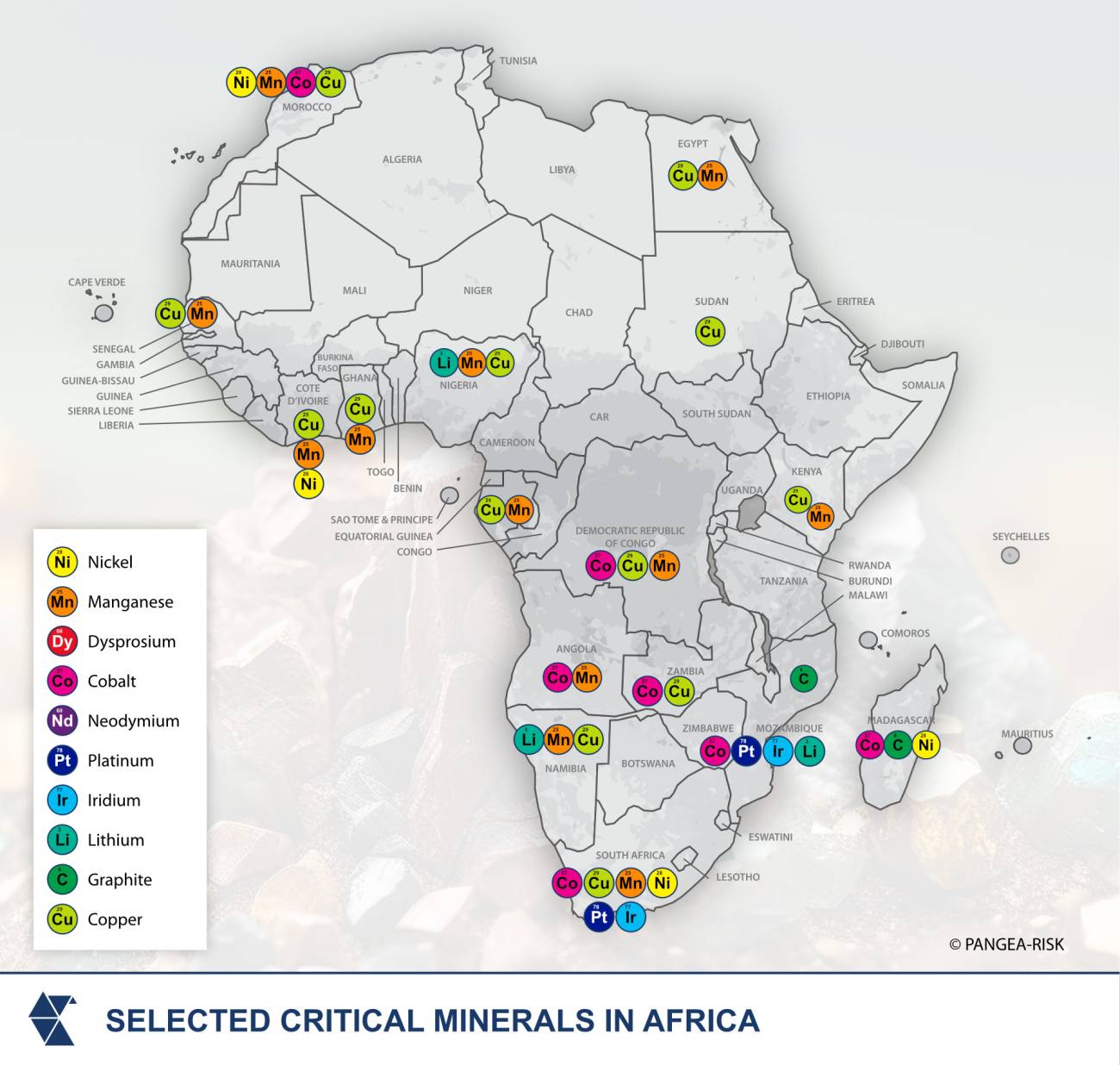

Africa’s mineral wealth is once again attracting external interest, but this iteration diverges from the past. With at least one-fifth of the world’s reserves of minerals critical to the energy transition, such as cobalt, lithium, and rare earth elements, African states are navigating an international landscape shaped by US efforts to counter China’s entrenched dominance in extraction, processing, and infrastructure. This dynamic is amplifying Africa’s bargaining power, but its durability will depend less on diplomatic choreography and more on structural policy readiness.

