Data access and control facilitate cross-border trade and investment

When it comes to international trade and investment, data is a key driver. Research studies have confirmed that cross-border data flows can promote international trade, with free data flow clauses in trade agreements promoting the growth of goods and services trade between signatory nations. This is partly because increased data flows from a nation reduce uncertainty at a firm level, decreasing the cost of market entry. These economic forces will guide investment and export opportunities away from nations that do not generate and promulgate data and towards nations that do.

Cross-border data flow provisions in bilateral trade agreements are more beneficial to economies with better digital environments. This means nations that have greater access to digital infrastructure and data facilities are likely to attract more foreign investments than those that do not. Conversely, nations or regions without strong digital environments are poised to benefit less from data-sharing provisions since a lack of data infrastructure means they will have less access to and control over their own data flows. Further, any data that is provided will likely be skewed to represent the most digitally active – and thus already most affluent – members of the nation, excluding the most in-need subsections of the population from being represented in the data.

Recent advancements, such as e-invoicing and open banking, are impacting the volume of cross-border data flows. E-invoicing regulations, aimed at combating VAT fraud, and open banking frameworks, enabling real-time access to granular payment flows, are creating trusted digital transaction data sources. These data sources, trusted due to their origin from regulated platforms or direct reporting mechanisms (e.g., France’s regulated e-invoicing platforms), allow innovative lenders to extend working capital even to sub-investment-grade businesses. For instance, open banking enables banks to verify that an invoice has not been funded twice and assess client payment performance.

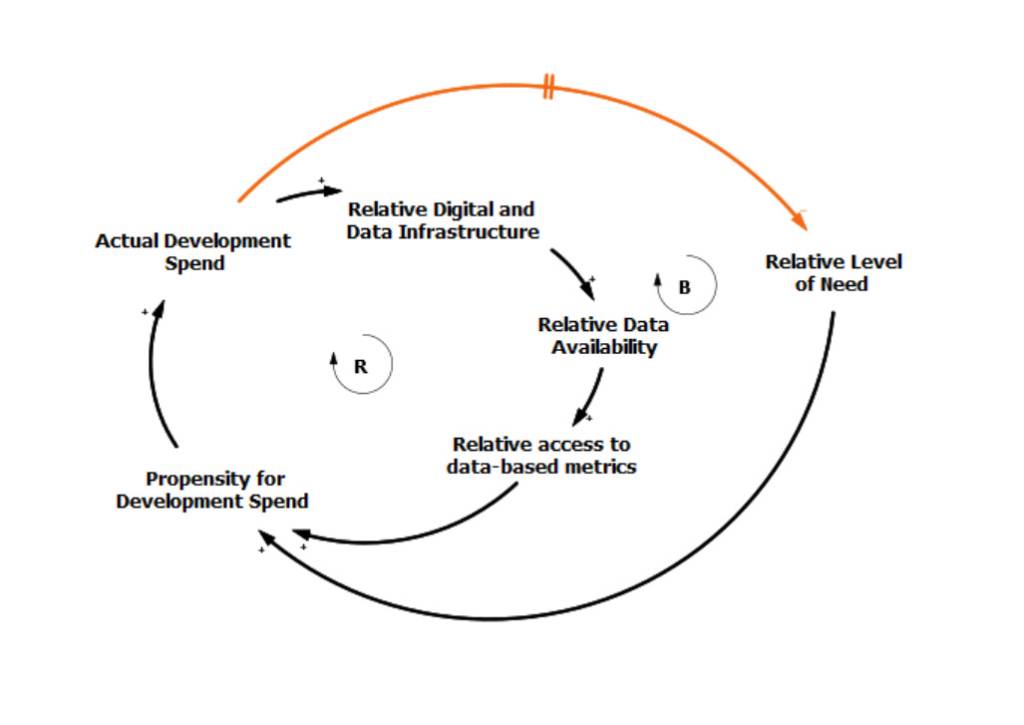

Despite these advancements, nations or regions without strong digital environments remain at a disadvantage. A lack of data infrastructure means limited access to these trusted data flows, further entrenching data inequality. This “scandal of invisibility” can lead to situations where those on the extreme end of the data inequality scale are passed over for desperately needed development aid. Many countries with poor data are trapped in a reinforcing cycle of underdevelopment because funders and organisations prefer to work in areas with a data-demonstrated need and where they can measure the impact of interventions. Limited data leads to limited development aid, which, in turn, inhibits the ability of those nations and regions to develop the data infrastructure needed to attract development aid in the first place. In all, whether it be in the form of limited organic investment and exports or reduced foreign aid, data-poor nations face challenges in the international economy.

Without collaborative efforts, trade digitalisation can exacerbate economic inequality

International trade – a traditionally paper-based industry – is currently experiencing a significant push towards digitalisation. Countless digital trade solutions are being developed, with experts speculating that only outdated and digitally unfriendly legislation in many jurisdictions stands in the way of rapid growth. As with any industry that becomes progressively digitalised, increased trade digitalisation will lead to an exponential increase in the volume of trade data generated. Unfortunately, the low existing data capacity of LDCs means that, in relative terms, the data gains they experience will be lower than what developed economies experience. Since data availability lowers the costs of market entry and increases international trade and investment flows, widespread digitalisation will make international trade and investment relatively more risky and expensive in data-poor nations, incentivising economic actors towards more data-rich and, thus, less expensive environments. Left to market forces alone, this asymmetric data environment can exacerbate worsening global economic inequality.

This lack of data capacity has implications for access to liquidity at the firm level. Financial institutions and credit insurers rely on data about obligors to evaluate creditworthiness and provide risk cover. Typically, originators like banks and trade-focused fund managers prefer to extend liquidity to trade receivables that are credit insured. However, in LDCs, insufficient data on businesses hinders credit insurers from extending risk cover, limiting the working capital liquidity available to these businesses. This cycle underscores the importance of collaborative efforts: regulated data feeds create trusted data sources, enabling credit insurers to engage and increasing the liquidity available to businesses to promote sustained development in their regions.

According to a report from the International Conference on Theory and Practice of Electronic Governance (ICEGOV), “Without collaborative efforts to frame international trade agreements by the international trade bodies and other stakeholders, the data divide in digital trade will become the new face of inequality and create barriers to reaching the agreed 2030 SDGs”.