UK Budget lands with £30bn tightening as trade outlook weakens

UK Budget lands with £30bn tightening as trade outlook weakens

Live Updates

Critical minerals: Budget signals a bigger role for UK finance in energy-transition supply chains

The Budget’s protection of public investment (to the tune of £725bn) has immediate implications for critical-minerals financing, as the UK looks to focus efforts on nuclear, grid upgrades, EV infrastructure, and other industrial corridors.

While the OBR forecasts weaker export growth and a structurally lower trade intensity (around 15% below pre-Brexit baselines) the government’s industrial strategy now leans more heavily on securing inputs for energy transition and advanced manufacturing. This shifts attention back to London’s role as a financing hub for critical raw materials such as lithium, copper, rare earths, nickel, and strategic metals, where supply chains run through Africa, Central Asia, Australia, and Latin America.

Fiscal tightening may have a negative impact on corporate margins, but other measures such as new trade arrangements with India and the US and growing cooperation with the EU create opportunities.

With UK growth slowing to 0.9% in 2026, and the OBR projecting subdued trade volumes, financing upstream and midstream mineral projects is likely to be key for the UK’s productivity and strategic resilience in the years ahead.

The Autumn Budget lands banks and treasury teams in a more delicate operating environment.

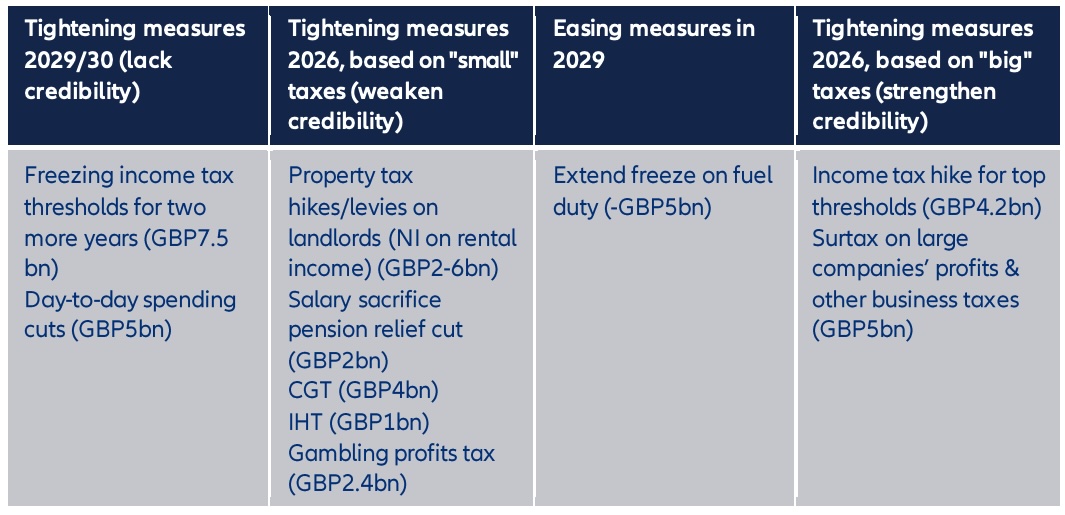

Allianz’s modelling indicates that the government’s reliance on a mix of “small” and “big” tax measures is likely to produce a modest gilt and sterling sell-off, a scenario that increases funding-cost volatility for lenders and corporates alike. With GDP growth expected to slow to 0.9% in 2026, and UK export growth averaging just 0.6% a year from 2026 to 2030, banks are likely to have thinner corporate buffers and increased credit differentiation across sectors.

Treasury desks may need to recalibrate hedging strategies as expected gilt volatility passes through to the swap curve, which would influence pricing across revolving credit lines and cross-border lending facilities. This could cause correspondent-banking networks to see more scrutiny on intraday liquidity, FX exposure, and counterparty limits as sterling responds to fiscal-credibility perceptions through 2026–27.

Credit and political risk insurers are already signalling a pivot in risk appetite following the Autumn Budget’s £30bn tax-led tightening and the OBR’s confirmation of structurally weak UK trade growth.

Modelling from Allianz shows that the government’s choice to lean heavily on “small-tax” measures in 2026 risks creating weaker market credibility and sharper moves in gilts and sterling if macro conditions deteriorate, while mixed “small + big” taxes still result in a modest sell-off across rates and FX.

Source: Allianz ResearchCombined with the OBR’s expectation that UK exports will average just 0.6% annual growth from 2026 to 2030, and that the current-account deficit will sit near 3–3.5% of GDP, insurers face thinner corporate margins and more volatile funding costs.

For the London Market, which underwrites a disproportionate share of global short-term credit limits, trade credit, political risk, and structured trade cover, these conditions are likely to result in higher demand for protection across UK-linked supply chains. This will particularly be the case in sectors like manufacturing, construction, retail/wholesale, commodity-linked SMEs, and import-intensive sectors that are impacted by the removal of low-value duty relief.

With public investment protected and a £725bn infrastructure pipeline maintained, insurers also expect a rise in structured, project-linked submissions as contractors, EPCs, and suppliers seek capacity in an uncertain 2026–27 environment.

The Budget and ensuing response seems to indicate that the UK risk cycle is turning, and credit insurers will once again become a critical shock absorber for companies dealing with tighter liquidity and increasingly uneven cash flows.

Key signals for the credit insurance market

- £30bn tightening, with ~80% of tax measures landing in 2026, raises insolvency and covenant pressure.

- Allianz warns “small-tax only” tightening risks market credibility, increasing gilt and FX volatility (p.3–4).

- OBR forecasts exports rising 3.3% in 2025 but slowing to 0.6% annually thereafter.

- Persistent 3–3.5% current-account deficit heightens sterling and funding-cost sensitivity.

- Removal of low-value import duty relief and changes to business rates increase risk for e-commerce, retail and logistics credit exposures.

- Protected public investment drives increased demand for structured and project-related CPRI/PRI capacity.

Source: Allianz Research

Here are the headline facts from Reeve’s budget

- £30bn fiscal tightening; ~80% of tax rises hit in 2026.

- UK trade intensity forecast to remain ~15% below pre-Brexit baseline.

- Current-account deficit steady at 3–3.5% of GDP.

- GDP growth revised down to 0.9% in 2026.

- £725bn worth of public investment has been maintained.

The UK has officially released it’s much anticipated Autumn Budget, confirming around £30bn of net fiscal tightening, overwhelmingly through tax rises and largely front-loaded into 2026

Markets had expected a tax-led adjustment, but the scale and early timing have surprised many, especially against an OBR outlook that shows UK trade intensity stuck about 15% below pre-Brexit levels, weak medium-term growth, and a current-account deficit hovering near 3–3.5% of GDP.

Public investment, however, has been protected, keeping many infrastructure and industrial-strategy projects alive even as households and corporates will be forced to absorb the higher taxes.