The US has framed its re-engagement with Africa’s mining sector around the mobilisation of public finance to catalyse private capital. The US International Development Finance Corporation (DFC), created under the Trump administration, has become the primary instrument of this effort. Its portfolio includes projects such as a graphite mine in Mozambique and, more recently, authorisation to invest in domestic mineral ventures. Nonetheless, the scale remains limited. As of late 2023, the DFC’s cumulative investments in mining projects stood at only USD 270 million. This compares unfavourably with China’s overseas mining investments, which under the Belt and Road Initiative (BRI) reached USD 21.4 billion in 2024 alone.

Beyond the DFC, other US-backed financing mechanisms are gaining prominence, including Export Credit Agencies (ECAs), which have been tasked with assuming greater risk exposure in resource-linked ventures. However, ECAs remain under scrutiny due to longstanding concerns about environmental and social safeguards. Even where financing is on offer, project implementation remains vulnerable to political interference, regulatory opacity, and infrastructure shortfalls, particularly in jurisdictions where the investment climate is undermined by erratic taxation frameworks and unresolved governance risks.

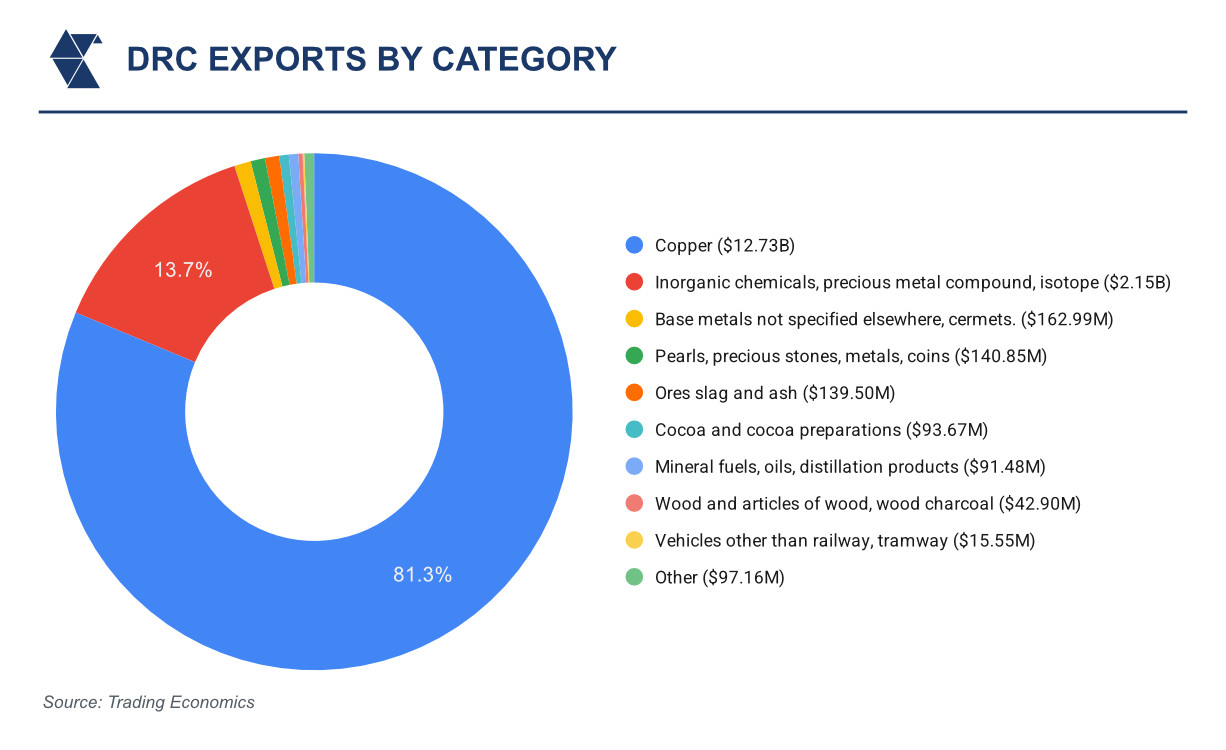

Nonetheless, some African governments have demonstrated an ability to use this moment to extract improved terms. Botswana renegotiated its longstanding agreement with De Beers to double the share of diamonds allocated for domestic processing, from 25 percent to a possible 50 percent. The government of the DRC, meanwhile, has moved to restrict cobalt exports, leveraging its dominant market position to exert greater control over the mineral value chain. The DRC has also engaged the US with a proposal linking security support to critical minerals access, echoing older resource-for-infrastructure arrangements such as the Sicomines deal with China.

