As customs authorities place greater emphasis on documentary accuracy and post-clearance verification, the presentation of goods and supporting documents has become central to defending preferential origin claims.

Importers should also verify if preferential origin was correctly declared on the import declaration, not only to ensure the duty savings, but also from a trade compliance standpoint.

If the customs broker raises import declarations on behalf of the trader, it is important that the customs agent is provided with full information about the imported product and all available shipping documents are presented.

By understanding the key elements reviewed by customs authorities during documentary examinations, traders can better prepare for future audits and ensure that their commercial invoices are fully compliant, especially when claiming preference based on the invoice statement.

The checklist below outlines these and other critical points, which are in line with the WCO Guidelines on Preferential Origin Verification (July 2015) for customs administrations:

- Invoice declaration wording is correct and in line with the format under the FTA

- Names of the exporter and importer

- Invoice number and date of issuance

- Correct and full description and quantity of goods

- Price of the goods (refer to the Customs Valuation section of the Exporters Playbook)

- Delivery terms (Incoterms®), depending on contractual arrangements between seller and buyer

- HTS or tariff codes of goods

Below is an example of what a commercial invoice could look like:

| Commercial Invoice Date: 01/08/2025 | |||||

| Sender:

Motor Parts Ltd. Millenium Business Park, Port Street, B12 – AWW Birmingham, United Kingdom |

Invoice number 00899 | Receiver / Billed to / Delivery to: Car Parts s.r.o.

Central Business Park 186 00 Nové Město Czech Republic |

|||

| Order number 123456 | Delivery note number: 14725 | ||||

| Delivery terms – CPT Car Parts s.r.o., , Nové Město, Czech Republic, Incoterms® 2020 | Transport ref: 8689544 | Despatch date: 01/08/2025 | |||

| Total Gross

20 Kgs |

Total Net

15 Kgs |

||||

| Pos | Part number | Part description | Quantity | Price (GBP) per unit | Total |

| 001 | M-4444 | Universal AC/DC Motor – large (2.5 Kgs) | 6 | £ 1,100.00 | £ 6,600.00 |

| Tariff code: 8501109190

Country of origin: GB |

|||||

| Packaging | 1 box 50 x 70 x 80 cm | ||||

| Invoice declaration

Period: from 01/01/2025 – 31/12/2025) The exporter of the products covered by this document (customs authorisation number 4567889) declares that, except where otherwise clearly indicated, these products are of GB preferential origin Birmingham, UK 01/08/2025 Sarah Smith (Motor Parts Ltd.) Customs Compliance Officer |

|||||

Origin management is an ongoing responsibility that does not end at the point of issuing the proof of origin. Customs authorities may conduct retrospective audits, and depending on the request, the importer of record must be prepared to provide the corresponding proof of origin for any audited entry.

Conducting post-entry audits is a best practice for maintaining compliance and identifying any missed opportunities for duty relief.

Below is a checklist with suggested post-entry checks related to preferential origin:

- Check whether the import declaration includes any preference, document, or status codes indicating a preferential programme (e.g. FTA, GSP) and if they are applicable

- Compare the import declaration against clearance instructions (if any were issued)

- If a preferential origin was claimed, confirm that the product meets the preference eligibility criteria

- Verify that the declared country of origin is correct and in line with the commercial invoice

- Ensure proof of origin is available (e.g. an invoice statement included on the commercial invoice), or a certificate of origin is received

- In case of any discrepancies, raise entry amendments as soon as possible; subsequent corrective action must be taken, and any errors rectified

- Depending on the severity of the error, consider submitting a voluntary disclosure to the relevant customs authority

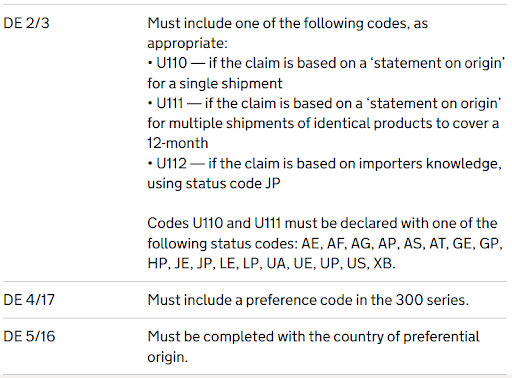

The figure below (from the UK’s HM Revenue & Customs) provides an example of document and status code checks on import declarations submitted via the UK Customs Declaration Service (CDS), specifically for trade between the UK and the EU.

Case study: Textile company

A customs specialist of an AEO-approved textile company in the UK is conducting post-entry customs audits on imported products from the previous month. The customs specialist pays extra attention to courier shipments, which are very fast-moving and high in frequency.

The import declaration of a selected entry shows the country of origin as Germany, and preferential origin was claimed: the preference code states ‘300’ and document code ‘U116’ was used along with ‘AE’ status code. However, the commercial invoice states that goods are of non-preferential status, with line items marked as ‘N’, and a note at the bottom of the invoice stating: ‘Only line items marked as ‘Y’ are of preferential origin.’

The customs broker missed this and declared goods under preferential treatment. The customs specialist, spotting the error, wrote an email to the courier requesting that an amendment be made and attached a copy of the invoice and import declaration.

The courier initially refused, stating that the goods came from Germany and therefore must be of preferential origin under the TCA. The customs specialist advised that just because the goods were dispatched from Germany, it does not make them of German origin, and pointed out the ‘N’ status and the explanatory text on the bottom of an invoice. The courier then agreed to make the amendment to this entry.

For deeper insight into documentary compliance, preferential origin controls, and post-clearance audit readiness, explore the full Exporters Guide here