24/7 payments, ISO 20022 adoption, and more: Key trends from the CPMI 2024 survey

24/7 payments, ISO 20022 adoption, and more: Key trends from the CPMI 2024 survey

Live Updates

Cross-border payments don’t happen in a vacuum. They rely heavily on domestic payment systems. Modernising these domestic rails is essential for improving interoperability across borders, says the 2024 cross-border payments monitoring survey conducted by the Committee on Payments and Market Infrastructures (CPMI) at the Bank for International Settlements (BIS), in cooperation with the Financial Stability Board (FSB)

The 2024 survey shows that enhancing domestic payment infrastructures is the foundation for smoother, faster, and more transparent cross-border transactions. But progress isn’t uniform. Different regions and payment systems are at varying stages of development, reflecting diverse starting points and priorities.

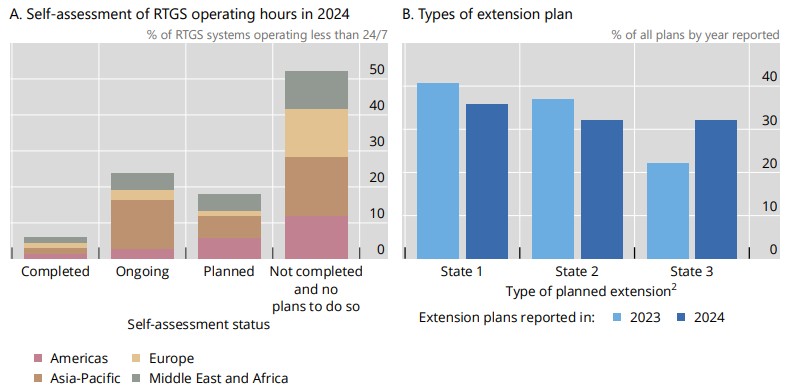

Extending operating hours: The push toward 24/7 payments

One of the standout trends is the growing interest in extending the operating hours of Real-Time Gross Settlement (RTGS) systems. While many systems still operate within traditional business hours, the appetite for 24/7 or near-24/7 operations is noticeably increasing, especially in the Asia-Pacific region.

Why does this matter? Longer operating hours reduce settlement risk and liquidity constraints, enabling faster cross-border payments that align better with global business hours.

The survey shows that nearly half of RTGS systems operating less than 24/7 are conducting or planning self-assessments to extend hours, with some already operating on weekends or around the clock.

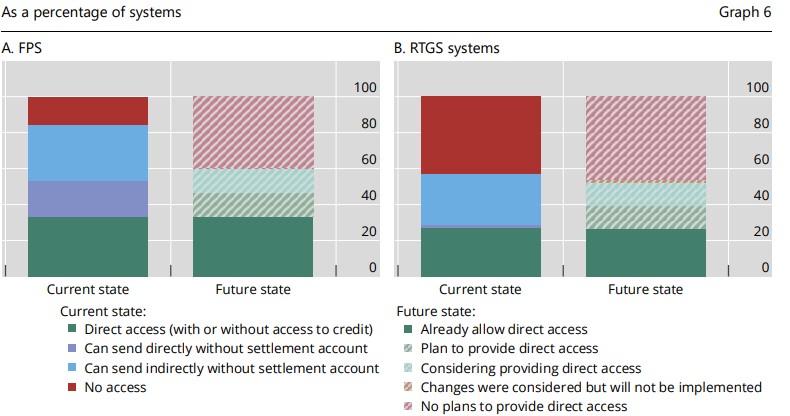

Expanding access: Opening doors to non-bank payment service providers

The survey highlights a significant shift in access policies. Direct access to payment systems by non-bank payment service providers (PSPs) and foreign banks is expanding, though unevenly.

Currently, about 63% of Fast Payment Systems (FPS) and RTGS systems allow foreign banks with a local presence direct access. However, only 14% permit access to foreign banks without a local presence.

Non-bank PSPs are gaining ground more quickly. Roughly one-third of FPS offer direct access, with over half providing direct or indirect access. This is expected to rise to nearly 50% by 2025, driven largely by European systems. RTGS systems lag behind, with only about 27% offering direct access to non-bank PSPs but aiming to reach 40% by 2025.

This expansion is more than administrative; it allows regulated non-bank PSPs direct access, fostering innovation, competition, and cost reduction. It also shortens correspondent banking chains, improving speed and efficiency.

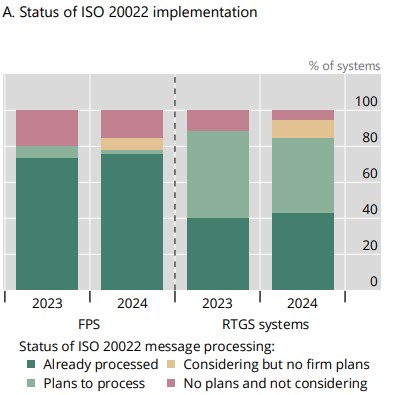

ISO 20022 and APIs: The new language of payments

Fragmented messaging standards have long contributed to friction in cross-border payments. The G20 cross-border payments programme identified this as a key barrier. The growing global adoption of the ISO 20022 messaging standard and APIs promises to change that by enhancing interoperability and data harmonisation.