Such bilateral frameworks are expanding beyond capital flows, encompassing technical cooperation, political guarantees, and operational support such as geological mapping and early-stage infrastructure development. However, outcomes across the continent remain uneven. Despite renewed expressions of interest by Western companies in the DRC, investment inflows have remained constrained due to persistent concerns related to tax policy, corruption exposure, and broader legal uncertainty.

Zambia, through its concurrent engagement with the US, China, and the EU, has adopted a diversified external posture, illustrating how multiple partnerships are being maintained simultaneously. Elsewhere, the durability of external commitments remains in flux, driven as much by investor appetite and domestic policy environments as by geopolitical alignment.

Exerting more control over strategic minerals

Countries that host critical mineral reserves are reasserting control over extraction, processing, and export flows. This trend has gathered momentum over the past few months, coinciding with intensified geopolitical competition over resources. Control measures have become more varied, encompassing fiscal instruments, regulatory frameworks, and structural ownership shifts.

Chile’s move in April 2023 to nationalise lithium extraction through mandated public-private partnerships illustrates how producing states are changing the investment landscape. The Chilean government, now requiring a majority state stake in all lithium ventures, oversees approximately 24 percent of global lithium output. Similar reconfigurations are unfolding across resource-bearing jurisdictions, often tied to broader ambitions to capture more value domestically through localisation of processing and manufacturing.

The DRC, a dominant source of cobalt and a key player in copper and gold markets, has adopted market-shaping measures in recent years. However, renewed conflict in its eastern provinces may disrupt national-level control. Localised actors or regional governments could attempt to assert influence over mining operations, fragmenting state authority and altering contract enforcement dynamics.

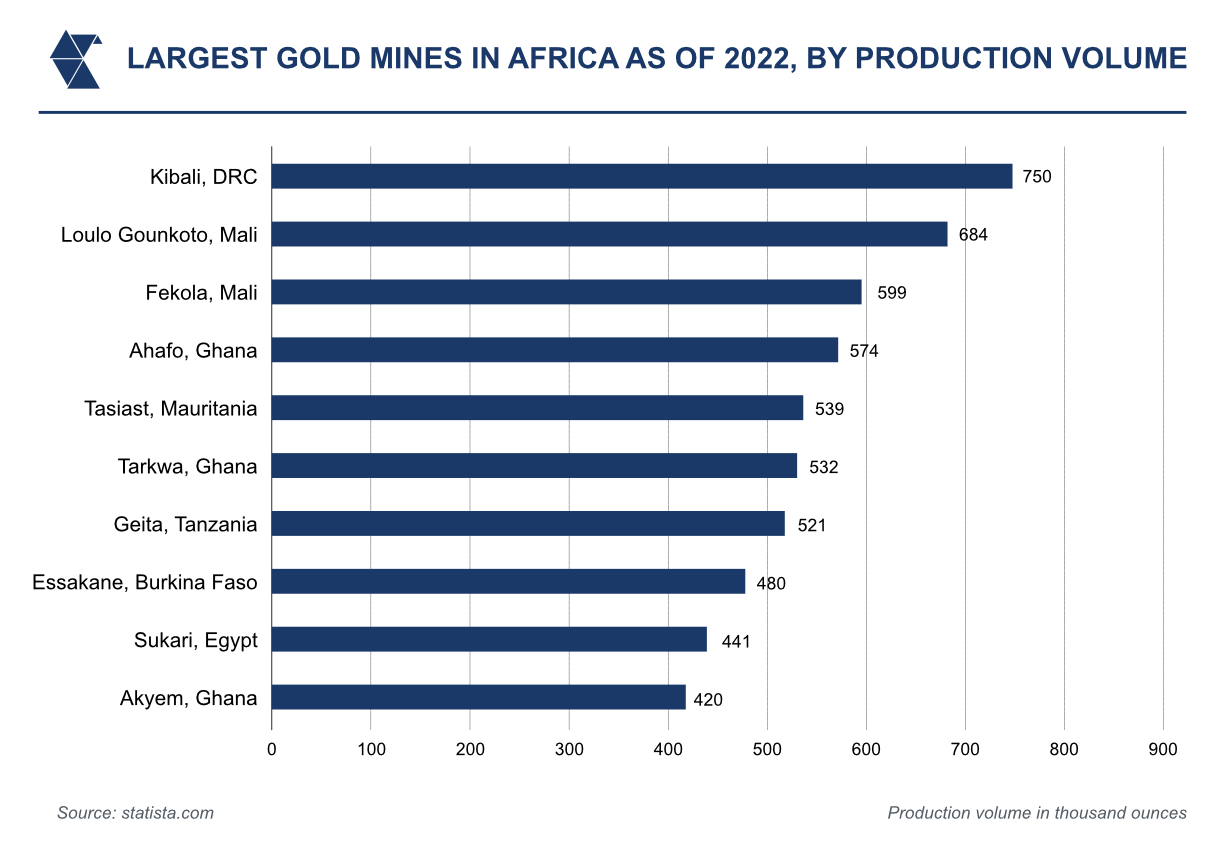

In West Africa, the state of political volatility is increasingly intersecting with resource management. Mali’s seizure of three tonnes of gold in January 2025, amid a dispute with Canada’s Barrick Gold, underscores the legal and operational uncertainty facing mining firms. The incident has shifted investor risk perceptions, especially as Mali’s share of global gold production – currently two percent – is now taking place in a context where the share of gold output originating from high-risk jurisdictions has risen from zero in 2016 to 18 percent in 2024. These trends have implications not only for gold’s supply chain but for its function as a financial safe haven during periods of macroeconomic instability.

This assertiveness is not confined to African or Latin American states. China and the US, central actors in current geopolitical rivalries, have both introduced mineral-related trade restrictions and defensive stockpiling policies. China has curtailed exports of gallium, germanium, and antimony, while the US has advanced plans to diversify its supply chain, including reviving domestic mining initiatives and exploring new acquisition targets.

As resource nationalism intensifies, so too does the variability of supply conditions. Countries are introducing value-capture strategies, ranging from export bans and tax hikes to mandatory local content rules, that affect not only price dynamics but also availability timelines. Producers are adopting dual strategies: asserting control while avoiding binary alignments in the global power competition between the US and China. The concentration of production in a small number of jurisdictions, particularly in the lithium and cobalt sectors, amplifies the impact of any policy shift or disruption, embedding long-term volatility into the critical minerals trade.

Insight

China continues to hold a dominant position across the critical minerals sector, supported by long-term industrial policy and vertically integrated state-backed enterprises. Export restrictions imposed on gallium, germanium, antimony, tungsten, and graphite have introduced structural volatility into global supply chains. These measures serve both commercial and political objectives, allowing the Chinese government to assert control over input costs and influence resource-dependent production in other states.

Attempts by the US and its allies to diversify sourcing and secure alternative supply chains have exposed structural financing limitations. Projections indicate a requirement of over USD 30 billion in capital investment by 2030 to meet demand across aligned jurisdictions. However, private lenders continue to demonstrate reluctance due to long asset maturity timelines, pricing instability, and the perception of uncompetitive cost curves. State-owned Chinese firms are able to operate in high-risk jurisdictions, frequently absorbing losses to maintain strategic positions. This distorts global pricing frameworks and increases cost unpredictability for private-sector competitors.

Export Credit Agencies (ECAs) are being repurposed in response. Rather than supporting export-linked transactions, ECAs in the US and United Kingdom are increasingly mandated to facilitate access to critical minerals through support for import-linked offtake contracts. This reflects a shift in financing models but remains constrained by institutional mandates and risk exposure thresholds. Projects affiliated with Chinese ownership or reliant on Chinese customers are explicitly excluded from eligibility under current ECA mandates in the US.

The Minerals Security Partnership (MSP) – comprising 14 governments, including all G7 members, Australia, India, South Korea, and the EU – has advanced efforts to coordinate financing for mineral access. Early-stage projects have been identified across Africa, Latin America, and Southeast Asia. However, challenges persist due to divergent institutional mandates, differing risk appetites, and limited capacity to structure joint financial interventions. Existing ECA charters, such as that of US Exim, impose portfolio limitations that reduce the flexibility to co-finance with other institutions.

In parallel, several Gulf Cooperation Council (GCC) states are increasing their engagement in mineral value chains. While currently underrepresented in upstream assets, their growing participation in offtake agreements, midstream facilities, and strategic partnerships across Africa and Central Asia positions them as emerging actors in global mineral diplomacy. Their financial capacity, combined with a policy of non-alignment in geopolitical blocs, enables engagement with a wide range of partners across competing supply frameworks.

China’s leverage is further reinforced through bundled investment models, particularly under the Belt and Road Initiative. These arrangements combine mineral extraction rights with integrated infrastructure development, such as power plants, transport corridors, and port facilities, thus embedding long-term economic dependencies. Such models offer recipient governments tangible developmental assets alongside resource monetisation, presenting a value proposition that other frameworks have yet to match in scope, delivery, or cost efficiency.

For the full country outlook, click HERE.