By the end of 2026, ISO 20022 adoption is expected to exceed FPS adoption, reaching about 83% for RTGS systems. If we include systems that are considering adoption, FPS could reach around 84% and RTGS could approach 94% in the medium term.

Most systems with implementation plans are in advanced stages, such as technical build or participant testing.

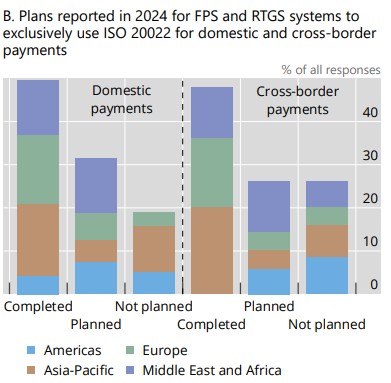

FPS uses ISO 20022 exclusively while RTGS systems often maintain legacy formats like SWIFT messages, given their earlier establishment. Around 78% of FPS and 83% of RTGS systems have fully migrated or plan to fully migrate to ISO 20022 for domestic payments.

For cross-border payments, adoption is slightly lower but still strong, with 72% of FPS and 75% of RTGS systems fully adopting or planning full adoption.

Geographically, about 70% of European payment systems process ISO 20022 messages, with advanced economies leading adoption. Emerging markets and developing economies (EMDEs) are catching up, with many planning implementations. Those without plans are mostly EMDEs in the Americas or Asia-Pacific.

This widespread adoption is a major step toward standardised, transparent, and efficient cross-border payments.

Interlinking payment systems: Models and regional leadership

Interlinking payment systems can improve international remittance and retail cross-border payments. It can benefit wholesale payments through RTGS interlinking.

The survey stated that among RTGS systems, three have bilateral links, nine connect via single access points, and three operate as regional common platforms facilitating cross-border flows. Yet, 18 of 34 RTGS systems still rely on participants’ correspondent banking relationships for cross-border legs. Five RTGS systems plan future links, and 18 are exploring options.

About half of FPS (53%) and RTGS systems (47%) currently process cross-border payments; the rest handle domestic payments only. Still, 46% of FPS and 24% of RTGS systems that now restrict payments domestically plan to enable cross-border capabilities.

Among FPS enabling cross-border payments, 25% restrict these to correspondent banking routes, 10% are multi-jurisdictional by design, and 43% have interlinking arrangements such as bilateral links or single access points.

The Asia-Pacific region tops FPS interlinking with six systems reporting bilateral links, alongside one from the Middle East and Africa. This includes around 17 bilateral corridors, primarily multicurrency, enabling transactions in both corridor currencies.

Governance and oversight remain critical challenges. While almost all FPS with bilateral links are overseen by home jurisdiction authorities, only three of the seven jurisdictions have mandates to oversee the interlinking arrangements themselves. Among these, cooperative oversight varies from formal agreements to informal or no cooperation.

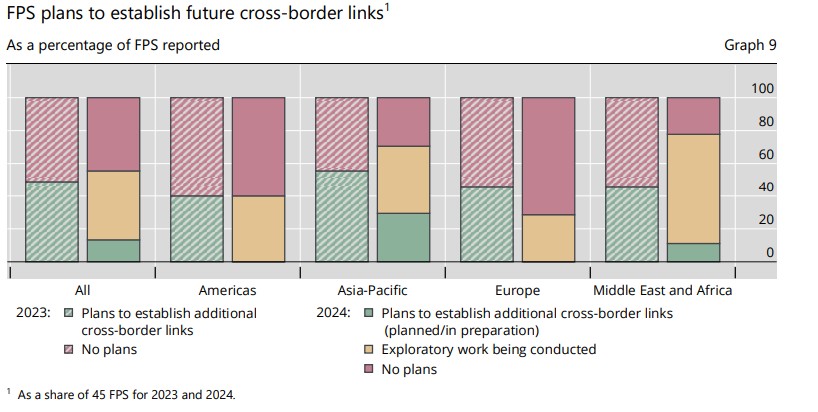

Interest in FPS interlinking is strong, with more than half of the 45 reported FPS exploring or planning connections, primarily in an exploratory phase.

Interlinking promises greater connectivity and efficiency but requires careful governance to manage risks inherent in cross-border, multicurrency arrangements.

What’s next?

The 2024 CPMI survey on cross-border payments shows steady progress and increasing ambition. Key developments include longer hours of operation, increased access, the use of ISO 20022, and better interlinking in the payments system. But challenges remain.

Legal reforms, governance of interlinking arrangements, and ensuring end-user benefits require ongoing attention. The next few years will be critical for turning infrastructure gains into tangible benefits for businesses and consumers worldwide.

The survey gathered data from a wide range of payment systems and jurisdictions worldwide, providing a comprehensive view of the current state and progress of cross-border payment infrastructures and policies.

Access the complete survey here.